PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035010

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035010

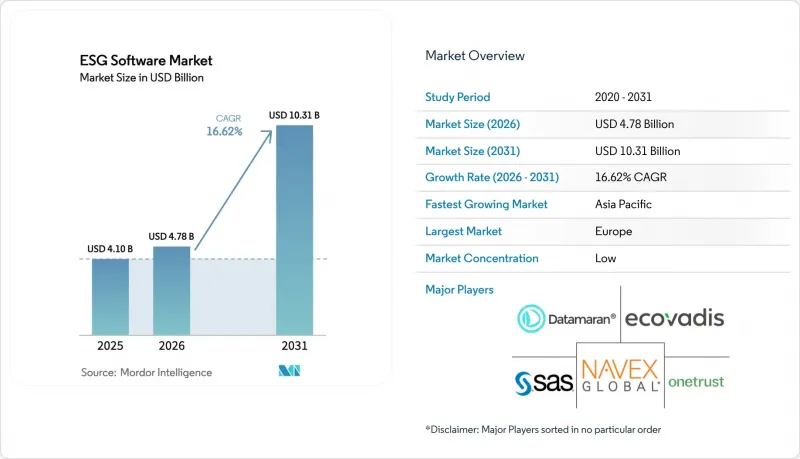

ESG Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The ESG software market size in 2026 is estimated at USD 4.78 billion, growing from 2025 value of USD 4.1 billion with 2031 projections showing USD 10.31 billion, growing at 16.62% CAGR over 2026-2031.

Rapid growth springs from converging regulatory mandates, mounting investor scrutiny, and technology advances that simplify data aggregation and reporting. Europe's Corporate Sustainability Reporting Directive (CSRD) and the United States Securities and Exchange Commission (SEC) climate rules now obligate thousands of firms to disclose standardized environmental, social, and governance (ESG) metrics, accelerating global demand for purpose-built platforms. Artificial intelligence (AI) and blockchain innovations further elevate the ESG software market by automating data quality checks and ensuring immutable audit trails. Cloud-native deployment lowers the entry barrier for small and medium enterprises (SMEs), while rising expectations for supply-chain transparency keep spending high across manufacturing, retail, and energy verticals.

Global ESG Software Market Trends and Insights

Regulatory Push for Standardized ESG Disclosures

Global policymakers have synchronized sustainability rules, forcing firms to align with CSRD in Europe, SEC climate directives in the United States, and similar statutes in California and Asia-Pacific. The CSRD alone expands mandatory reporting to more than 50,000 companies, requiring double materiality assessments that many legacy systems cannot support. Parallel SEC rules oblige large accelerated filers to disclose Scope 1 and Scope 2 emissions starting with fiscal year 2025, intensifying demand for multi-framework compliance engines sec.gov. Vendors that embed pre-mapped disclosure templates and audit-ready evidence repositories have become preferred partners, especially among global multinationals navigating overlapping frameworks.

Investor & Stakeholder Pressure for Transparency

Institutional investors link access to capital with granular ESG performance data. European retail banking research indicates 24% of customers would switch banks over poor ESG credentials. Corporations such as Digital Realty already track 66% renewable energy consumption and evaluate 60% of their suppliers for ESG risks using dedicated software, signaling how real-time dashboards influence stakeholder confidence. Green bond volumes continue to climb, so automated investor reporting modules and API-level integrations with treasury systems have become must-have features for CFOs.

High Implementation & Integration Costs for Legacy-Heavy Industries

Industrial enterprises with proprietary control systems face steep expenses retrofitting ESG data feeds. Manufacturers expect to add staff and adopt AI to meet CSRD and SEC requirements, yet early pilots expose budget overruns tied to outdated data architectures. Hospitals must connect patient management systems with emissions calculators to comply with EU taxonomy, further inflating IT project scopes envoria.com. Utilities upgrading data centers confront similar costs because 89% of technology leaders now prioritize sustainability metrics in procurement. Long integration timelines and custom connectors slow adoption, dampening overall CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Operational Efficiency Gains via Centralized ESG Data

- Rising Adoption of Cloud-Native ESG Platforms Among SMEs

- Data Quality & Fragmentation Across Global Supply Chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated the majority of revenue in 2025, yet service engagements such as integration, advisory, and managed reporting are expanding at 18.06% CAGR through 2031. Implementation projects often pair core ESG platforms with carbon accounting, product stewardship, and audit modules, spurring demand for multi-year consulting contracts. Vendors with standardized delivery frameworks shorten deployment cycles, appealing to manufacturers retrofitting enterprise resource planning suites. Meanwhile, the ESG software market size for integration services is projected to climb steadily as firms outsource complex supplier data onboarding to domain specialists. Managed services remain an emerging niche, but rising governance obligations suggest an uptick as organizations pivot to "compliance-as-a-service" to control costs.

Second-order impacts include heightened consolidation activity: platform providers increasingly acquire boutique consultancies to bundle software licenses with delivery capacity. Clients value single-provider accountability, pushing vendors to broaden domain knowledge across regulations, industry benchmarks, and assurance standards. Over the forecast period, the ESG software market will likely blur the line between product and professional service as holistic transformation partnerships become standard.

Although multitenant cloud remains the primary deployment model, government procurement policies and data-residency requirements lift demand for hybrid architecture. The ESG software market size for hybrid deployments is set to record the fastest CAGR, driven by energy utilities and public firms that must retain sensitive data on-premise while leveraging cloud analytics for scenario planning. Organizations balancing sovereignty with scalability adopt containerized micro-services that orchestrate workloads across private data centers and sovereign cloud zones. Software vendors have responded by adding policy-based data routing, encryption, and zero-trust frameworks.

Cloud supremacy continues because subscription models align with CSRD phase-in schedules. Software upgrades integrate new disclosure templates without customer downtime, critical when Europe refines European Sustainability Reporting Standards. For high-volume data ingest-such as IoT sensors monitoring Scope 1 emissions-elastic cloud storage avoids capital outlay. ESG software market share will remain concentrated around cloud first movers; however, firms with multilayer hybrid roadmaps are capturing fast-growth, regulation-sensitive verticals.

ESG Software Market Report Segments the Industry Into Offerings (Solution, Services), by Deployment (Cloud, On-Premise), by Enterprise (SMEs, Large Enterprises), by End-User Vertical (BFSI, IT and Telecom, Manufacturing, Retail and E-Commerce, Healthcare, Government, Other End-User Verticals), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retains leadership owing to unified policy frameworks and strong investor activism. The CSRD, effective from January 2024, triggered a wave of platform renewals and expansions. Multinational corporations headquartered in France, Germany, and the Nordics scale up integrated suites that map double materiality outcomes. The ESG software market size attached to Europe thus shows stable yet mature expansion.

Asia-Pacific exhibits the steepest growth trajectory. China mandates sustainability reports for more than 300 listed entities by 2026, prompting local and foreign suppliers to adopt standardized toolsets. Singapore will require climate disclosures from all listed companies in 2025, and Japan promotes AI-driven ESG scoring agents, as demonstrated by HEROZ and NZAM's joint launch in 2025. Governments also establish green-finance taxonomies, so cross-border investors insist on common data definitions, driving regional convergence.

North America advances at a steady clip. SEC rules spur public companies to automate Scope 1 and Scope 2 tracking, while state-level initiatives-such as California's Climate Accountability Package-extend disclosure to suppliers. A thriving venture ecosystem funds AI-first ESG startups, and utilities like Xcel Energy pilot carbon-monitoring software to meet net-zero commitments.

The Middle East and Africa remain nascent but display early interest, especially among sovereign wealth funds and national oil companies pursuing diversification and low-carbon strategies. Pilot projects concentrate in Gulf Cooperation Council nations where compliance with global capital-market expectations becomes essential.

- Datamaran

- EcoVadis

- NAVEX

- SAS Institute

- OneTrust

- Coolset

- TruValue Labs (FactSet)

- Diligent

- Workiva

- Persefoni

- Sphera Solutions

- Enablon (Wolters Kluwer)

- Intelex

- Cority

- Plan A

- Greenstone

- IBM Envizi

- Salesforce (Net Zero Cloud)

- FigBytes

- ESG Book

- Novisto

- IsoMetrix

- Benchmark ESG (Gensuite)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for standardized ESG disclosures

- 4.2.2 Investor and stakeholder pressure for transparency

- 4.2.3 Operational efficiency gains via centralized ESG data

- 4.2.4 Rising adoption of cloud-native ESG platforms among SMEs

- 4.2.5 AI-powered predictive analytics enabling proactive risk management

- 4.2.6 Tokenization and blockchain for immutable ESG data provenance

- 4.3 Market Restraints

- 4.3.1 High implementation and integration costs for legacy-heavy industries

- 4.3.2 Data quality and fragmentation across global supply chains

- 4.3.3 Shortage of in-house ESG expertise and change-management capability

- 4.3.4 Evolving standards causing solution re-architecture cycles

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

- 4.8 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Sustainability Reporting and Disclosure Platforms

- 5.1.1.2 Carbon Accounting Software

- 5.1.1.3 Supply-Chain ESG Management

- 5.1.1.4 Risk and Compliance Management

- 5.1.1.5 Audit and Assurance Tools

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration

- 5.1.2.2 Consulting and Advisory

- 5.1.2.3 Training and Support

- 5.1.2.4 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment

- 5.2.1 Cloud (SaaS)

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises (more than 1,000 employees)

- 5.3.2 Mid-Sized Enterprises (250 to 999)

- 5.3.3 Small Enterprises (less than 250)

- 5.4 By Functionality

- 5.4.1 Data Collection and Aggregation

- 5.4.2 Materiality Assessment

- 5.4.3 Analytics and Benchmarking

- 5.4.4 Reporting and Disclosure Automation

- 5.4.5 Scenario Analysis and Forecasting

- 5.4.6 Stakeholder Engagement

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Manufacturing

- 5.5.3.1 Automotive

- 5.5.3.2 Chemicals and Materials

- 5.5.3.3 Heavy Industry and Engineering

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Energy and Utilities

- 5.5.7 Government and Public Sector

- 5.5.8 Others (Education, Hospitality, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Netherlands

- 5.6.3.7 Russia

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 ASEAN-5

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Israel

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Datamaran

- 6.4.2 EcoVadis

- 6.4.3 NAVEX

- 6.4.4 SAS Institute

- 6.4.5 OneTrust

- 6.4.6 Coolset

- 6.4.7 TruValue Labs (FactSet)

- 6.4.8 Diligent

- 6.4.9 Workiva

- 6.4.10 Persefoni

- 6.4.11 Sphera Solutions

- 6.4.12 Enablon (Wolters Kluwer)

- 6.4.13 Intelex

- 6.4.14 Cority

- 6.4.15 Plan A

- 6.4.16 Greenstone

- 6.4.17 IBM Envizi

- 6.4.18 Salesforce (Net Zero Cloud)

- 6.4.19 FigBytes

- 6.4.20 ESG Book

- 6.4.21 Novisto

- 6.4.22 IsoMetrix

- 6.4.23 Benchmark ESG (Gensuite)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment