PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035016

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035016

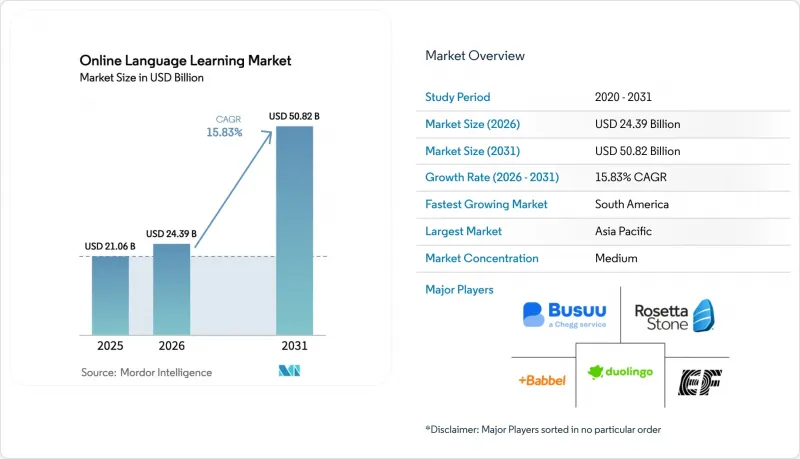

Online Language Learning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The online language learning market size was valued at USD 21.06 billion in 2025 and estimated to grow from USD 24.39 billion in 2026 to reach USD 50.82 billion by 2031, at a CAGR of 15.83% during the forecast period (2026-2031).

Growing cross-border trade, demographic shifts, and rapid mobile adoption keep demand high, while AI-driven personalization and immersive technologies strengthen learning effectiveness. Platforms deliver ever-larger course catalogues and adaptive paths that improve retention, a key differentiator in an increasingly competitive landscape. Corporates accelerate spending on workforce language skills to meet ESG and DEI goals, and public-sector budgets for multilingual programs further expand the accessible learner base. Meanwhile, strict data-privacy regimes in Europe and rising user-acquisition costs in saturated freemium channels temper growth, encouraging platforms to refine monetization strategies and diversify revenue streams.

Global Online Language Learning Market Trends and Insights

Globalisation-driven cross-border communication demand

Intensifying international trade turns language proficiency into a core competitiveness lever. Enterprises across technology, tourism, and finance invest in scalable online language programs to remove communication bottlenecks. Providers like Open English have broadened Latin American access by marketing English skills as an economic mobility enabler. Regional trade blocs also lift demand for Portuguese and Spanish, underscoring multi-directional growth beyond English .

AI-powered adaptive learning penetration

Artificial-intelligence engines now adjust content sequencing, difficulty, and feedback in real time, raising completion rates and upsell potential. Duolingo integrates generative AI to personalize review loops and pronunciation drills, an investment detailed in its 2024 SEC filing . Venture funding echoes this trend: Speak's valuation surpassed USD 1 billion after proving conversational AI can support a billion spoken sentences and premium adoption. Platforms that align AI with privacy-by-design guidelines build durable differentiation under Europe's strict data regime.

Data-security and privacy concerns

GDPR rules prohibit unchecked voice-data transfers to third-party AI processors, forcing platforms to build costly private speech-recognition pipelines. New localization mandates further raise overhead, compressing smaller entrants' margins and nudging the market toward scale players with in-house compliance teams.

Other drivers and restraints analyzed in the detailed report include:

- Mobile-first uptake in emerging economies

- Corporate ESG and DEI language-upskilling mandates

- Low course-completion and high churn rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-learning apps generated 56.35% of 2025 revenue, underpinning the online language learning market's largest delivery channel. This dominance relies on always-on accessibility, micro-lesson design, and algorithmic personalization that lower per-learner cost. However, tutor-led live instruction is advancing at 21.25% CAGR, reflecting heightened demand for real-time conversation that algorithms still only partially simulate. Hybrid pathways-recorded modules plus weekly tutor sessions-emerge as the retention sweet-spot, helping platforms defend subscription pricing. Preply's marketplace illustrates the financial upside of such blended delivery, with session bookings rising alongside subscription upgrades. Continued innovation in scheduling automation and pay-per-minute billing is expected to pull more independent instructors onto aggregated platforms, deepening supply and compressing lesson prices to learners' benefit.

Rising broadband quality in emerging markets further boosts live tutoring uptake by mitigating latency that previously hindered synchronous video practice. Conversely, self-learning incumbents invest in AI voice partners to replicate tutor feedback. The dual strategy indicates the online language learning market will not polarize; rather, integrated workflows will dominate. Providers that dynamically route learners between self-study and live conversation based on progress signals could see higher lifetime value and lower churn.

Individuals held 47.35% of 2025 revenue-a foundational pillar of the online language learning market. Price-sensitive consumers gravitate toward freemium models, forcing platforms to balance ad loads and feature gating. In contrast, corporate clients, expanding at 23.70% CAGR, purchase bulk licences bundled with analytics dashboards and single-sign-on integrations that command 6-8X higher ARPU. Speak for Business reports 85% internal adoption within client firms, reinforcing the stickiness of enterprise rollouts.

Public-sector allocations strengthen demand from schools and workforce-integration programs. U.S. English Language Acquisition grants, for instance, stimulate district-level procurement of adaptive solutions, thereby funneling learners into long-term online ecosystems . The cross-subsidy effect allows vendors to reinvest in consumer feature development, illustrating the symbiotic revenue model spanning consumer and B2B sub-markets within the broader online language learning market.

The Online Language Learning Market is Segmented by Learning Mode (Self Learning Apps, Tutor-Led, Blended Learning, and More), End-User (Individual, Corporate Learners, Educational Institutions, and More), Language (English, Mandarin Chinese, Spanish, French, and More), Age Group (<< 13 Years, 13 - 17 Years, 18 - 30 Years, and More), Technology Platforms (Mobile Applications, Web-Based Platforms, and More), and Geography.

Geography Analysis

Asia-Pacific, with 45.75% of 2025 revenue, remains the engine of the online language learning market. China's urban learners pay for premium English tracks that facilitate overseas study, while India's young mobile-native population leans on freemium tiers to supplement exam preparation. Government multilingual policies in Indonesia and Vietnam mandate early exposure, broadening the K-12 funnel. Corporate-sector demand grows as regional firms court foreign investment, pushing vendors to launch HR dashboards that log skill progression for compliance reporting.

South America posts the fastest 21.90% CAGR outlook, propelled by Brazil's massive user base and Mexico's near-shoring boom that values bilingual staff. Subsidized smartphone plans and improved 4G coverage widen distribution channels, letting platforms bundle English courses with telecom loyalty programs. Local cultural references in content-sports idioms, regional slang-have proven to lift completion rates, a critical insight for the online language learning market's course-design strategy.

North America and Europe exhibit high per-capita spend yet slower learner-base expansion. North America benefits from immigration-driven heritage-language niches and enterprises' DEI budgets. Europe's GDPR compliance costs elevate entry barriers, tilting competitive advantage toward established providers with in-house legal and infosec teams. Nevertheless, both regions act as innovation testbeds-features perfected here, like real-time dysfluency analytics, later scale into Asia-Pacific and South America, reinforcing a global RandD diffusion cycle inside the online language learning market.

- Duolingo Inc.

- Babbel GmbH

- Busuu Ltd.

- Memrise Ltd.

- Preply Inc.

- Rosetta Stone LLC

- italki HK Ltd.

- Lingoda GmbH

- Enux Education Ltd. (LingoDeer)

- Berlitz Corporation

- EF Education First Ltd.

- VIPKid HK Ltd.

- HelloTalk Ltd.

- Speexx AG

- Mango Languages (Creative Empire LLC)

- Cambridge University Press and Assessment

- Kaplan International Languages

- Pimsleur (Simon and Schuster)

- FluentU Inc.

- Tandem Fundazioa (Tandem app)

- Voxy Inc.

- Open English LLC

- Lingvist OU

- Cambly Inc.

- Speaky Community SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Globalisation-driven cross-border communication demand

- 4.2.2 AI-powered adaptive learning penetration

- 4.2.3 Mobile-first uptake in emerging economies

- 4.2.4 Corporate ESG and DEI language-upskilling mandates

- 4.2.5 Early-age language mandates in K-12 curricula

- 4.2.6 Voice-assistant ecosystem skill marketplaces

- 4.3 Market Restraints

- 4.3.1 Data-security and privacy concerns

- 4.3.2 Low course-completion and high churn rates

- 4.3.3 Freemium-model revenue saturation

- 4.3.4 AI copyright / ethics regulatory barriers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Learning Mode

- 5.1.1 Self-Learning Apps

- 5.1.2 Tutor-Led

- 5.1.3 Blended Learning

- 5.1.4 AI-Adaptive Platforms

- 5.2 By End-user

- 5.2.1 Individual Learners

- 5.2.2 Corporate Learners

- 5.2.3 Educational Institutions (K-12 and Higher-Ed)

- 5.2.4 Government and Non-profit Bodies

- 5.3 By Language

- 5.3.1 English

- 5.3.2 Mandarin Chinese

- 5.3.3 Spanish

- 5.3.4 French

- 5.3.5 German

- 5.3.6 Japanese

- 5.3.7 Other Languages

- 5.4 By Age Group

- 5.4.1 < 13 Years

- 5.4.2 13 - 17 Years

- 5.4.3 18 - 30 Years

- 5.4.4 31 - 45 Years

- 5.4.5 > 45 Years

- 5.5 By Technology Platform

- 5.5.1 Mobile Applications

- 5.5.2 Web-based Platforms

- 5.5.3 VR and AR Tools

- 5.5.4 Conversational Voice Assistants

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Duolingo Inc.

- 6.4.2 Babbel GmbH

- 6.4.3 Busuu Ltd.

- 6.4.4 Memrise Ltd.

- 6.4.5 Preply Inc.

- 6.4.6 Rosetta Stone LLC

- 6.4.7 italki HK Ltd.

- 6.4.8 Lingoda GmbH

- 6.4.9 Enux Education Ltd. (LingoDeer)

- 6.4.10 Berlitz Corporation

- 6.4.11 EF Education First Ltd.

- 6.4.12 VIPKid HK Ltd.

- 6.4.13 HelloTalk Ltd.

- 6.4.14 Speexx AG

- 6.4.15 Mango Languages (Creative Empire LLC)

- 6.4.16 Cambridge University Press and Assessment

- 6.4.17 Kaplan International Languages

- 6.4.18 Pimsleur (Simon and Schuster)

- 6.4.19 FluentU Inc.

- 6.4.20 Tandem Fundazioa (Tandem app)

- 6.4.21 Voxy Inc.

- 6.4.22 Open English LLC

- 6.4.23 Lingvist OU

- 6.4.24 Cambly Inc.

- 6.4.25 Speaky Community SAS

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment