PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035005

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035005

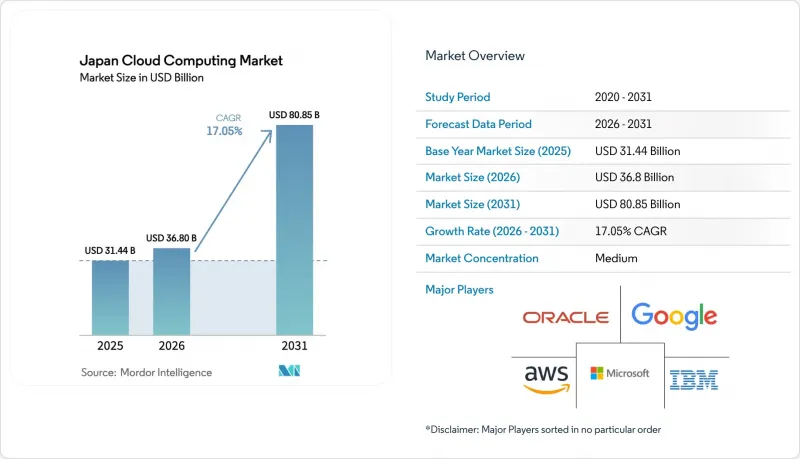

Japan Cloud Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan Cloud Computing market size is expected to grow from USD 31.44 billion in 2025 to USD 36.8 billion in 2026 and is forecast to reach USD 80.85 billion by 2031 at 17.05% CAGR over 2026-2031.

Growth reflects three powerful forces: the sovereign-AI agenda, accelerated digital-transformation programs, and heavy foreign hyperscaler investment that is reshaping enterprise IT strategies. Central-government "Cloud-by-Default" rules compel agencies to adopt domestic platforms, while manufacturers, banks, and healthcare providers rely on cloud services to modernize legacy environments and deploy generative-AI workloads. Foreign providers have pledged more than USD 25 billion in new capacity, yet domestic firms capture sensitive workloads by pairing regulatory compliance with leading-edge GPU infrastructure. Labor shortages, tax incentives for green data-centres, and Tokyo-area power congestion all reinforce the migration away from on-premises servers toward elastic cloud resources. Taken together, these factors position the Japan cloud computing market for robust multi-year expansion.

Japan Cloud Computing Market Trends and Insights

Generative-AI workload boom demanding sovereign compute

Japan's appetite for high-performance compute has exploded since the government earmarked JPY 72.5 billion (USD 483 million) for five domestic providers tasked with building sovereign-AI infrastructure. This funding mitigates the global GPU shortage and reduces reliance on foreign clouds, a dependency that produced a digital-trade deficit of JPY 5.5 trillion in 2023. SoftBank's plan to deploy the world's first DGX SuperPOD in Tokyo with a JPY 150 billion investment by 2025 illustrates private-sector alignment with sovereign goals. Start-ups receive subsidised access through the Generative-AI Accelerator Challenge, which feeds demand for domestic IaaS and creates a feedback loop: more compute capacity enables advanced local models, which in turn justify further capacity additions. International players such as OpenAI now maintain Tokyo offices, heightening competitive urgency for local alternatives that guarantee data residency compliance.

Government "Cloud-by-Default" and Digital Agency Gov-Cloud rollout

The Digital Agency's Cloud First Principle mandates that all new government systems adopt cloud services unless a stronger rationale exists for other models. Under the agency's certification scheme, Sakura Internet became the first domestic provider to pass the rigorous ISMAP security assessment, setting a procurement precedent that favours in-country operators. Pilot projects running generative-AI chatbots for document drafting and citizen-service inquiries proved viable during December 2023 March 2024 field tests, leading ministries to budget additional cloud spending in fiscal 2025Municipalities also migrate legacy registries to the Government Cloud framework, reducing fragmented IT contracts and freeing funds for broader digital-transformation efforts.

Strict cross-border data-residency and privacy rules

Amendments to the Act on the Protection of Personal Information broaden restrictions on offshore processing, while the Economic Security Promotion Act classifies cloud systems as critical infrastructure that must undergo domestic supply-chain verification. Although Japan recently endorsed the Data Free Flow with Trust framework to ease certain transfers, regulators still apply a cautious stance toward sensitive datasets, compelling enterprises to retain core information inside national borders. Financial institutions respond by segmenting platforms: regulated workloads remain in domestic availability zones, while less-sensitive services run overseas. Compliance complexity increases provider switching costs and raises barriers for smaller foreign entrants.

Other drivers and restraints analyzed in the detailed report include:

- Tax incentives for regional green data-centres using renewables

- Robust DX programs in manufacturing and BFSI

- Cloud-native talent scarcity and wage inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid architectures record a 18.45% CAGR to 2031 as Japanese enterprises blend global reach with in-country data control. Public-cloud options captured 52.60% of Japan cloud computing market share in 2025, yet sensitive workloads remain on private clouds or domestic infrastructure. Government projects typically position regulated data within sovereign regions while shifting public-facing portals to hyperscale nodes. Migration roadmaps frequently phase legacy mainframes into containerized microservices that connect to public APIs. This staged approach minimizes downtime and aligns with risk-mitigation guidelines issued by the Financial Services Agency.

Hybrid frameworks also solve latency and energy-availability constraints. Firms deploy on-premises edge nodes for deterministic manufacturing processes while bursting AI training tasks into GPU clusters housed in Tokyo or Osaka mega-facilities. The Digital Agency's Gov-Cloud design codifies this model, combining local IaaS with community clouds accessible by prefectural agencies. Consequently, the Japan cloud computing market benefits from diversified spend across both foreign and domestic providers, amplifying total capacity without breaching residency mandates.

Software-as-a-Service led with 46.10% of the Japan cloud computing market size in 2025 because pre-configured applications accelerate time-to-value. Enterprises tap SaaS for ERP modernisation, unified communications, and cybersecurity posture management. However, Platform-as-a-Service registers the fastest 21.10% CAGR through 2031, driven by the need to build and iterate AI solutions rapidly. PaaS offerings bundle data pipelines, model-training environments, and DevSecOps toolchains, freeing developers from infrastructure administration.

Infrastructure-as-a-Service remains foundational, but price competition compresses margins. Providers differentiate by pairing bare-metal GPU instances with managed Kubernetes and serverless functions. The joint proposal by NTT, KDDI, Fujitsu, NEC, and Rakuten to deliver Beyond-5G PaaS underscores this shift toward integrated stacks tuned for subsector use cases. As native-language large-language-models proliferate, demand for specialised PaaS accelerates, sustaining high utilisation of sovereign compute clusters and reinforcing the broader Japan cloud computing market.

Japan Cloud Computing Market Report is Segmented by Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Service Model (IaaS, Paas, Saas), Organisation Size (Large Enterprises, Smes), End-User Industry (BFSI, Manufacturing, Healthcare and More), Workload Type (AI/ML & HPC, ERP & Core Business Apps, Web Hosting & CDN and Pune), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- NTT Communications

- Fujitsu Ltd

- NEC Corp

- Oracle Corp

- IBM Corp

- Salesforce Inc

- SAP SE

- Rackspace Technology

- Internet Initiative Japan (IIJ)

- SoftBank Corp

- KDDI / TELEHOUSE

- Sakura Internet

- Hitachi Ltd

- GMO Cloud

- Alibaba Cloud Japan

- DigitalOcean

- VMware by Broadcom

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Generative-AI workload boom demanding sovereign compute

- 4.2.2 Government "Cloud-by-Default"and Digital Agency Gov-Cloud rollout

- 4.2.3 Tax incentives for regional green data-centres using renewables

- 4.2.4 Robust DX programs in manufacturing and BFSI

- 4.2.5 Vendor-financed mainframe-to-cloud migration schemes

- 4.2.6 Acute GPU/ASIC shortages pushing pay-as-you-go IaaS adoption

- 4.3 Market Restraints

- 4.3.1 Strict cross-border data?residency and privacy rules

- 4.3.2 Cloud-native talent scarcity and wage inflation

- 4.3.3 Tokyo-area power-grid congestion delaying hyperscale permits

- 4.3.4 Keiretsu-driven vendor lock-in slowing multicloud uptake

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Demand Trends

- 4.8 Case Study Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Service Model

- 5.2.1 Infrastructure-as-a-Service (IaaS)

- 5.2.2 Platform-as-a-Service (PaaS)

- 5.2.3 Software-as-a-Service (SaaS)

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Healthcare

- 5.4.4 Retail and E-Commerce

- 5.4.5 Telecom and IT

- 5.4.6 Government and Public Sector

- 5.4.7 Others

- 5.5 By Workload Type

- 5.5.1 AI / ML and HPC

- 5.5.2 ERP and Core Business Apps

- 5.5.3 Web Hosting and CDN

- 5.5.4 Dev/Test and CI-CD

- 5.5.5 Data Analytics and Big Data

- 5.5.6 IoT and Edge Workloads

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services (AWS)

- 6.4.2 Microsoft Azure

- 6.4.3 Google Cloud

- 6.4.4 NTT Communications

- 6.4.5 Fujitsu Ltd

- 6.4.6 NEC Corp

- 6.4.7 Oracle Corp

- 6.4.8 IBM Corp

- 6.4.9 Salesforce Inc

- 6.4.10 SAP SE

- 6.4.11 Rackspace Technology

- 6.4.12 Internet Initiative Japan (IIJ)

- 6.4.13 SoftBank Corp

- 6.4.14 KDDI / TELEHOUSE

- 6.4.15 Sakura Internet

- 6.4.16 Hitachi Ltd

- 6.4.17 GMO Cloud

- 6.4.18 Alibaba Cloud Japan

- 6.4.19 DigitalOcean

- 6.4.20 VMware by Broadcom

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment