PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035077

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035077

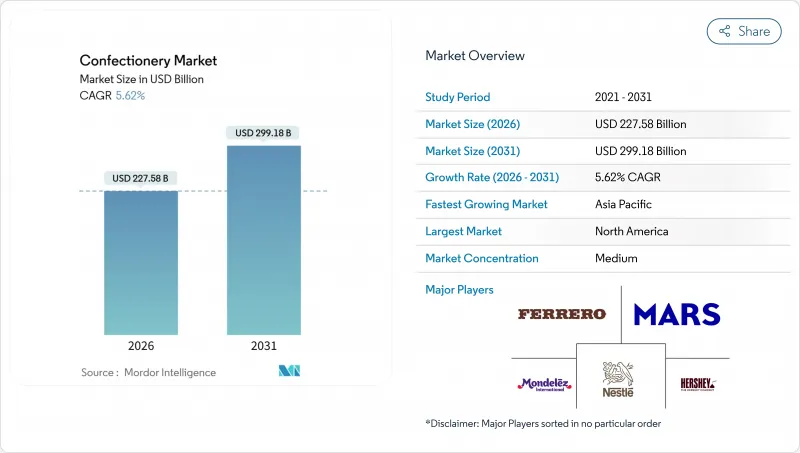

Confectionery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The confectionery market size stood at USD 227.58 billion in 2026 and is projected to reach USD 299.18 billion by 2031, advancing at a 5.62% CAGR.

Several factors are driving this growth, including fluctuations in cocoa prices, a growing focus on health-conscious product reformulations, an increasing demand for premium gifting options, and the implementation of stricter sustainability mandates. These evolving dynamics are compelling manufacturers to mitigate rising costs by introducing value-added products and adopting ethical sourcing practices. Although cocoa futures have recently eased, the long-term supply chain remains vulnerable due to the aging cocoa trees in West Africa and the persistent impact of climate variability. To address these challenges and maintain their market share, brands are innovating by incorporating plant-based dairy alternatives, adding functional ingredients, and utilizing recyclable packaging solutions. These strategies aim to strengthen their position in the highly competitive confectionery market. Additionally, leading industry players are significantly increasing their capital investments, highlighting a strategic effort to absorb raw material price shocks and sustain a robust pace of innovation.

Global Confectionery Market Trends and Insights

Premiumization and experiential gifting boom

L20: Consumers are increasingly allocating their discretionary spending to confectionery products that convey status and provide memorable unboxing experiences, a trend amplified by social media and the growing practice of self-gifting. This shift is particularly evident in the Middle East, where Ramadan and Eid drive demand for luxury chocolate boxes that combine dates with Belgian pralines. Brands like Godiva and Patchi have expanded their retail presence in Dubai and Riyadh to capture high-margin sales during these festive periods. The premiumization trend focuses less on volume growth and more on revenue concentration, as manufacturers recognize that affluent urban consumers in North America, Europe, and the Gulf Cooperation Council are willing to pay a higher price per gram for products offering provenance, craftsmanship, and visually appealing aesthetics. The emotional and experiential value of craft chocolates further drives premiumization, positioning these products as both indulgent treats and gifting options. Brands differentiate themselves through compelling narratives, innovative packaging, and curated flavor profiles. For instance, in June 2025, Cacao Hunters, a premium chocolate brand renowned for its award-winning single-origin chocolates and ethical sourcing, entered the U.S. market, highlighting the growing demand for premium, ethically produced chocolate products.

Demand surges for reduced-sugar, sugar-free, and functional confectionery

Health-conscious consumers, spurred by regulatory mandates, are driving a swift shift in the chocolate, candy, and gum industries towards lower-sugar and sugar-free options. With diseases like diabetes on the rise, consumers are gravitating towards confectionery products with reduced sugar content. According to the latest International Diabetes Federation (IDF) Diabetes Atlas (2025), a notable 11.1% of adults aged 20-79, equating to 1 in 9, are currently living with diabetes . In 2024, the World Health Organization reiterated its stance that free sugars should make up less than 10% of total energy intake, ideally dropping below 5%. This guideline amplifies the urgency for manufacturers to explore and innovate with alternative sweeteners such as allulose, stevia, and erythritol. Beyond just sugar reduction, the realm of functional confectionery is broadening its horizons. In 2024, South Korea witnessed a surge in popularity for taurine-infused candies and probiotic gummies, as consumers increasingly favor snacks that offer wellness benefits alongside their indulgent nature. The gum segment has nearly transitioned entirely to sugar-free variants. Brands like Mars Wrigley are now introducing caffeine-infused and CBD-infused gums, elevating the category's perception from merely a breath freshener to a functional delivery system. When scaled effectively, this pivot proves lucrative; functional ingredients not only command premium price points but also foster repeat purchases from health-conscious consumers, a demographic that traditional candies often find challenging to retain.

Cocoa and sugar cost volatility

Manufacturers are facing significant challenges as fluctuating raw-material prices compress profit margins and necessitate product reformulations, which risk alienating consumers accustomed to established taste profiles. In March 2025, cocoa futures experienced a sharp increase due to export concerns in Ivory Coast, according to the International Cocoa Organization. During their 2024 earnings calls, Mondelez and Hershey emphasized the adverse impact of rising cocoa prices on consumer demand. Both companies indicated that chocolate prices could increase by as much as 50%, with Hershey explicitly stating that it was reformulating its products to reduce cocoa content as a cost-saving measure. Similarly, sugar prices have shown considerable volatility, driven by factors such as unpredictable weather conditions in Brazil and India, biofuel mandates, and currency fluctuations. These dynamics force manufacturers to adopt aggressive hedging strategies or absorb margin compression. However, passing these costs to retailers is not always feasible, as it could result in the loss of valuable shelf space, further complicating the situation for manufacturers.

Other drivers and restraints analyzed in the detailed report include:

- Continuous flavor, texture, and health innovation

- Packaging and convenience support growth

- Sugar-content and child-marketing regulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, chocolate accounted for 54.28% of the market value, reinforcing its position as the premium anchor of the category. However, the Sugar Confectionery segment is expected to grow faster, with a projected 6.10% CAGR through 2031. This growth is fueled by health-conscious consumers seeking functional mints, probiotic gummies, and portion-controlled hard candies. The International Cocoa Organization (ICCO) reported that Africa produced approximately 3.46 million tons of cocoa beans in the 2024/2025 season . This highlights Africa's critical role in the global cocoa supply chain and emphasizes the need for sustainable practices in these key producing regions. By integrating sustainability into their sourcing strategies, chocolate manufacturers can mitigate reputational and supply risks while capitalizing on the expanding segment of ethically conscious consumers, positioning sustainability as a key growth driver. Dark Chocolate is steadily gaining market share within the chocolate segment, as brands focus on its antioxidant benefits and reduced sugar content. Milk and White Chocolate remain the volume leaders but are under pressure to reformulate due to WHO guidelines and national regulations advocating for sugar reduction. The rapid growth of Sugar Confectionery reflects its versatility: Pastilles, Gummies, and Jellies are now infused with vitamins, probiotics, and adaptogens, transforming them from children's treats into functional snacks for adults.

Snack Bars are a high-growth subsegment. Protein Bars and Energy Bars are increasingly used as meal replacements and post-workout recovery options, while Cereal Bars and Fruit and Nut Bars cater to families seeking convenient breakfast solutions. General Mills and Kellogg lead the Cereal Bar market with brands like Nature Valley and Nutri-Grain but face growing competition from startups promoting clean labels and single-ingredient formulations. Gums, including both Chewing Gum and Bubble Gum, experienced declines during the pandemic as mask-wearing reduced consumption, and recovery has been slow. In response, Mars Wrigley and Mondelez are pivoting toward functional gums infused with caffeine, CBD, or teeth-whitening agents to justify premium pricing and reposition the category as a wellness product rather than a commodity breath freshener. This trend reflects a broader shift: product-type boundaries are becoming less distinct. Chocolate bars now compete with protein bars for on-the-go nutrition, and gummies rival vitamin supplements for functional benefits. This shift is pushing manufacturers to redefine their categories and invest in cross-category innovation.

L28: In 2025, single-serve formats accounted for 58.97% of the market value, driven by convenience stores, vending machines, and impulse purchases at checkout counters. However, multipacks are expected to grow faster, with a projected 6.38% CAGR through 2031. This growth is primarily fueled by e-commerce platforms and warehouse clubs, which attract consumers by offering lower per-unit costs for bulk purchases. To address the needs of online shoppers, who cannot physically inspect products, confectionery brands are redesigning multipacks with features such as resealable closures, transparent windows, and portion-control options. Mondelez introduced paper-based Toblerone packaging in select European markets in 2024, aligning with its goal to make 95% of its packaging recyclable or reusable by 2025. The shift toward sustainable materials is gaining momentum, particularly as Europe's Extended Producer Responsibility schemes impose financial penalties on non-recyclable packaging. Innovations in single-serve packaging emphasize portability and shelf appeal. Mars tested compostable M&M's pouches that decompose within 12 weeks in industrial composting facilities, while Nestle launched paper-based KitKat wrappers in several countries, aiming to eliminate plastic entirely.

Multipacks are transitioning from simple bundling to variety packs that combine multiple flavors or formats. This approach not only encourages product trials but also reduces decision fatigue for consumers shopping online or at warehouse clubs. Ferrero's Kinder variety packs, which include Kinder Bueno, Kinder Chocolate, and Kinder Joy in one box, illustrate this strategy. The distribution of packaging types highlights channel dynamics: convenience stores and gas stations prefer single-serve formats for impulse purchases, while supermarkets and hypermarkets allocate shelf space to both formats. Online retailers prioritize multipacks to distribute shipping costs across higher order values. Manufacturers face the challenge of managing SKU proliferation, since each packaging format requires separate production runs and inventory management, while meeting the demands of diverse channels and occasions. This challenge often benefits larger players with flexible manufacturing capabilities and advanced demand-planning systems.

The Confectionery Market Report is Segmented by Product Type (Chocolate, Sugar Confectionery, Snack Bar, Gums), Packaging Type (Single-Serve, Multipacks), Price Tier (Mass, Premium), Distribution Channel (Supermarket/Hypermarket, Online Retail Store, Convenience Store, Other), and Geography (North America, South America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Geography Analysis

North America represented 36.57% of the global confectionery market in 2025, supported by the U.S.'s strong per-capita consumption and established retail infrastructure. However, the region's growth is slowing as health trends and regulatory pressures drive consumers toward reduced-sugar and functional alternatives. While Canada and Mexico hold smaller shares, they exhibit unique characteristics: Canada's market increasingly reflects U.S. trends, with a focus on premiumization and plant-based options. As the region matures, growth will primarily come from premiumization, functional innovations, and shifts in sales channels rather than volume increases. Brands that fail to address the health-conscious shift risk losing market share to agile startups and private labels.

Asia-Pacific is projected to achieve a strong 6.54% CAGR through 2031, fueled by rising incomes in India, Indonesia, and Vietnam amid expanding GDP in developing Asia. Multinational brands are attracting first-time buyers with localized flavors such as cardamom chocolate and mango gummies. South Korea and Japan emphasize functional and premium offerings, while China's slower consumption growth tempers the regional average. In 2024, Barry Callebaut launched an innovation hub in Singapore to deliver customized coatings and capitalize on the region's growing momentum. In many Southeast Asian cities, digital commerce has surpassed traditional retail, making mobile-first strategies critical for capturing confectionery market growth.

Europe maintains stable volumes but faces stricter nutrient requirements and sustainability regulations. In 2024, Mondelez introduced Cadbury Dairy Milk 30% Less Sugar in the U.K. to anticipate tighter sugar guidelines. Seasonal demand, such as Easter eggs and Christmas pralines, drives markets in Germany, France, and Italy. Meanwhile, Switzerland and Belgium leverage their heritage to secure premium pricing. Nestle, under cost pressures, invested over CHF 100 million to modernize its Swiss factories and sustain regional production. Eastern European facilities, benefiting from lower labor costs, meet Western demand, enhancing their competitiveness within the broader confectionery market.

- Mars Inc.

- Mondelez International Inc.

- Nestle S.A.

- Ferrero Group

- The Hershey Company

- Barry Callebaut AG

- Kellogg Company

- General Mills Inc.

- Yildiz Holding

- HARIBO Holding

- Perfetti Van Melle BV

- Lotte Corporation

- Meiji Holdings

- Ezaki Glico Co Ltd

- Grupo Arcor

- August Storck KG

- Lindt and Sprungli AG

- Godiva Chocolatier

- Cargill Cocoa and Chocolate

- Barry Callebaut (Processing)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization and experiential gifting boom

- 4.2.2 Demand surges for reduced-sugar, sugar-free, and functional confectionery

- 4.2.3 Continuous flavour, texture, and health innovation

- 4.2.4 Packaging and convenience support the growth

- 4.2.5 Ethical sourcing of ingredients, eco-friendly packaging

- 4.2.6 Advent-calendar-style seasonal bundling

- 4.3 Market Restraints

- 4.3.1 Cocoa and sugar cost volatility

- 4.3.2 Sugar-content and child-marketing regulation

- 4.3.3 Carbon-credit land competition squeezing cocoa supply

- 4.3.4 Price-elastic volume drops after sharp hikes

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Chocolate

- 5.1.1.1 Dark Chocolate

- 5.1.1.2 Milk and White Chocolate

- 5.1.2 Sugar Confectionery

- 5.1.2.1 Hard Candy

- 5.1.2.2 Mints

- 5.1.2.3 Pastilles, Gummies, and Jellies

- 5.1.2.4 Toffees and Nougats

- 5.1.2.5 Lollipops

- 5.1.2.6 Other

- 5.1.3 Snack Bar

- 5.1.3.1 Cereal Bar

- 5.1.3.2 Energy Bar

- 5.1.3.3 Protein Bar

- 5.1.3.4 Fruit and Nut Bar

- 5.1.4 Gums

- 5.1.4.1 Chewing Gum

- 5.1.4.1.1 Sugar Chewing Gum

- 5.1.4.1.2 Sugar-free Chewing Gum

- 5.1.4.2 Bubble Gum

- 5.1.4.1 Chewing Gum

- 5.1.1 Chocolate

- 5.2 Packaging type

- 5.2.1 Single-serve

- 5.2.2 Multipacks

- 5.3 Price Tier

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 Distribution Channel

- 5.4.1 Supermarket/Hypermarket

- 5.4.2 Online Retail Store

- 5.4.3 Convenience Store

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Chile

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Sweden

- 5.5.3.8 Belgium

- 5.5.3.9 Poland

- 5.5.3.10 Netherlands

- 5.5.3.11 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Thailand

- 5.5.4.5 Singapore

- 5.5.4.6 Indonesia

- 5.5.4.7 South Korea

- 5.5.4.8 Australia

- 5.5.4.9 New Zealand

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mars Inc.

- 6.4.2 Mondelez International Inc.

- 6.4.3 Nestle S.A.

- 6.4.4 Ferrero Group

- 6.4.5 The Hershey Company

- 6.4.6 Barry Callebaut AG

- 6.4.7 Kellogg Company

- 6.4.8 General Mills Inc.

- 6.4.9 Yildiz Holding

- 6.4.10 HARIBO Holding

- 6.4.11 Perfetti Van Melle BV

- 6.4.12 Lotte Corporation

- 6.4.13 Meiji Holdings

- 6.4.14 Ezaki Glico Co Ltd

- 6.4.15 Grupo Arcor

- 6.4.16 August Storck KG

- 6.4.17 Lindt and Sprungli AG

- 6.4.18 Godiva Chocolatier

- 6.4.19 Cargill Cocoa and Chocolate

- 6.4.20 Barry Callebaut (Processing)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK