PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035071

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035071

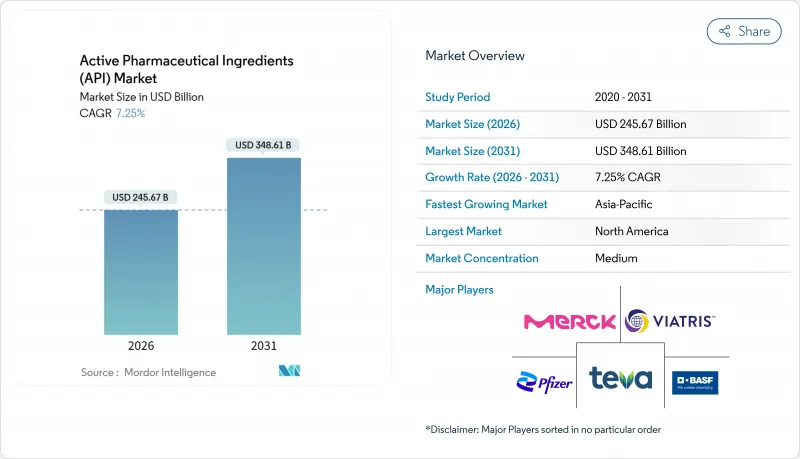

Active Pharmaceutical Ingredients (API) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Active Pharmaceutical Ingredients Market size is estimated at USD 245.67 billion in 2026, and is expected to reach USD 348.61 billion by 2031, at a CAGR of 7.25% during the forecast period (2026-2031).

Aging populations, the persistent rise of chronic illnesses, and surging biologics approvals keep demand strong, yet producer margins hinge on merchant manufacturing uptake, continuous-flow plant deployment, and on-shoring incentives in major economies. Governments in India, the United States, and the European Union disbursed more than USD 4 billion in combined Production Linked Incentive and tax-credit packages between 2024 and 2026, shifting new capacity toward domestic clusters. Contract development and manufacturing organizations (CDMOs) scaled faster than captives because continuous-flow and mini-plant technologies shorten cycle times and cut capital intensity for mid-volume APIs. Intensifying compliance rules, including nitrosamine testing and global GMP harmonization, temporarily raise costs but reinforce the case for larger, better-capitalized suppliers able to absorb regulatory overhead.

Global Active Pharmaceutical Ingredients (API) Market Trends and Insights

Escalating Chronic-Disease Drug Demand

Non-communicable diseases are forecast to increase global prescription volumes by 22% between 2025 and 2030, thereby amplifying baseline API requirements. Indian exports of statin and metformin APIs increased 14% year-over-year in 2025, as European wholesalers pre-built safety stocks. Oncology APIs for checkpoint inhibitors reached USD 12,000 per kilogram in merchant trade in 2025, nearly double the 2023 levels, highlighting the chronic-disease pull on premium molecules. Dedicated fermentation and synthesis lines are being added ahead of forecast demand, marking a departure from prior just-in-time practices. Sizable but uneven spending pressures commodity suppliers, yet innovators with a specialty focus sustain stronger pricing.

Biologics & Targeted-Therapy Pipeline Expansion

Monoclonal antibodies, biosimilars, and antibody-drug conjugates made up 43% of FDA approvals in 2025, up from 31% in 2020. Samsung Biologics brought a 256,000-liter plant online in May 2025 to meet the rising demand for biologics. Lonza invested CHF 1.2 billion in mammalian-cell capacity across Switzerland and the United States, improving scale for advanced modalities. Peptide APIs for GLP-1 agonists still face tightness despite supplier expansion, reflecting rapid uptake in diabetes and obesity therapy. Extended review timelines, often 18-24 months for multi-region filings, remain a gating factor but are gradually easing under evolving biosimilar comparability rules.

Rising Global GMP & Nitrosamine-Control Compliance Costs

Mandatory nitrosamine testing, fully enforced from 2024, adds USD 150,000-300,000 per dossier and triggered 483 FDA observations at Indian and Chinese sites between 2024 and 2025. EMA aligned thresholds with the FDA in March 2025, removing lower-cost regulatory arbitrage. Smaller firms often lack the funds for high-resolution mass spectrometry upgrades, which accelerates consolidation. Commodity suppliers struggle to pass through new costs, whereas innovators embed compliance expense into project budgets.

Other drivers and restraints analyzed in the detailed report include:

- Outsourced Manufacturing Cost Advantages

- Continuous-Flow & Mini-Plant Technologies Gain Traction

- Generic-Price Compression Squeezing API Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic APIs held 65.78% revenue in 2025, anchored by small-molecule generics for cardiovascular and metabolic therapy, while biologics are slated to post a 9.22% CAGR to 2031, a trend that will raise the biologics share of the active pharmaceutical ingredients market size to nearly one-third. Highly potent APIs increased by 8.1% in 2025 as antibody-drug conjugate payloads advanced, prompting the development of new OEB-5 suites at Lonza and Piramal.

Developers favor biologics for their extended exclusivity and differentiated mechanisms, but large-scale capacity remains concentrated in a handful of players, which keeps average sell prices high. Synthetic producers counter by moving toward continuous-flow and green-chemistry routes that cut solvent waste and shrink batch footprints. Sustainable-sourcing certifications are increasingly influencing purchasing decisions for natural or phytochemical APIs, a small yet image-sensitive niche.

Captive plants commanded 51.73% of 2025 revenue, but merchant producers are set to grow faster, lifting their slice of the active pharmaceutical ingredients market to more than 55% by 2031. WuXi AppTec's 19% annual API sales gain illustrates the pivot, with biotech clients leveraging its regulatory files to avoid capital outlays.

Integrated drug makers maintain select captive lines for intellectual property control, yet fixed costs and underutilization prompt asset sales or hybrid agreements. CDMOs absorb compliance risk and offer faster scale-up, while real-time analytics and AI design tools reduce per-batch engineering, widening the cost gap versus in-house plants.

The Active Pharmaceutical Ingredients Market Report is Segmented by API Type (Synthetic APIs, Biological APIs, and More), Manufacturer Model (Captive/In-house, Merchant/Outsourced), Molecule Size (Small Molecule, Large Molecule/Biologics), Therapeutic Area (Oncology, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 39.64% of the 2025 revenue in the active pharmaceutical ingredients market, driven by Pfizer CentreOne's expansions and the FDA's expedited pathways, which shave 6-9 months off oncology API timelines. The Inflation Reduction Act's credit structure encourages the co-location of API and finished-dosage lines, as evident in AbbVie's USD 1.5 billion biologics upgrade in Massachusetts, completed in March 2025. Canada's regulatory alignment with the FDA speeds Drug Master File approvals, supporting modest domestic growth, while Mexico attracts European CDMOs seeking U.S. proximity through new Monterrey capacity at Recipharm.

Europe will benefit from the forthcoming Critical Medicines Act aimed at 15 essential APIs, though high labor costs temper expansion. Lonza invested CHF 1.2 billion in Swiss and UK sites through 2025, with a focus on mammalian cell and viral vector production. Post-Brexit MHRA rolling-review rules accelerate UK approvals, but dual compliance with EMA standards raises costs for cross-border suppliers. France, Italy, and Spain collectively utilize reshoring grants to revive their antibiotic and sterile-injectable lines, thereby balancing earlier offshoring to Asia.

The Asia-Pacific region is forecast to grow at 10.57% through 2031, the fastest among regions, driven by India's PLI outlays and China's shift from commodity to high-potency oncology intermediates. China's NMPA issued 62 warning letters in 2024-2025, driving facility upgrades but also brief supply disruptions. Japan remains a specialty-API hub, with Fujifilm Diosynth expanding cell-culture capacity, while South Korea's Samsung Biologics plant cements the country's biosimilar prominence.

- Abbvie

- Aurobindo Pharma

- BASF

- Boehringer Ingelheim

- Cambrex

- Catalent

- Cipla

- Dr. Reddy's Laboratories

- GlaxoSmithKline

- Lonza Group

- Merck

- Novartis

- Pfizer CentreOne

- Piramal Group

- Recipharm

- Samsung Group

- Siegfried AG

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- WuXi App Tec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Chronic-Disease Drug Demand

- 4.2.2 Biologics & Targeted-Therapy Pipeline Expansion

- 4.2.3 Outsourced Manufacturing Cost Advantages

- 4.2.4 Continuous-Flow & Mini-Plant Technologies Gain Traction

- 4.2.5 Government PLI/On-Shoring Incentives Reshape Clusters

- 4.2.6 AI-Enabled Retrosynthesis Cuts Development Cycles

- 4.3 Market Restraints

- 4.3.1 Rising Global GMP & Nitrosamine-Control Compliance Costs

- 4.3.2 Generic-Price Compression Squeezing API Margins

- 4.3.3 Supply-Chain Opacity Fueling Quality-Risk Perception

- 4.3.4 Complex Global Regulatory Harmonization for Biotech APIs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By API Type

- 5.1.1 Synthetic APIs

- 5.1.2 Biological APIs

- 5.1.3 Highly-Potent APIs (HPAPIs)

- 5.1.4 Natural / Phytochemical APIs

- 5.2 By Manufacturer Model

- 5.2.1 Captive / In-house

- 5.2.2 Merchant / Outsourced

- 5.3 By Molecule Size

- 5.3.1 Small Molecule

- 5.3.2 Large Molecule / Biologics

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 Cardiovascular

- 5.4.3 Infectious Diseases

- 5.4.4 Metabolic Disorders

- 5.4.5 CNS & Neurology

- 5.4.6 Other Therapeutic Area

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 AbbVie Inc.

- 6.4.2 Aurobindo Pharma

- 6.4.3 BASF SE

- 6.4.4 Boehringer Ingelheim

- 6.4.5 Cambrex Corporation

- 6.4.6 Catalent Inc.

- 6.4.7 Cipla

- 6.4.8 Dr. Reddy's Laboratories

- 6.4.9 GSK plc

- 6.4.10 Lonza Group

- 6.4.11 Merck KGaA

- 6.4.12 Novartis International AG

- 6.4.13 Pfizer CentreOne

- 6.4.14 Piramal Pharma Solutions

- 6.4.15 Recipharm AB

- 6.4.16 Samsung Biologics

- 6.4.17 Siegfried AG

- 6.4.18 Sun Pharmaceutical Industries

- 6.4.19 Teva Pharmaceutical Industries

- 6.4.20 WuXi AppTec

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment