PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035022

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035022

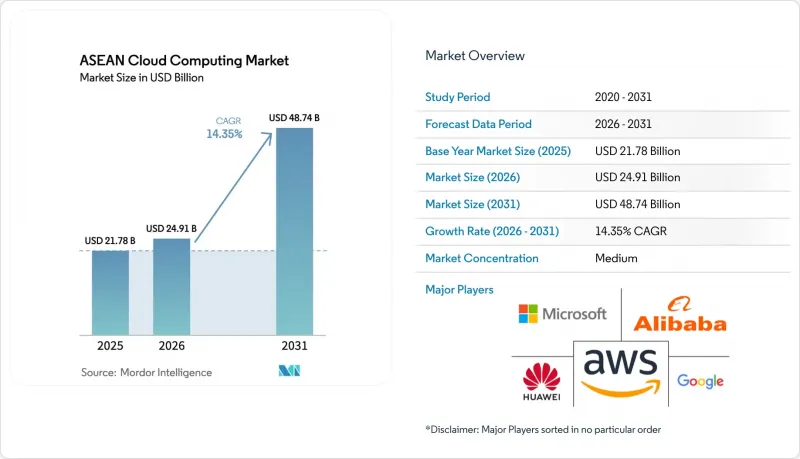

ASEAN Cloud Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The ASEAN Cloud Computing Market size was valued at USD 21.78 billion in 2025 and estimated to grow from USD 24.91 billion in 2026 to reach USD 48.74 billion by 2031, at a CAGR of 14.35% during the forecast period (2026-2031).

Singapore anchors regional demand, Vietnam registers the fastest growth, and hyperscale investments exceeding USD 25 billion in 2024-2025 have strengthened the overall capacity pipeline. Government digital-economy master plans continue to mandate cloud migration across public agencies, while enterprise modernization pushes multi-cloud and hybrid strategies. Chinese hyperscalers have added significant price competition and localized capacity, accelerating infrastructure build-out across Indonesia, Malaysia, and Thailand. The ASEAN cloud computing market benefits further from 5G-enabled edge deployments, renewable-energy data-center initiatives, and rising demand for scalable IT among SMEs.

ASEAN Cloud Computing Market Trends and Insights

Accelerated 5G roll-outs enabling edge-cloud convergence

Nationwide 5G licenses in Cambodia and dense network upgrades in Thailand are enabling millisecond-latency applications that depend on proximate cloud nodes. Utilities such as Thailand's Metropolitan Electricity Authority have already tied 5G grids to cloud analytics for predictive outage management. The synergy between edge nodes and public clouds improves service resilience and widens the addressable base for Internet-of-Things (IoT) workloads. Regional telcos now co-locate mini-data centers inside 5G base stations to minimize backhaul congestion. This convergence is expected to deepen hybrid adoption as enterprises partition latency-sensitive traffic to edge nodes while scaling the remainder on central hyperscale regions.

Surge in ASEAN hyperscale data-center investments by Chinese providers

Tencent allocated USD 500 million for Indonesian builds and formed deeper partnerships with local e-commerce leaders, delivering cost-competitive alternatives to North American platforms. Alibaba Cloud's collaborative AI programs have also widened service breadth across Malaysia and Thailand. The influx of Chinese capacity favors regulated industries that prioritize local data residency, thereby pressuring incumbent vendors on price and latency. Short-haul cross-border interconnects between Chinese-backed facilities in Johor and Singapore have begun to offer sub-2 ms latency for multi-region replication. This investment wave materially boosts the ASEAN cloud computing market's overall supply, lowering entry barriers for SMEs and start-ups.

Data residency and sovereignty regulations

Malaysia's 2025 Cross-Border Transfer Guidelines oblige firms to run Transfer Impact Assessments and prove the equivalence of foreign privacy standards. Vietnam's July 2025 Data Law classifies "core data" and enforces domestic processing for sensitive sets. Such rules fragment infrastructure planning, forcing providers to duplicate facilities, raise capital costs, and adapt service catalogs per jurisdiction. Enterprises face legal complexity and higher total cost of ownership when architecting cross-region disaster recovery. Although compliance consultancies can bridge knowledge gaps, divergent national rules remain a notable drag on ASEAN cloud computing market growth during the near term.

Other drivers and restraints analyzed in the detailed report include:

- Government digital-economy masterplans boosting cloud adoption

- Rising enterprise demand for scalable IT infrastructure

- Shortage of cloud-skilled workforce in Tier-2 markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public Cloud retained a 67.05% share of the ASEAN cloud computing market in 2025, backed by elastic pricing and abundant regional availability zones. Hybrid Cloud is forecast to post a 15.85% CAGR, generating the largest incremental addition to the ASEAN cloud computing market size between 2026-2031. Telecom operators such as AIS are blending local sovereignty with global services by launching domestically owned hyperscale platforms. Private Cloud installations continue among regulated banks and hospitals but are expected to cede share as security postures mature.

Hybrid growth springs from multi-cloud governance tooling, container portability, and maturing zero-trust frameworks. Enterprises now segment latency-critical analytics to local nodes while routing burst workloads to public zones, optimizing cost and compliance simultaneously. The approach unlocks new addressable opportunities for orchestration vendors and managed-service providers that can bridge hybrid estates across ASEAN's diverse data-regulation landscape.

Software as a Service contributed 55.65% revenue in 2025 and remains the market's most mature delivery mode. Platform as a Service, however, is on track for a 16.3% CAGR, reflecting rising developer demand for serverless runtimes and integrated DevSecOps pipelines. The PaaS surge enlarges the ASEAN cloud computing market size for developer-centric tooling, with VNPT targeting USD 11.3 billion cloud-related revenue on the back of platform services.

Micro-services, AI model hosting, and IoT event streams require managed middleware that abstracts infrastructure yet preserves flexibility, positioning PaaS as the essential layer for rapid product cycles. SaaS uptake remains strong among HR, CRM, and ERP workloads, especially for mid-market firms seeking turnkey solutions. IaaS growth continues but at a tempered pace as abstraction layers climb the value chain.

ASEAN Cloud Computing Market is Segmented by Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Service Model (Infrastructure As A Service, Platform As A Service, and Software As A Service), Organization Size (Small and Medium Enterprises and Large Enterprises), End-User Industry (Manufacturing, Education, Retail, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC (Alphabet Inc.)

- Alibaba Cloud (Alibaba Group Holding Limited)

- Huawei Technologies Co., Ltd.

- Tencent Holdings Ltd.

- IBM Corporation

- Oracle Corporation

- Salesforce, Inc.

- SAP SE

- DigitalOcean Holdings, Inc.

- Rackspace Technology, Inc.

- VMware, Inc.

- Equinix, Inc.

- OVH Groupe SAS (OVHcloud)

- Cloudflare, Inc.

- Snowflake Inc.

- NetApp, Inc.

- Nutanix, Inc.

- Red Hat, Inc. (IBM)

- Fastly, Inc.

- Akamai Technologies, Inc.

- Workday, Inc.

- ServiceNow, Inc.

- Databricks Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated 5G roll-outs enabling edge-cloud convergence

- 4.2.2 Surge in ASEAN hyperscale data-center investments by Chinese providers

- 4.2.3 Government digital-economy masterplans boosting cloud adoption

- 4.2.4 Rising enterprise demand for scalable IT infrastructure

- 4.2.5 Cloud-native fintech growth in Indonesia and Vietnam

- 4.2.6 Sustainability incentives for renewable-powered cloud facilities

- 4.3 Market Restraints

- 4.3.1 Data residency and sovereignty regulations

- 4.3.2 Shortage of cloud-skilled workforce in Tier-2 markets

- 4.3.3 Cross-border connectivity and latency challenges

- 4.3.4 High total cost of private and hybrid deployments for SMEs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Pricing Model Analysis

- 4.8 Assessment of Macro-Economic Trends

- 4.8.1 Ongoing Digitalization in SMEs

- 4.8.2 Economic Growth in ASEAN Countries

- 4.9 Number of Data Centres Across ASEAN

- 4.10 Industry Attractiveness - Porter's Five Forces Analysis

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Buyers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes

- 4.10.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Service Model

- 5.2.1 Infrastructure as a Service (IaaS)

- 5.2.2 Platform as a Service (PaaS)

- 5.2.3 Software as a Service (SaaS)

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Education

- 5.4.3 Retail

- 5.4.4 Transportation and Logistics

- 5.4.5 Healthcare

- 5.4.6 BFSI

- 5.4.7 Telecom and IT

- 5.4.8 Government and Public Sector

- 5.4.9 Utilities

- 5.4.10 Other End-user Industries

- 5.5 By Country

- 5.5.1 Singapore

- 5.5.2 Thailand

- 5.5.3 Malaysia

- 5.5.4 Indonesia

- 5.5.5 Vietnam

- 5.5.6 Philippines

- 5.5.7 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC (Alphabet Inc.)

- 6.4.4 Alibaba Cloud (Alibaba Group Holding Limited)

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Tencent Holdings Ltd.

- 6.4.7 IBM Corporation

- 6.4.8 Oracle Corporation

- 6.4.9 Salesforce, Inc.

- 6.4.10 SAP SE

- 6.4.11 DigitalOcean Holdings, Inc.

- 6.4.12 Rackspace Technology, Inc.

- 6.4.13 VMware, Inc.

- 6.4.14 Equinix, Inc.

- 6.4.15 OVH Groupe SAS (OVHcloud)

- 6.4.16 Cloudflare, Inc.

- 6.4.17 Snowflake Inc.

- 6.4.18 NetApp, Inc.

- 6.4.19 Nutanix, Inc.

- 6.4.20 Red Hat, Inc. (IBM)

- 6.4.21 Fastly, Inc.

- 6.4.22 Akamai Technologies, Inc.

- 6.4.23 Workday, Inc.

- 6.4.24 ServiceNow, Inc.

- 6.4.25 Databricks Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment