PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035013

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035013

Indie Game - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

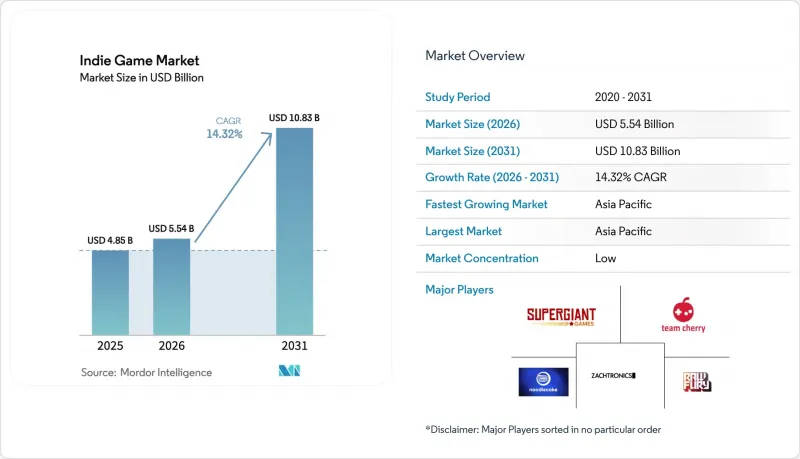

The indie game market size is expected to grow from USD 4.85 billion in 2025 to USD 5.54 billion in 2026 and is forecast to reach USD 10.83 billion by 2031 at 14.32% CAGR over 2026-2031.

The surge reflects how low-cost engines, generous first-party publishing schemes, and near-frictionless global storefronts are flattening structural barriers for small studios. Mobile platforms have become the primary revenue engine as 5G roll-outs in Latin America and Southeast Asia pull new players into the paid ecosystem. Subscription services are gaining traction, yet one-off premium sales still provide critical day-one cash flow that funds creative risk-taking. Rapid catalog growth on Steam and the App Store signals vibrant supply, but the same abundance amplifies discoverability challenges and marketing cost inflation for newcomers.

Global Indie Game Market Trends and Insights

Expanding Reach of Digital Distribution Platforms in Asia

Asia-Pacific's bandwidth upgrades and mobile-first habits are widening the addressable indie audience. The region already houses 1.5 billion active mobile gamers, and alternative carrier-backed storefronts such as dtac's Gaming Nation are winning creators by taking smaller revenue cuts. Indonesia's 96% mobile gaming preference shows how emerging markets bypass consoles entirely. Direct carrier billing lowers payment friction, letting solo studios monetize impulse purchases that credit-card-dependent channels miss. These factors collectively add weight to the indie game market growth outlook as regional storefront competition keeps platform fees under pressure.

Democratization of Game Engines and Dev-Tools

Unity powered 48% of all 2024 Steam releases, proving that easy-to-learn, royalty-free engines shorten time-to-market for small teams. Unreal Engine's photoreal toolset is also showing up in higher-fidelity independent productions, while open-source Godot offers zero-royalty freedom. AI-assisted editors further compress iteration cycles, making narrative, art and code chores more approachable for non-technical creators. The widespread tool democratization keeps contributor diversity high and feeds the indie game market with new genres and artistic voices.

Saturation on Key Digital Marketplaces (Steam, App Store)

Steam listed over 14,000 new titles in 2024, diluting storefront visibility and shrinking wishlist-to-sale conversion ratios to 0.125. Algorithms increasingly reward proven engagement, so unlaunched games fight uphill battles against entrenched hits. First-time teams often divert scarce resources to pre-launch marketing, driving costs beyond sustainable levels. The crowding effect slows revenue velocity, tempering indie game market expansion despite robust consumer appetite.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Based Indie Publishing Partnerships

- 5G-Enabled Mobile Gameplay Enhancing Engagement in LATAM

- Discoverability and User-Acquisition Cost Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile's 51.42% revenue share underscores how always-connected play aligns with indie design constraints. The segment is forecast to post a 16.52% CAGR, pulling the indie game market size for mobile-first titles toward the USD 6.2 billion mark by 2031. Nintendo Switch remains a lucrative secondary channel; 45% of households own multiple units, and the family-friendly catalog bias dovetails with indie aesthetics. PC is still the default development environment because open storefronts offer higher revenue splits, yet fierce competition reduces average earnings. Console ecosystems bring curated discoverability but entail more compliance overhead and longer certification queues.

Cross-platform engines now allow simultaneous release across PC, console, and mobile without tripling asset budgets. Cloud gaming sidesteps hardware caps, but bandwidth variability hampers adoption in lower-income regions. Success cases such as "Clair Obscur: Expedition 33," which sold 1.5 million units across three platforms on a sub-USD 30 million budget, showcase scale possibilities. Multiplayer parity and cross-save functions have become baseline consumer expectations, forcing teams to architect networking features early or face negative store reviews.

Action/adventure still commands 28.35% of 2025 revenue, illustrating player loyalty to skill-based, story-driven gameplay loops. Yet simulation and sandbox titles are climbing at a 16.78% CAGR, reflecting social-creation trends and the economic appeal of user-generated content ecosystems. The indie game market share lead may tilt if simulation growth sustains beyond 2027. Role-playing games attract high-engagement cohorts willing to pay for narrative DLC, offering steady annuity revenue in lieu of blockbuster spikes. Strategy and puzzle niches exhibit lower production costs, allowing micro-studios to survive on modest absolute sales.

Hybrid sub-genres blur boundaries, evidenced by survival-craft hits that merge sandboxes with roguelike progression. Cozy life sims echo wellness and escapism themes, leveraging low-consequence mechanics to appeal to broader demographics. Regional taste skews are pronounced; APAC gravitating to mobile-friendly casual sims, while Western players lean toward story-rich experiences. Such diversity keeps genre experimentation high, reinforcing the creative churn that underpins indie game market resilience.

Indie Game Market Report is Segmented by Device Type (PC, Mobile, Console), Game Genre (Action / Adventure, Role-Playing (RPG), Simulation and Sandbox, and More), Business Model (Premium (One-Time Purchase), Free-To-Play, and More), Distribution Channel (Digital Storefronts, Third-Party Publishing Platforms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the indie game market with a 44.35% revenue share in 2025 and is pacing at 16.08% CAGR. South Korea's Ministry of Culture earmarked 5 trillion won (USD 3.6 billion) for content industries, handing out grants, tax breaks, and overseas marketing grants that pull indies into global festivals. China's studios dominate mobile top-grossing charts worldwide, providing collaboration pathways and outsourcing demand that fund smaller regional teams. India represents the fastest-growing gamer base, forecast to add 250 million users by 2030 as smartphone affordability rises.

North America remains the heartbeat for premium indie launches; strong disposable income and console penetration support higher average selling prices. Canada's tax credits of up to 37.5% of labor costs lower effective burn for Montreal and Vancouver studios. The United States supplies platform HQs, venture funding, and large-scale conventions such as GDC that act as find-a-publisher accelerators. Mexico and Brazil's 5G expansions fuel mobile-centric revenue, and local payment solutions foster micro-transactions at scale.

Europe benefits from coordinated public funding. Sweden's game sector generated SEK 34.6 billion (USD 3.2 billion) in 2023, aided by export-oriented tax frameworks. The European Investment Fund's USD 21 million injection into Behold Ventures widens seed capital for Nordic startups. Germany, France, and the United Kingdom anchor large PC communities and esports ecosystems that provide evergreen demand for indie strategy, sim, and narrative titles. The MENA-3 cluster (Saudi Arabia, UAE, Egypt) produced USD 1.92 billion in 2023 and is slated for USD 2.65 billion by 2027, opening greenfield potential for culturally localized content.

- Team17 Group PLC

- Devolver Digital Inc.

- Annapurna Interactive

- Thunderful Group AB

- Raw Fury AB

- Supergiant Games LLC

- Klei Entertainment Inc.

- InnerSloth LLC

- Studio MDHR

- Glass Bottom Games

- Larian Studios

- ConcernedApe LLC

- InnerSloth LLC

- Chucklefish Ltd.

- Coffee Stain Publishing AB

- Humble Games

- TinyBuild Inc.

- Versus Evil LLC

- Playdigious SAS

- Zachtronics LLC

- Team Cherry

- Noodlecake Studios

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Reach of Digital Distribution Platforms in Asia

- 4.2.2 Democratization of Game Engines and Dev-Tools (Unity, Unreal)

- 4.2.3 Cloud-Based Indie Publishing Partnerships (Xbox ID@, PS Partners)

- 4.2.4 5G-Enabled Mobile Gameplay Enhancing Engagement in LATAM

- 4.2.5 Crowdfunding and Early-Access Models Lowering Entry Barriers

- 4.2.6 Government Indie-Fund Programs (Canada, Sweden, South Korea)

- 4.3 Market Restraints

- 4.3.1 Saturation on Key Digital Marketplaces (Steam, App Store)

- 4.3.2 Discoverability and User-Acquisition Cost Inflation

- 4.3.3 Limited Access to AAA-Class Marketing Budgets

- 4.3.4 IP Infringement and Asset Cloning in Mobile Stores

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers (Gamers)

- 4.5.3 Bargaining Power of Suppliers (Engines, Stores)

- 4.5.4 Threat of Substitutes (Modding, AAA F2P)

- 4.5.5 Competitive Rivalry

- 4.6 Investment Analysis

- 4.7 Macroeconomic Impact Analysis (COVID-19 and Post-Inflation)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 PC

- 5.1.2 Mobile

- 5.1.3 Console

- 5.2 By Game Genre

- 5.2.1 Action / Adventure

- 5.2.2 Role-Playing (RPG)

- 5.2.3 Simulation and Sandbox

- 5.2.4 Strategy and Puzzle

- 5.2.5 Others (Visual Novel, Rhythm)

- 5.3 By Business Model

- 5.3.1 Premium (One-time Purchase)

- 5.3.2 Free-to-Play (IAP/Ads)

- 5.3.3 Subscription / Season Pass

- 5.3.4 Crowdfunded / Early-Access

- 5.4 By Distribution Channel

- 5.4.1 Digital Storefronts (Steam, EGS, Console Stores)

- 5.4.2 Third-Party Publishing Platforms

- 5.4.3 Physical / Collector Editions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Team17 Group PLC

- 6.3.2 Devolver Digital Inc.

- 6.3.3 Annapurna Interactive

- 6.3.4 Thunderful Group AB

- 6.3.5 Raw Fury AB

- 6.3.6 Supergiant Games LLC

- 6.3.7 Klei Entertainment Inc.

- 6.3.8 InnerSloth LLC

- 6.3.9 Studio MDHR

- 6.3.10 Glass Bottom Games

- 6.3.11 Larian Studios

- 6.3.12 ConcernedApe LLC

- 6.3.13 InnerSloth LLC

- 6.3.14 Chucklefish Ltd.

- 6.3.15 Coffee Stain Publishing AB

- 6.3.16 Humble Games

- 6.3.17 TinyBuild Inc.

- 6.3.18 Versus Evil LLC

- 6.3.19 Playdigious SAS

- 6.3.20 Zachtronics LLC

- 6.3.21 Team Cherry

- 6.3.22 Noodlecake Studios

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment