PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035055

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035055

Japan Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

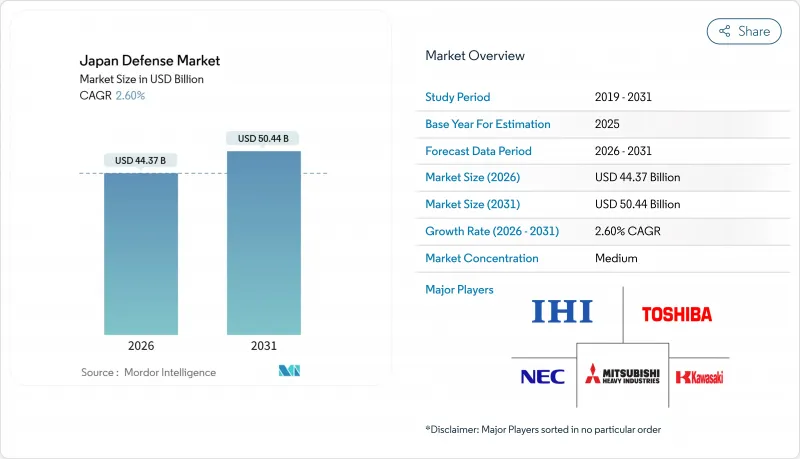

The Japan defense market size stands at USD 44.37 billion in 2026 and is projected to reach USD 50.44 billion by 2031, translating into a 2.6% CAGR across the forecast period.

Heightened threats from China and North Korea, Cabinet-endorsed spending that rises toward 2% of GDP, and an accelerated shift toward counter-strike capabilities are reshaping the Japan defense market in ways unseen since the Cold War. The growing procurement of hypersonic interceptors, the fielding of private 5G networks for real-time command, and deeper integration into multilateral programs such as GCAP, as well as a prospective AUKUS Pillar II foothold, all broaden the market's technology base. Foreign Military Sales remain indispensable for high-end systems even as yen weakness inflates dollar-denominated contracts, making cost-share partnerships more attractive. Domestic primes continue to capture sovereign programs, yet a wave of smaller firms is winning niche awards in counter-drone and directed-energy applications, intensifying competition across the Japan defense market.

Japan Defense Market Trends and Insights

Heightened Security Risks In The Indo-Pacific Region

China executed 1,200 incursions into Japan's ADIZ during fiscal 2024, up 15%, while North Korea launched 23 ballistic missiles, some crossing Japanese airspace, prompting Tokyo to accelerate integrated air and missile defense architectures. The National Security Strategy, revised in 2022, identifies China as "the greatest strategic challenge," unlocking counter-strike options and underpinning a December 2024 purchase of 400 Tomahawk missiles. Taiwan-strait contingency planning places the Nansei chain at the front line, driving investments in hardened depots and distributed munitions. The sustained nature of these threats secures multi-year appropriations through 2031. Consequently, the Japan defense market records persistent demand for early-warning satellites, long-range fires, and mobile air-defense units.

Significant Increase In Long-Term Defense Spending Commitments

The FY2023-2027 plan allocates JPY 43 trillion (USD 272.34 billion), 56% above the prior quinquennium, backed by tax-linked financing that isolates the defense top line from annual fluctuations. Spending equal to 2% of GDP would increase annual outlays to JPY 11 trillion (USD 69.67 billion) by 2027. Institutional reforms, most notably the Acquisition, Technology & Logistics Agency, trimmed procurement lead times by 18 months and enabled serial production savings, as evidenced by a 12% per-hull cost drop for the Mogami-class frigate. These measures embed a funding trajectory that sustains the Japan defense market well into the 2030s.

High Public Debt Levels Constraining Long-Term Expansion

Government debt reached 264% of GDP in 2025, with debt service absorbing 23% of the general budget. Sustaining a 2% of GDP defense line post-2027 requires higher taxes or welfare cuts, both of which are politically delicate. Fitch revised Japan's outlook to negative in August 2024, warning of "limited fiscal space to absorb additional spending shocks". Although the current five-year program is funded, procurement beyond 2027 could be reduced, which would moderate growth in the Japan defense market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Advancement of Missile and Hypersonic Strike Capabilities

- Deepening Participation In Global Defense Collaboration Initiatives

- Environmental Pushback Against Base Development And Live-Fire Training

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Japanese Air Self-Defense Force (JASDF) is on course for a 5.67% CAGR through 2031, eclipsing ground and maritime growth. It fields 147 F-35s, integrates 400 Tomahawk missiles, and co-develops the GCAP fighter, with each program contributing to the development of the Japan defense market, which is allocated to air modernization. A KC-46A tanker fleet further extends reach beyond 2,000 km, while the Hypersonic Defense Unit anchors missile-defense resources in Okinawa.

The Army retained a 36.24% stake in 2025 but shifted from tank-centric formations to agile island-defense brigades, slowing Type-10 production to eight units annually. Maritime forces commission Taigei-class submarines equipped with Li-ion batteries, which double submerged endurance. These reallocations reinforce a balanced yet air-skewed Japan defense market.

Weapons and ammunition dominated the 2025 baseline at 32.11%; however, unmanned systems are set for a 7.32% CAGR, the swiftest ascent across categories. MQ-9B SeaGuardians deliver 30-hour patrol windows, while Subaru's VTOL drone advances carrier-based ISR, tightening the loop between sensors and shooters. These gains push the Japan defense market toward autonomous operations.

C4ISR and EW enjoy steady inflows as private 5G and AI-powered fusion platforms proliferate. Personnel training and protection receive VR simulators and upgraded body armor, though their share remains modest. Space and cyber systems, buoyed by QZSS satellite launches, contribute incremental yet strategic value to the broader Japan defense market.

The Japan Defense Market Report is Segmented by Armed Forces (Air Force, Army, Navy, and Space Force), Type (Personnel Training and Protection, C4ISR and Electronic Warfare, Vehicles, Weapons and Ammunition, Unmanned Systems, and More), Domain (Land, Air, Naval, Space, and More), and Procurement Nature (Indigenous Production and Foreign Procurement). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mitsubishi Heavy Industries, Ltd.

- Kawasaki Heavy Industries, Ltd.

- IHI AEROSPACE Co., Ltd.

- ShinMaywa Industries, Ltd.

- Japan Steel Works, Ltd.

- SUBARU CORPORATION

- NEC Corporation

- Toshiba Corporation

- Mitsubishi Electric Corporation

- Lockheed Martin Corporation

- The Boeing Company

- BAE Systems plc

- RTX Corporation

- Northrop Grumman Corporation

- Thales Group

- Leonardo S.p.A.

- L3Harris Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened security risks in the Indo-Pacific region

- 4.2.2 Significant increase in long-term defense spending commitments

- 4.2.3 Rapid advancement of missile and hypersonic strike capabilities

- 4.2.4 Deepening participation in global defense collaboration initiatives

- 4.2.5 Demographic pressures fueling growth in autonomous and unmanned systems

- 4.2.6 Deployment of private 5G networks across defense installations

- 4.3 Market Restraints

- 4.3.1 High public debt levels constraining long-term budget expansion

- 4.3.2 Limited industrial capacity and skilled workforce availability

- 4.3.3 Currency depreciation driving up import-related procurement costs

- 4.3.4 Environmental pushback against base development and live-fire training

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Armed Forces

- 5.1.1 Air Force

- 5.1.2 Army

- 5.1.3 Navy

- 5.2 By Type

- 5.2.1 Personnel Training and Protection

- 5.2.2 C4ISR and Electronic Warfare (EW)

- 5.2.3 Vehicles

- 5.2.4 Weapons and Ammunition

- 5.2.5 Unmanned Systems

- 5.2.6 Space and Cyber Systems

- 5.3 By Domain

- 5.3.1 Land

- 5.3.2 Air

- 5.3.3 Naval

- 5.3.4 Space

- 5.3.5 Cyber and Electromagnetic Spectrum

- 5.4 By Procurement Nature

- 5.4.1 Indigenous Production

- 5.4.2 Foreign Procurement

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mitsubishi Heavy Industries, Ltd.

- 6.4.2 Kawasaki Heavy Industries, Ltd.

- 6.4.3 IHI AEROSPACE Co., Ltd.

- 6.4.4 ShinMaywa Industries, Ltd.

- 6.4.5 Japan Steel Works, Ltd.

- 6.4.6 SUBARU CORPORATION

- 6.4.7 NEC Corporation

- 6.4.8 Toshiba Corporation

- 6.4.9 Mitsubishi Electric Corporation

- 6.4.10 Lockheed Martin Corporation

- 6.4.11 The Boeing Company

- 6.4.12 BAE Systems plc

- 6.4.13 RTX Corporation

- 6.4.14 Northrop Grumman Corporation

- 6.4.15 Thales Group

- 6.4.16 Leonardo S.p.A.

- 6.4.17 L3Harris Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment