PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035043

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035043

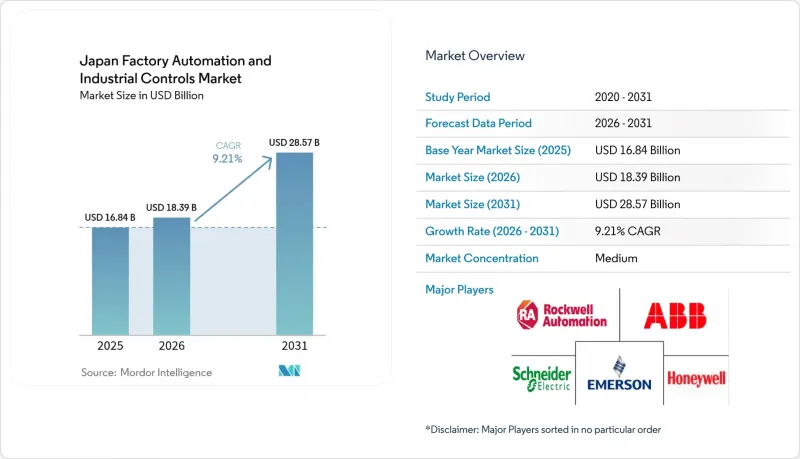

Japan Factory Automation And Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan factory automation and industrial controls market size was valued at USD 16.84 billion in 2025 and estimated to grow from USD 18.39 billion in 2026 to reach USD 28.57 billion by 2031, at a CAGR of 9.21% during the forecast period (2026-2031).

Momentum stems from a shrinking labor pool, aggressive decarbonization rules, and unprecedented fiscal incentives that are compressing payback cycles for next-generation robotics, distributed control systems, and edge-computing platforms. Energy-efficiency benchmarks introduced under the amended Energy Conservation Act, combined with the JPY 150 trillion Green Transformation Fund, are steering budgets toward integrated hardware-plus-software packages that guarantee measurable CO2 cuts. Manufacturers also face rising wage inflation, cybersecurity requirements tied to OPC UA over TSN deployments, and a renewed urgency to localize semiconductor supply, all of which heighten demand for turnkey consulting and predictive-maintenance services. Competitive intensity is rising as domestic incumbents open their ecosystems while European suppliers differentiate through subscription analytics, tilting revenue models away from transactional hardware toward annuity-based service contracts

Japan Factory Automation And Industrial Controls Market Trends and Insights

Carbon-Neutrality Mandates And Energy-Efficiency Regulations

Japan's 2023 Energy Conservation Act revision obliges factories that consume at least 1,500 kiloliters of crude oil equivalent annually to benchmark energy intensity or face fines, which is channeling budgets into variable-frequency drives, regenerative conveyors, and real-time energy-management suites from Schneider Electric and Siemens. The 2024 amendment broadened the scope to Scope 3 emissions, forcing tier-1 automotive suppliers to audit subcontractor footprints and sparking PLC retrofits across second-tier metal shops in Aichi and Shizuoka. Yokogawa's OpreX Energy Management suite experienced a 340% increase in domestic installations during fiscal 2024, marking a shift from compliance spending to operational cost arbitrage.

Aging Workforce And Acute Labor Shortages

Japan's working-age population is expected to shrink by 580,000 in 2024, with projections indicating a 12% decline in manufacturing labor by 2030. Collaborative robots are plugging gaps: Fanuc's CRX-5iA, launched March 2024, enables fence-free assembly, while Omron's mobile-robot-plus-vision combo cut changeover time 40% on a Panasonic battery line. Rising base wages, up 3.6% in spring 2024 bargaining, have shortened payback on robotics to under 24 months in packaging and logistics, where Yaskawa's Motoman robots now outnumber humans in 60% of new warehouses.

High Upfront CAPEX For SMEs

SMEs account for 99.7% of manufacturers yet face debt-service ratios below thresholds required by regional banks, making a JPY 8 million PLC-plus-vision cell equal to 6-9 months of profit. While the Monozukuri subsidy covered 1,240 projects in fiscal 2024, approval rates slipped to 32%, forcing many SMEs to defer plans or seek costly lease options.

Other drivers and restraints analyzed in the detailed report include:

- Government's Society 5.0 / Connected Industries Program

- Robust Demand From Automotive And Electronics Verticals

- Semiconductor Supply-Chain Disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PLC solutions captured a 36.35% share of the Japan factory automation and industrial controls market in 2025 and MES is projected to accelerate at a 9.95% CAGR through 2031. Distributed control systems dominate process industries, where Yokogawa holds a 42% domestic share, while Mitsubishi Electric and Omron together control 60% of discrete PLC deployments.

The shift to soft PLCs and cloud historians is expanding the Japan factory automation and industrial controls market size for virtualized edge servers and digital twin platforms. Supervisory control and data acquisition platforms are moving into factories to satisfy real-time carbon reporting, and MES-PLM convergence is rising fastest in battery and semiconductor lines.

Hardware accounted for 58.12% of 2025 revenue; however, services revenue is growing at a rate of 10.41% per year, the fastest of any component segment. Robotics and machine vision shipped 26% more units in 2024, but OPC UA TSN rollouts, cloud historians, and predictive maintenance workloads are pushing integrators to the forefront.

This pivot is expanding the Japan factory automation and industrial controls market size for annual service contracts that bundle edge AI and cybersecurity monitoring. Hardware duopolies in drives and motors maintain pricing power, yet component-only suppliers risk margin erosion as buyers favor integrated energy-management packages.

The Japan Factory Automation and Industrial Controls Market Report is Segmented by System Type (DCS, PLC, SCADA, PLM, MES, HMI, and Other), Component (Hardware, Software, and Services), Factory Size (SME and Large Enterprises), and End-User Industry (Oil and Gas, Chemical, Power, Food and Beverage, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mitsubishi Electric Corporation

- Omron Corporation

- Fanuc Corporation

- Yokogawa Electric Corporation

- Siemens AG

- ABB Ltd.

- Schneider Electric SE

- Rockwell Automation, Inc.

- Honeywell International Inc.

- Emerson Electric Co.

- Yaskawa Electric Corporation

- Nidec Corporation

- Fuji Electric Co., Ltd.

- Seiko Epson Corporation

- Shibaura Machine Co., Ltd.

- Keyence Corporation

- Panasonic Holdings Corporation (Factory Solutions)

- SMC Corporation

- Hitachi Ltd. (Industrial Equipment Systems)

- Denso Corporation (Factory Automation)

- Advantech Co., Ltd.

- IAI Corporation

- Azbil Corporation

- Nachi-Fujikoshi Corp.

- Kawasaki Heavy Industries, Ltd. (Robotics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Carbon-Neutrality Mandates And Energy-Efficiency Regulations

- 4.2.2 Aging Workforce And Acute Labor Shortages

- 4.2.3 Government's Society 5.0 / Connected Industries Program

- 4.2.4 Robust Demand From Automotive And Electronics Verticals

- 4.2.5 Green-DX Subsidy Programme (GX Fund) Accelerates Automation

- 4.2.6 Rapid Piloting Of OPC UA Over TSN For Shop-Floor Interoperability

- 4.3 Market Restraints

- 4.3.1 High Upfront CAPEX For SMEs

- 4.3.2 Semiconductor Supply-Chain Disruptions

- 4.3.3 Cyber-Security Skill Gap For OT/IT Convergence

- 4.3.4 Conservative Culture Slowing Cloud-Native Control Adoption

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By System Type

- 5.1.1 Distributed Control System (DCS)

- 5.1.2 Programmable Logic Controller (PLC)

- 5.1.3 Supervisory Control and Data Acquisition (SCADA)

- 5.1.4 Product Lifecycle Management (PLM) Software

- 5.1.5 Manufacturing Execution System (MES)

- 5.1.6 Human-Machine Interface (HMI)

- 5.1.7 Other System Types

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Machine Vision

- 5.2.1.2 Industrial Robotics

- 5.2.1.3 Sensors and Transmitters

- 5.2.1.4 Motors and Drives

- 5.2.1.5 Safety Systems

- 5.2.1.6 Other Hardwares

- 5.2.2 Software

- 5.2.3 Services (Integration, Consulting, Maintenance)

- 5.2.1 Hardware

- 5.3 By Factory Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Power and Utilities

- 5.4.4 Food and Beverage

- 5.4.5 Automotive and Transportation

- 5.4.6 Electronics and Semiconductor

- 5.4.7 Pharmaceuticals

- 5.4.8 Metals and Mining

- 5.4.9 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mitsubishi Electric Corporation

- 6.4.2 Omron Corporation

- 6.4.3 Fanuc Corporation

- 6.4.4 Yokogawa Electric Corporation

- 6.4.5 Siemens AG

- 6.4.6 ABB Ltd.

- 6.4.7 Schneider Electric SE

- 6.4.8 Rockwell Automation, Inc.

- 6.4.9 Honeywell International Inc.

- 6.4.10 Emerson Electric Co.

- 6.4.11 Yaskawa Electric Corporation

- 6.4.12 Nidec Corporation

- 6.4.13 Fuji Electric Co., Ltd.

- 6.4.14 Seiko Epson Corporation

- 6.4.15 Shibaura Machine Co., Ltd.

- 6.4.16 Keyence Corporation

- 6.4.17 Panasonic Holdings Corporation (Factory Solutions)

- 6.4.18 SMC Corporation

- 6.4.19 Hitachi Ltd. (Industrial Equipment Systems)

- 6.4.20 Denso Corporation (Factory Automation)

- 6.4.21 Advantech Co., Ltd.

- 6.4.22 IAI Corporation

- 6.4.23 Azbil Corporation

- 6.4.24 Nachi-Fujikoshi Corp.

- 6.4.25 Kawasaki Heavy Industries, Ltd. (Robotics)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment