PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035069

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035069

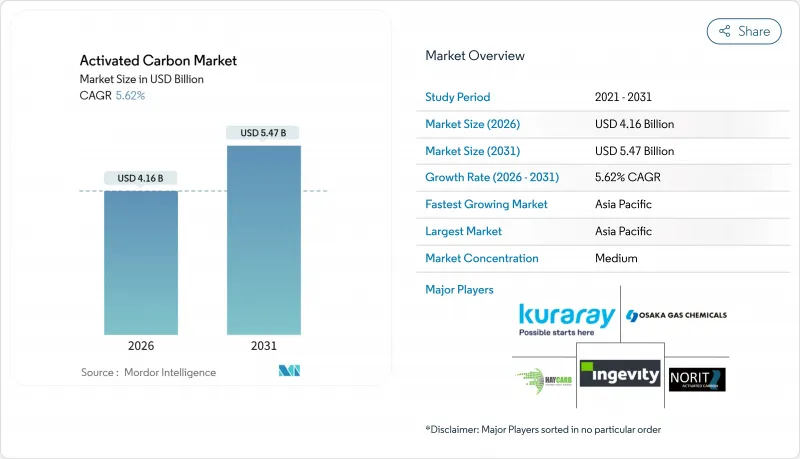

Activated Carbon - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Activated Carbon Market size is estimated at USD 4.16 billion in 2026, and is expected to reach USD 5.47 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031).

Tightening water-quality regulations, the rollout of nationwide PFAS remediation programs, and mercury-removal mandates at coal-fired plants are central to this expansion. The U.S. Environmental Protection Agency's 2024 rule set parts-per-trillion limits for six PFAS compounds, prompting a wave of granular activated carbon (GAC) retrofits across hundreds of utilities. Concurrently, large sugar, chemical, and refining operators are investing in solvent-recovery circuits that rely on high-performance carbons, while municipal buyers strengthen long-term offtake agreements to secure supply. Operators are also shifting from single-use powdered activated carbon (PAC) toward GAC coupled with regional reactivation hubs to cut lifecycle costs. In Asia-Pacific, abundant coal feedstock and expanding coconut-shell charcoal exports keep new capacity online, yet feedstock price swings and weather-driven harvest shocks continue to complicate procurement strategies.

Global Activated Carbon Market Trends and Insights

Growing Demand for Water Purification

Regulators worldwide continue to ratchet down allowable contaminant thresholds, driving unprecedented investment in high-capacity GAC filters. The EPA's PFAS rule alone is forcing hundreds of U.S. utilities to lock in multi-year supply contracts, such as American Water's ten-state deal with Calgon Carbon. European utilities face similar pressure under the updated Drinking Water Directive, while Indian and Chinese municipalities accelerate capacity to meet population-driven demand. The preference is shifting from PAC toward regenerable GAC systems, as operators weigh long-term disposal liabilities against higher up-front capital outlays. Suppliers able to guarantee both virgin supply and reactivation services enjoy a competitive advantage as utilities prioritize circular procurement frameworks.

Mercury-Removal Mandates for Coal-Fired Plants

Revised Mercury and Air Toxics Standards in the United States, coupled with comparable rules in China and India, are reinforcing demand for powdered and impregnated carbons designed for flue-gas injection. Although portions of the coal fleet are retiring, remaining units must upgrade capture systems, sustaining a durable, if regionally uneven, order pipeline. Japan's strict emission controls add a steady baseline demand despite the country's broader decarbonization push. Suppliers specializing in brominated or halogenated grades secure premium margins thanks to the technical complexity of long-duration mercury capture.

Supply-Chain Disruption for Coconut-Shell Charcoal

Weather-related harvest shocks, coupled with export restrictions and competition from alternatives like briquettes, have led to a tightening of coconut-shell charcoal supplies. In 2024, Indonesia saw its exports drop in volume and value. This decline caused prices to surge. In North America and Europe, buyers contended with longer lead times and heightened costs, especially since PFAS removal standards leaned towards coconut-shell grades. While producers are branching out into wood, peat, and low-rank coal precursors, these substitutes fall short in micropore distribution, which is crucial for effective trace-contaminant adsorption. As a result, adept feedstock risk management has emerged as a key differentiator in extensive, multi-year utility tenders.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Low-Sulphur Fuel Regulations Boosting Solvent Recovery

- Increasing Biogas Upgrading and H2S Scrubbing at Small-Scale Plants

- Coal-Price Volatility Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coal-derived products retained 43.18% of the activated carbon market share in 2025 because of their favorable cost structure and extensive supply footprints in China, India, and the United States. Coconut-shell-based carbons, while smaller in tonnage, are projected to expand at a 6.78% CAGR as regulators and high-purity users favor their ultrafine micropore network for PFAS and pharmaceutical removal. The activated carbon market size for coconut-shell grades is therefore expected to outpace every other raw-material category through 2031. Feedstock diversification, including pilot work on peat and lignite, is accelerating as suppliers hedge against both coal and coconut price swings.

Producers with multi-feedstock portfolios demonstrated greater resilience during the 2024-2025 coconut-shell shortfall, maintaining contractual volumes by switching to chemically activated wood or low-rank coal blends. Technical papers published in 2024 showed successful ilmenite- and iron-oxide-assisted activation of lignite, yielding iodine numbers comparable to premium coconut carbons. End-use buyers increasingly evaluate lifecycle greenhouse-gas profiles, pushing suppliers to quantify emission intensity across precursor sourcing, activation energy, and reactivation cycles. Coal will remain dominant in cost-sensitive municipal tenders, yet coconut-shell and wood grades are positioned to capture value-added niches where adsorption performance outweighs unit price.

PAC represented 47.86% of the activated carbon market size in 2025, anchored in large-volume sugar, beverage, and batch water-treatment applications that value fast kinetics and straightforward dosing. GAC, however, is forecast to grow at a 6.30% CAGR as utilities embrace on-site or regional reactivation to trim the total cost of ownership. Major suppliers secured permits for new furnaces in Sweden, France, and the U.S. Gulf Coast, underpinning a regional circular economy that reduces haul-back distances and Scope 3 emissions. The activated carbon market sees extruded and pelletized shapes gaining share in flue-gas and automotive evaporative-emission control, where high mechanical strength and low pressure drop are essential.

Lifecycle economics favor GAC, tipping more municipal bidders toward regenerable systems. PAC remains entrenched in sugar decolorization and intermittent batch uses where spent media disposal aligns with existing sludge management practices. Hybrid strategies are emerging: plants dose PAC for shock-load events while maintaining base-flow GAC beds, enabling compliance flexibility without overcapitalizing reactivation assets. Suppliers leveraging both PAC and GAC portfolios can therefore align with diverse customer risk appetites and cash-flow constraints.

The Activated Carbon Market Report is Segmented by Raw Material (Coal-Based, Coconut-Shell-Based, Wood-Based, and Other), Form (Powdered, Granular, and Extruded/Pelletised), Application (Decolorisation, Sugar Production, Concentration, Solvent Recovery, and More), End-User (Water Treatment, Industrial Processing, and More), and Geography (Asia-Pacific, North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 37.72% of 2025 revenue and is anticipated to post a 6.44% CAGR through 2031, driven by Chinese coal-to-carbon integration, India's burgeoning municipal buildout, and ASEAN's expanding coconut-shell charcoal exports. In 2024, Indian exporters boosted shipments of coconut-shell carbon, with notable exports flowing to the United States, Sri Lanka, and Belgium. Meanwhile, Chinese producers are harnessing coke-oven off-gases to cut down on activation energy costs. Despite wider decarbonization initiatives, Japanese utilities continue to show a strong demand for mercury-control carbons.

North America's activated carbon market is shaped by PFAS compliance and a decisive pivot toward domestic GAC capacity. Arq commissioned a line in Louisiana during 2025, marking the region's first vertically integrated virgin-carbon asset. Calgon Carbon expanded Gulf Coast reactivation capacity in 2024 and launched "Operation Bedrock" in 2025 to secure long-term supply for major utilities. Canadian and Mexican buyers benefit from shorter delivery lead times under continental trade agreements.

New reactivation hubs in France, Sweden, and the United Kingdom are cutting spent-carbon shipping distances, underscoring Europe's commitment to circularity. The revised Drinking Water Directive enforces PFAS group limits, prompting capital upgrades analogous to U.S. programs. Germany, Italy, Spain, and the Nordics add incremental demand from biogas upgrading and industrial VOC abatement. South America grows from a low base as Brazil and Argentina expand municipal networks, while the Middle East and Africa see early-stage adoption tied to desalination and gold-processing projects, though volumes remain modest relative to other regions.

- Albemarle Corporation

- Arq, Inc.

- Carbon Activated Corporation

- CarboTech

- Donau Carbon GmbH

- Haycarb PLC

- Ingevity

- KALPAKA Chemicals

- KURARAY CO., LTD.

- MICBAC India

- Nanping Yuanli Active Carbon Company

- Norit

- Osaka Gas Chemicals Co., Ltd.

- Puragen

- Rotocarb (PTY) Ltd.

- Shanghai Activated Carbon Co.,Ltd

- Silcarbon Aktivkohle GmbH

- Suneeta Carbons

- Xylem

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for water purification

- 4.2.2 Mercury-removal mandates for coal-fired plants

- 4.2.3 Surge in low-sulphur fuel regulations boosting solvent-recovery activated carbon

- 4.2.4 Increasing Bio-gas upgrading and H2S scrubbing at small-scale plants

- 4.2.5 Growing usage of activated carbon for air purification

- 4.3 Market Restraints

- 4.3.1 Supply-chain disruption for coconut shell charcoal

- 4.3.2 Coal-price volatility squeezing margins

- 4.3.3 High cap-ex for regional reactivation hubs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Raw Material

- 5.1.1 Coal-Based

- 5.1.2 Coconut-Shell-Based

- 5.1.3 Wood-Based

- 5.1.4 Other (Peat, Lignite, etc.)

- 5.2 By Form

- 5.2.1 Powdered Activated Carbon (PAC)

- 5.2.2 Granular Activated Carbon (GAC)

- 5.2.3 Extruded/Pelletised Activated Carbon (EAC)

- 5.3 By Application

- 5.3.1 Decolorisation Treatment

- 5.3.2 Sugar Production

- 5.3.3 Concentration Treatment

- 5.3.4 Solvent Recovery

- 5.3.5 PFAS Adsorption Treatment

- 5.3.6 Drinking Water Treatment

- 5.3.7 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Water Treatment

- 5.4.2 Industrial Processing

- 5.4.3 Healthcare

- 5.4.4 Food and Beverage

- 5.4.5 Automotive

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacifc

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 NORDIC Countries

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacifc

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles

- 6.4.1 Albemarle Corporation

- 6.4.2 Arq, Inc.

- 6.4.3 Carbon Activated Corporation

- 6.4.4 CarboTech

- 6.4.5 Donau Carbon GmbH

- 6.4.6 Haycarb PLC

- 6.4.7 Ingevity

- 6.4.8 KALPAKA Chemicals

- 6.4.9 KURARAY CO., LTD.

- 6.4.10 MICBAC India

- 6.4.11 Nanping Yuanli Active Carbon Company

- 6.4.12 Norit

- 6.4.13 Osaka Gas Chemicals Co., Ltd.

- 6.4.14 Puragen

- 6.4.15 Rotocarb (PTY) Ltd.

- 6.4.16 Shanghai Activated Carbon Co.,Ltd

- 6.4.17 Silcarbon Aktivkohle GmbH

- 6.4.18 Suneeta Carbons

- 6.4.19 Xylem

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Rising PFAS-remediation spend by utilities