PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035026

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035026

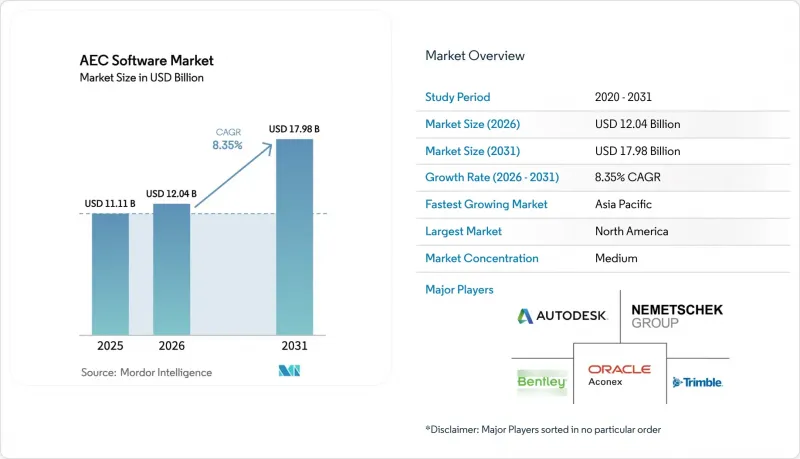

AEC Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The AEC software market size is expected to grow from USD 11.11 billion in 2025 to USD 12.04 billion in 2026 and is forecast to reach USD 17.98 billion by 2031 at 8.35% CAGR over 2026-2031.

This expansion reflects an acceleration in the construction sector's digital transformation as infrastructure programs in new megacities converge with government rules that make Building Information Modeling compulsory on public contracts. Falling cloud-hosting costs allow small and medium enterprises to adopt sophisticated design, modeling, and project-management systems, while generative-AI tools shorten iteration cycles and inspire platform vendors to consolidate feature sets. In parallel, owners' preference for single-source data environments is pushing vendors to weave together formerly separate design, construction, and operations modules, opening fresh routes to recurring revenue through subscription bundles that expand the addressable client base of the AEC software market.

Global AEC Software Market Trends and Insights

Infrastructure Boom in Emerging Megacities

Public authorities in Asia-Pacific are channeling record budgets into transport hubs, prefabricated housing, and district-scale smart utilities, intensifying demand for advanced modeling applications that can coordinate hundreds of subcontractors at once. China's 14th Five-Year Plan funnels capital toward new urban clusters, while India's Smart Cities Mission favors BIM-ready documentation on all tender packages. Singapore's Building and Construction Authority already stipulates BIM submissions on public projects valued above SGD 5 million, setting a compliance benchmark for regional neighbors. Because megacity programs combine rail, utilities, and vertical construction, the AEC software market benefits from bundled licenses that cover design authoring, clash detection, and digital twin handover in a single platform instance. Contractors that historically relied on 2-D CAD now migrate to parametric modeling in order to secure prequalification, creating a multiplier effect for the AEC software market as each flagship scheme triggers follow-on technology purchases among tier-two suppliers. International vendors partly localize user interfaces and code libraries to capture this wave, but competition from indigenous brands remains vigorous, sustaining price transparency and spurring feature innovation.

Mandated BIM Use in Public-Sector Projects

Across advanced economies, voluntary BIM guidance has evolved into enforceable procurement policy. The United Kingdom insists on BIM Level 2 deliverables across all centrally funded works, while the US General Services Administration extends similar provisions to federal jobs above USD 750,000. Eastern European transport ministries incorporate BIM clauses into EU-backed modernization tenders, creating uniform purchase triggers for software vendors. These regulations guarantee a predictable core of annual demand because compliance is not discretionary, driving stable license renewals and service contracts that underpin long-term revenue visibility for the AEC software market. They also set a hurdle that smaller niche suppliers often struggle to clear, thereby supporting moderate consolidation as certified multiproduct vendors fill the vacuum. The standardization of information-management protocols, moreover, accelerates cloud platform conversion because public owners increasingly accept SaaS hosting once data security requirements are codified in contractual language.

Talent Gap in Advanced Modeling

Many contractors purchase licenses yet fall short of capturing productivity gains because they lack staff adept at parametric authoring, 4-D sequencing, or AI-assisted clash resolution. Autodesk's 2024 State of Design and Make Report shows 56% of surveyed firms listing advanced modeling as their foremost recruitment pain point. Pay premiums of 15%-25% for BIM talent inflate project costs and dilute the return on software investment, especially among SMEs that cannot match corporate salary budgets. Training pipelines need six months or more to elevate Revit or Tekla novices to job-ready proficiency, delaying vendor revenue recognition tied to active-use metrics. Although cloud-hosted learning portals shorten ramp-up times, the underlying demographic shortfall remains a medium-term headwind for the AEC software market.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Affordability for SMEs

- Consolidation of Design-Build Data Platforms

- Inter-Suite Data-Exchange Friction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software licenses remained the primary revenue driver in 2024, yet the services slice is enlarging swiftly because clients want workflow mapping, template creation, and custom API scripting that help realize the full utility of purchased code. Services grew 10.85% annually, outpacing the overall AEC software market and reinforcing the thesis that digital transformation is more about disciplined process change than tool acquisition. Hybrid "software-plus-managed services" bundles are gaining traction, giving vendors recurring income tied to measurable productivity targets rather than unit shipments. Bentley Systems' 2024 expansion of its professional-services arm targets precisely this consultative vacuum. In parallel, software publishers embed self-service wizards into their flagship platforms to standardize best practice, but larger owners still prefer white-glove configuration, leaving room for integrators and specialist consultancies. Because implementation engagements often trigger add-on module sales, the service momentum generates a virtuous expansion loop for the AEC software market.

A rising proportion of service revenue comes from digital-twin upkeep, security audits, and AI model retraining, tasks that persist long after the initial project phase concludes. Vendors with credible service depth can negotiate enterprise frameworks that align license renewals to operational performance indices, anchoring clients for multiyear terms. This stickiness curbs churn and underpins valuation multiples for publicly listed platforms. Consequently, private equity investors exhibit growing interest in service-heavy targets as a hedge against potential licensing downcycles once the AEC software industry reaches maturity.

Cloud installations held 59.70% of 2025 spending and are forecast to grow at 10.25% CAGR, eclipsing on-premises setups that persist in heavily regulated asset classes such as defense. Work-from-anywhere norms that crystallized during the 2020-2021 pandemic accelerated SaaS uptake and permanently altered user expectations on version parity and simultaneous editing. Procore's double-digit revenue expansion in early 2025 illustrates how site managers view browser-based dashboards as integral to day-to-day jobsite control. The incremental shift toward cloud also changes cost structure: instead of lumpy capital purchases, firms accrue predictable monthly fees, smoothing cash-flow forecasting, and freeing capital for other project investments.

Further, cloud data hubs enable real-time IoT sensor ingestion and AI-driven pattern detection, features difficult to replicate in siloed on-premises silos. Governments are gradually certifying SaaS for public contracts, provided vendors meet sovereign-hosting or encryption stipulations, thus eliminating a final barrier to ubiquitous cloud penetration. As legacy license models decline, the proportion of subscription income within the AEC software market size figure will swell, making recurring revenue the dominant trajectory in vendor P&L's by the decade's close.

AEC Software Market is Segmented by Product (Software and Services), Deployment (On-Premises and Cloud), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Discipline (Architecture, Engineering, and Construction), Application (Design and Modelling, Project/Construction Management, and Asset and Facility Management), End-User (Design-Consultancies, EPC Contractors, and Owners/Developers), and Geography.

Geography Analysis

North America generated 37.90% of global revenue in 2025 owing to mature BIM mandates, stable public-infrastructure budgets, and deep pools of digitally trained labor. State and federal agencies regularly embed Level of Development requirements into tender packages, making compliance tools non-negotiable. Cloud adoption is comparatively advanced as data-hosting providers meet FedRAMP and DoD IL-4 standards, encouraging municipal owners to switch from on-premises vaults to SaaS repositories without extended waiver processes. Tight labor markets, however, push firms to invest in AI-assisted design to offset staffing shortages, ensuring continuous license expansion even in established organizations.

Asia-Pacific emerges as the fastest-growing region at an 10.70% CAGR through 2031. China's national push for modular construction techniques calls for firm integration between design software and off-site manufacturing execution, rewarding vendors that support parametric modules readily convertible to CNC code. India's metro and airport sprees amplify demand for centrally hosted coordination hubs where dozens of subcontractors overlap schedules. Local brands such as PKPM compete through domestic code libraries and Chinese-language support, but international vendors defend share by localizing content packs and forging joint ventures with provincial planning institutes. The region's SME surge further diversifies client profiles, compelling publishers to offer tiered pricing in local currencies to capture volumes in secondary cities.

Europe maintains a steady mid-single-digit growth trajectory anchored by the EU Green Deal and circular-economy legislation that requires whole-life carbon analysis during permitting. Germany's Building Energy Act compels energy simulations in new builds, prompting widespread purchase of daylight-analysis and HVAC-sizing modules. Cross-border rail and power-interconnect projects also build momentum for open data exchange, pressuring vendors to enhance Industry Foundation Class support or risk exclusion from EU procurement qualification. While the continent's market is smaller than North America's in absolute terms, its regulatory rigor sets interoperability benchmarks that ripple outward to global product roadmaps, influencing feature-set decisions across the entire AEC software market.

- Autodesk Inc.

- Nemetschek SE

- Trimble Inc.

- Bentley Systems Inc.

- Oracle Corp. (Aconex)

- Procore Technologies Inc.

- Dassault Systemes SE

- Hexagon AB

- AVEVA Group plc

- ANSYS Inc.

- Bluebeam Inc.

- Graphisoft SE

- Bricsys NV

- RIB Software GmbH

- Sage Group plc

- Vectorworks Inc.

- PlanGrid Inc.

- Viewpoint Inc.

- Tekla Corp.

- Allplan GmbH

- Synchro Software Ltd.

- Revizto Group

- Cohesive Companies

- Asite Solutions Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure boom in emerging megacities

- 4.2.2 Mandated BIM use in public?sector projects

- 4.2.3 Cloud affordability for SMEs

- 4.2.4 Consolidation of design-build data platforms

- 4.2.5 Generative-AI-driven carbon-optimal design

- 4.2.6 Digital-twin O&M cost-savings proof-points

- 4.3 Market Restraints

- 4.3.1 Talent gap in advanced modelling

- 4.3.2 Inter-suite data-exchange friction

- 4.3.3 Cyber-security/IP liability on multitenant clouds

- 4.3.4 Antitrust scrutiny of de-facto monopolies

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Sustainability and Circularity Outlook

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Discipline

- 5.4.1 Architecture

- 5.4.2 Engineering

- 5.4.3 Construction

- 5.5 By Application

- 5.5.1 Design and Modelling

- 5.5.2 Project/Construction Management

- 5.5.3 Asset and Facility Management

- 5.6 By End-user

- 5.6.1 Design-Consultancies

- 5.6.2 EPC Contractors

- 5.6.3 Owners/Developers

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Singapore

- 5.7.4.6 Malaysia

- 5.7.4.7 Australia

- 5.7.4.8 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Autodesk Inc.

- 6.4.2 Nemetschek SE

- 6.4.3 Trimble Inc.

- 6.4.4 Bentley Systems Inc.

- 6.4.5 Oracle Corp. (Aconex)

- 6.4.6 Procore Technologies Inc.

- 6.4.7 Dassault Systemes SE

- 6.4.8 Hexagon AB

- 6.4.9 AVEVA Group plc

- 6.4.10 ANSYS Inc.

- 6.4.11 Bluebeam Inc.

- 6.4.12 Graphisoft SE

- 6.4.13 Bricsys NV

- 6.4.14 RIB Software GmbH

- 6.4.15 Sage Group plc

- 6.4.16 Vectorworks Inc.

- 6.4.17 PlanGrid Inc.

- 6.4.18 Viewpoint Inc.

- 6.4.19 Tekla Corp.

- 6.4.20 Allplan GmbH

- 6.4.21 Synchro Software Ltd.

- 6.4.22 Revizto Group

- 6.4.23 Cohesive Companies

- 6.4.24 Asite Solutions Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment