PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035025

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035025

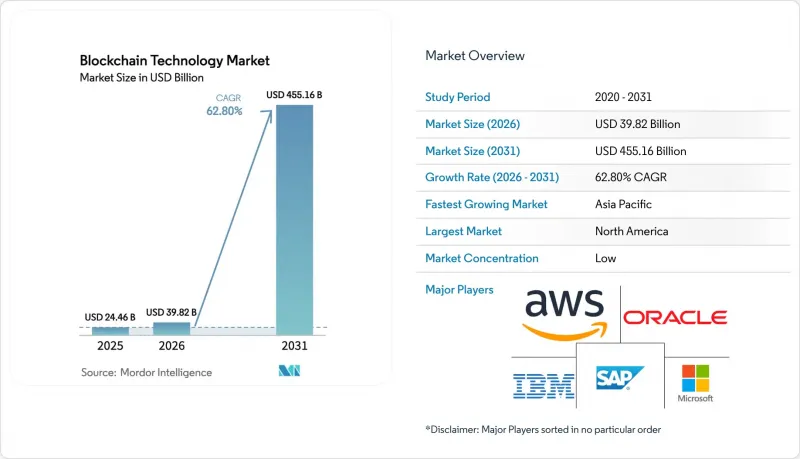

Blockchain Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Blockchain Technology Market size was valued at USD 24.46 billion in 2025 and estimated to grow from USD 39.82 billion in 2026 to reach USD 455.16 billion by 2031, at a CAGR of 62.8% during the forecast period (2026-2031).

Surging demand for tokenized assets, rapid enterprise migration toward Blockchain-as-a-Service (BaaS), and expanding use cases in supply-chain transparency and digital identity keep the growth curve steep. Public networks remain dominant for cross-industry traceability, whereas private and consortium chains draw corporations that must meet data sovereignty and regulatory mandates. Payment and remittance platforms maintain the broadest installed base, yet tokenization is now the fastest-scaling application as asset managers digitize traditional securities. Competition is intense but still fragmented, allowing partnerships between software giants and specialist vendors to set technical standards while enabling small providers to address niche vertical problems.

Global Blockchain Technology Market Trends and Insights

Rising Demand for End-to-End Supply-Chain Transparency

Global brands now view immutable traceability as mandatory for food safety, ESG reporting, and counterfeit mitigation. Walmart's food-safety pilot with IBM cut produce trace analysis from 7 days to 2.2 seconds, proving that blockchain can collapse compliance latency and operating risk. Manufacturers are integrating IoT sensors with distributed ledgers to build digital twins, triggering smart-contract rules that automate quality checkpoints and recall alerts. Regulatory pressure on Scope 3 emissions pushes procurement teams to demand real-time supplier disclosures, driving platform vendors to embed carbon-tracking modules. As transparency shifts from brand differentiator to legal requirement, on-chain product passports become the default audit mechanism across North America and Europe before cascading to Asia-Pacific exporters.

Rapid Adoption Across Financial Services

Tokenized deposits, wholesale CBDCs, and instant-settlement stablecoins redefine core banking workflows. BNY Mellon's Digital Asset Data Insights service processes on- and off-chain data for BlackRock's tokenized U.S. Treasury fund, demonstrating that frontline asset managers now treat blockchain as critical market infrastructure. By 2026, pilots in 20 economies will test CBDCs, reshaping monetary-policy plumbing and cross-border liquidity. Visa's e-HKD sandbox shows near-real-time settlement for retail payments, reducing interbank float costs. Remittance corridors stand to save USD 10 per transaction once smart-contract-based FX nets replace legacy correspondent banking. As regulatory frameworks such as the EU's MiCA mature, institutional treasurers gain the clarity necessary to hold on-chain cash equivalents, fueling demand spikes in permissioned payment rails.

Shortage of Skilled Blockchain Architects and Auditors

Rapid deployment outpaces workforce supply. Cryptography specialists, smart-contract auditors, and protocol designers remain scarce, particularly in Latin America, Southeast Asia, and Africa, where universities have yet to embed distributed-ledger modules. Global surveys show medium-sized banks delaying projects by up to 12 months while searching for certified talent. Cyber-security risk rises when inexperienced teams deploy production code, raising the value of external audit firms that can validate ZKP libraries and cross-chain bridges. Government-backed scholarship programs and vendor-hosted training aim to close gaps, but near-term bottlenecks could temper the blockchain technology market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Shift to BaaS Models

- Tokenization of U.S. Treasuries Creating Structural Demand

- Zero-Knowledge Proofs Enabling Privacy-Compliant Data Sharing

- Evolving and Fragmented Global Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Private chains are recording a 64.9% CAGR through 2031 as enterprises pursue controlled-access ledgers that dovetail with data-protection statutes and internal governance. Financial institutions use permissioned R3 Corda deployments for bilateral trade-finance and real-time gross settlement, restricting node participation to KYC-verified entities. Manufacturers form consortium blockchains so tier-two suppliers can append compliance certificates without broadcasting proprietary data to the open internet. Hybrid architectures bridge public transparency and private confidentiality; for example, shipment milestones post to Ethereum while sensitive bills of lading reside on a private side chain. Public networks still captured 51.35% share in 2025 because cryptocurrency activity and decentralized finance rely on global accessibility, yet the swing toward private deployments underscores enterprise comfort with walled-garden models for mission-critical operations.

Blockchain-native middleware now mediates interoperability between public proof-of-stake chains and private Byzantine Fault Tolerant networks, letting corporates settle tokens on open rails while anchoring confidential documents in permissioned stores. Regulatory sandboxes in Singapore and Abu Dhabi test cross-border data flows that vault hashes of trade certificates onto a public ledger, achieving auditability without disclosing commercial terms. As cross-chain bridges harden, chief information officers expect to toggle workloads between both environments, reinforcing the dual-track trajectory inside the broader blockchain technology market.

Cloud vendors that package consensus engines, validator orchestration, and key management into subscription bundles are swelling at a 64.7% CAGR. Oracle, IBM, Microsoft Azure, and Amazon Web Services pitch multi-tenant BaaS clusters where enterprises spin up nodes in minutes, sidestepping hardware procurement and talent shortages. Pay-per-use pricing reduces up-front costs, allowing start-ups to field proofs-of-concept with minimal risk. At the same time, traditional on-premises platforms and fully custom solutions still generated 67.45% of 2025 revenue because heavily regulated industries require bespoke integrations into mainframe, SAP, and high-availability environments.

Vendor convergence is evident as BaaS providers embed low-code workflow builders while established platform vendors expose managed hosting tiers. Enterprises evaluate offerings on audit readiness, throughput, and SLA terms rather than raw cryptographic horsepower. As security modules integrate hardware security modules and confidential-compute enclaves, BaaS could become the enterprise default, leveling the field for SMEs and pushing the blockchain technology market toward consumption-based economics.

The Blockchain Technology Market Report is Segmented by Type (Public, Private, and More), Component (Platform / Solution and Blockchain-As-A-Service (BaaS)), Application (Payments and Remittances, Smart Contracts, and More), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End User (BFSI, Transport and Logistics, and More), and Geography.

Geography Analysis

North America owns 34.05% of global revenue in 2025 thanks to early enterprise pilots, venture funding density, and a maturing policy environment. The FDIC's 2025 directive permits banks to undertake crypto-related activities without individualized approvals, accelerating blockchain deployments in custodial services, trade finance, and wealth management. Canada complements U.S. growth through supply-chain transparency projects in agriculture and mining, whereas Mexico trials cross-border payroll platforms to lower remittance costs for expatriate workers.

Asia-Pacific is the fast-track region, expanding at a 63.4% CAGR as governments embed blockchain into national digital-economy blueprints. China pledged USD 54.5 billion for multi-industry blockchain rollouts, including tax rebates, smart-city logistics, and intellectual-property registries. Japan and South Korea run stablecoin sandboxes tied to real-time gross settlement, while India's Unified Payments Interface layers pilot decentralized identity to increase financial inclusion. Australia's commodity exporters bolt traceability tokens to iron-ore shipments, and Singapore's Project Orchid experiments with programmable money for tourism vouchers.

Europe advances on the back of the fully operational MiCA framework, providing harmonized crypto-asset rules across member states. Germany's automotive supply base logs parts provenance, the Netherlands tests blockchain for harbor customs clearance, and Nordic utilities tokenize renewable energy certificates to satisfy Green Deal reporting. Still, rigorous disclosure requirements raise compliance costs for start-ups, nudging them toward BaaS providers that bake in regulatory tooling. The region's emphasis on privacy turbocharges adoption of zero-knowledge proof extensions, giving EU enterprises a head start in data-sovereignty-sensitive deployments within the blockchain technology market.

- IBM

- Microsoft

- Amazon Web Services (AWS)

- Oracle

- SAP SE

- Accenture

- Infosys

- NTT Data

- Intel

- ConsenSys

- R3

- Ripple Labs

- Chainalysis

- Fireblocks

- Bitfury

- Guardtime

- Hyperledger Foundation

- Polygon Labs

- Hedera Hashgraph

- Cegeka

- PixelPlex

- LimeChain

- Accubits Technologies

- SoluLab

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for end-to-end supply-chain transparency

- 4.2.2 Rapid adoption across financial services (tokenized deposits, CBDCs)

- 4.2.3 Enterprise shift to BaaS to cut cap-ex and time-to-market

- 4.2.4 Tokenization of U.S. Treasuries creating structural demand pools

- 4.2.5 Zero-knowledge proofs enabling privacy-compliant data sharing

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled blockchain architects and auditors

- 4.3.2 Evolving and fragmented global regulations

- 4.3.3 ESG backlash on energy-intensive consensus models

- 4.3.4 Interoperability gaps across layer-1 and layer-2 networks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Public

- 5.1.2 Private

- 5.1.3 Consortium

- 5.1.4 Hybrid

- 5.2 By Component

- 5.2.1 Platform / Solution

- 5.2.2 Blockchain-as-a-Service (BaaS)

- 5.3 By Application

- 5.3.1 Payments and Remittances

- 5.3.2 Smart Contracts

- 5.3.3 Supply-Chain and Traceability

- 5.3.4 Digital Identity and Credentialing

- 5.3.5 Internet-of-Things Integration

- 5.3.6 Tokenization / Asset Management

- 5.3.7 Others

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End User

- 5.5.1 BFSI

- 5.5.2 Transport and Logistics

- 5.5.3 Energy and Utilities

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Government and Public Sector

- 5.5.7 IT and Telecommunications

- 5.5.8 Real Estate and Construction

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Italy

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM

- 6.4.2 Microsoft

- 6.4.3 Amazon Web Services (AWS)

- 6.4.4 Oracle

- 6.4.5 SAP SE

- 6.4.6 Accenture

- 6.4.7 Infosys

- 6.4.8 NTT Data

- 6.4.9 Intel

- 6.4.10 ConsenSys

- 6.4.11 R3

- 6.4.12 Ripple Labs

- 6.4.13 Chainalysis

- 6.4.14 Fireblocks

- 6.4.15 Bitfury

- 6.4.16 Guardtime

- 6.4.17 Hyperledger Foundation

- 6.4.18 Polygon Labs

- 6.4.19 Hedera Hashgraph

- 6.4.20 Cegeka

- 6.4.21 PixelPlex

- 6.4.22 LimeChain

- 6.4.23 Accubits Technologies

- 6.4.24 SoluLab

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment