PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035050

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035050

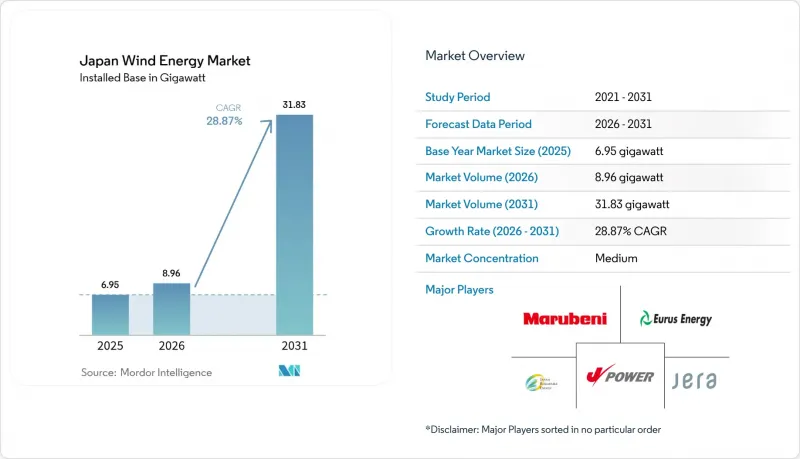

Japan Wind Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Japan Wind Energy Market size in 2026 is estimated at 8.96 gigawatt, growing from 2025 value of 6.95 gigawatt with 2031 projections showing 31.83 gigawatt, growing at 28.87% CAGR over 2026-2031.

Growth rests on Japan's policy commitment to curb fossil-fuel dependence and achieve carbon neutrality by 2050, supported by the 7th Strategic Energy Plan that targets 40-50% renewables in the national power mix by 2040. Offshore wind auctions, sovereign transition bonds, and corporate power-purchase agreements (PPAs) channel new capital, while domestic component alliances reduce import risks and shorten project timelines. Floating-platform breakthroughs enlarge the area available for development by a factor of ten, unlocking deeper waters for future capacity. At the same time, grid congestion in wind-rich northern regions and stakeholder opposition in fishing communities temper short-term installation rates.

Japan Wind Energy Market Trends and Insights

Surge in Offshore-Wind Auction Rounds

Round 3 auctions in December 2024 awarded 1 GW across Aomori South and Yuza at JPY 3/kWh with mandated start-up by June 2030. Revised auction rules in January 2025 introduced price-indexation and early-operation incentives to offset cost-inflation risk.These changes signal regulatory agility that preserves competitive pricing while broadening bidder participation. Round 4, slated for 2025, will test whether rule refinements can accelerate capacity awards without compromising local-content requirements. The approach positions auctions as a predictable growth engine for the Japan wind energy market.

Declining Onshore LCOE and Turbine Upgrades

The 147 MW Abukuma wind farm, commissioned in April 2025 with 46 GE Vernova 3.2 MW units, shows how larger turbines cut balance-of-plant costs per megawatt. Domestic switchgear and semiconductor tie-ups between Vestas, Mitsubishi Electric, and Fuji Electric deepen the supply chain and lower import exposure. NEDO-funded floating vertical-axis prototypes extend cost reductions into deep-water environments, supporting broader deployment. Together, these factors lift project internal rates of return and quicken the shift toward larger, more efficient machines, advancing the Japan wind energy market.

Grid Congestion & Curtailment Risk in Tohoku/Hokkaido

Renewable curtailment reached 1.76 TWh in FY 2023, with Kyushu recording a 6.7% rate. Wind-rich Hokkaido and Tohoku lie far from demand hubs, and high-voltage upgrades to Honshu will not finish before 2030. Priority dispatch for nuclear reactors squeezes available capacity in peak-wind seasons. Although Marubeni's 25 MW/103.7 MWh battery system in Hokkaido offers partial relief, statewide storage needs exceed 2 GW. Persistent congestion threatens revenue stability and delays financing for new entrants in the Japan wind energy market.

Other drivers and restraints analyzed in the detailed report include:

- Capital Inflows from Green-Bond Issuances

- Corporate PPAs from Data-Centre & Semiconductor Clusters

- Typhoon-Driven O&M Cost Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Offshore capacity is forecast to climb from a negligible base to roughly 12.1 GW by 2031, raising its Japan wind energy market share from 4.88% in 2025 to nearly 39% at the end of the decade. Round 3 awards totaling 1.065 GW cleared at grid-parity prices and specified 15 MW turbines that compress balance-of-system costs by roughly one-fifth. Commercial floating wind receives a legal boost from March 2025 EEZ legislation, which unlocks 150 GW of deep-water potential in the Sea of Japan and Pacific trenches.

Developers still prize onshore repowering opportunities: 1.2 GW of 1990s-era turbines can be swapped for 4-5 MW machines without adding new land footprints, and grid taps are already in place. Yet local moratoriums in Akita and Aomori and environmental reviews on migratory-bird routes hold the onshore pipeline at 800 MW. Offshore projects must contend with a domestic shortage of heavy-lift jack-up vessels; only 3 are available versus 25 in Europe, pushing developers to charter Korean or Chinese assets at premium day rates.

The Japan Wind Energy Market Report is Segmented by Location (Onshore and Offshore), Turbine Capacity (Less Than 3 MW, 3 To 6 MW, and Above 6 MW), and Application (Utility-Scale, Commercial and Industrial, and Community Projects). The Market Size and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Vestas A/S

- Siemens Gamesa Renewable Energy

- Mitsubishi Heavy Industries

- GE Vernova

- Hitachi Energy

- JERA

- Eurus Energy Holdings

- Electric Power Development (J-Power)

- Sumitomo Corp.

- Marubeni Corp.

- Japan Renewable Energy (JRE)

- Cosmo Eco Power

- Toshiba Energy Systems

- Pattern Energy Japan

- Northland Power Japan

- Orsted Japan

- RWE Renewables Japan

- BP Offshore Wind Japan

- Shell Japan Renewables

- Inpex Renewable Energy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in offshore-wind auction rounds

- 4.2.2 Declining onshore LCOE and turbine upgrades

- 4.2.3 Capital inflows from green-bond issuances

- 4.2.4 Corporate PPAs from data-centre & semiconductor clusters

- 4.2.5 Opening of Japan's EEZ for floating wind

- 4.2.6 National hydrogen-ammonia strategy boosting wind demand

- 4.3 Market Restraints

- 4.3.1 Gas-fired capacity additions under the GX roadmap

- 4.3.2 Grid congestion & curtailment risk in Tohoku/Hokkaido

- 4.3.3 Typhoon-driven O&M cost inflation

- 4.3.4 Fishery & local-stakeholder opposition delaying permits

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (floating foundations, 15-MW turbines)

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Location

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 By Turbine Capacity

- 5.2.1 Up to 3 MW

- 5.2.2 3 to 6 MW

- 5.2.3 Above 6 MW

- 5.3 By Application

- 5.3.1 Utility-scale

- 5.3.2 Commercial and Industrial

- 5.3.3 Community Projects

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Nacelle/Turbine

- 5.4.2 Blade

- 5.4.3 Tower

- 5.4.4 Generator and Gearbox

- 5.4.5 Balance-of-System

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Vestas A/S

- 6.4.2 Siemens Gamesa Renewable Energy

- 6.4.3 Mitsubishi Heavy Industries

- 6.4.4 GE Vernova

- 6.4.5 Hitachi Energy

- 6.4.6 JERA

- 6.4.7 Eurus Energy Holdings

- 6.4.8 Electric Power Development (J-Power)

- 6.4.9 Sumitomo Corp.

- 6.4.10 Marubeni Corp.

- 6.4.11 Japan Renewable Energy (JRE)

- 6.4.12 Cosmo Eco Power

- 6.4.13 Toshiba Energy Systems

- 6.4.14 Pattern Energy Japan

- 6.4.15 Northland Power Japan

- 6.4.16 Orsted Japan

- 6.4.17 RWE Renewables Japan

- 6.4.18 BP Offshore Wind Japan

- 6.4.19 Shell Japan Renewables

- 6.4.20 Inpex Renewable Energy

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Floating wind in deep-water EEZ blocks

- 7.3 Green-hydrogen coupling & coastal ammonia hubs

- 7.4 Repowering ageing onshore fleets (Greater than 20 yrs)

- 7.5 Co-location with battery storage & data centres