PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035079

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035079

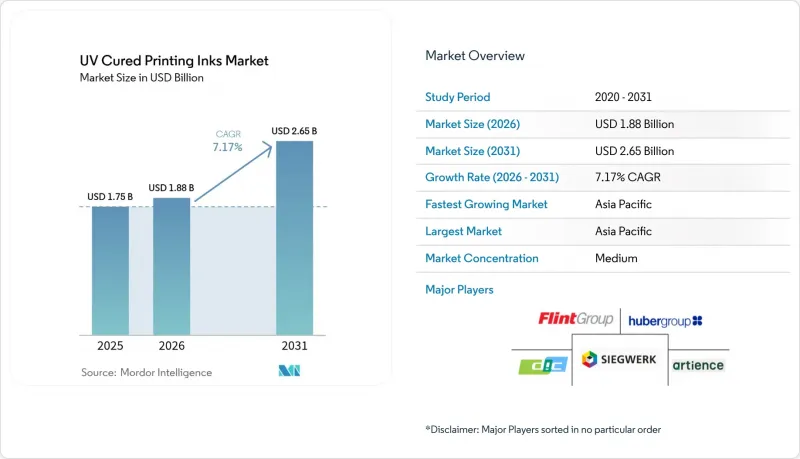

UV Cured Printing Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The UV Cured Printing Inks Market size was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.88 billion in 2026 to reach USD 2.65 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031).

Energy-efficient LED curing, which lowers press power consumption by 60-65% while removing mercury lamp maintenance and VOC emissions, is the primary growth driver. Packaging converters are accelerating adoption because low-migration formulations meet tightening food-contact rules in Asia-Pacific, the European Union, and North America. As OEMs release retrofit LED systems that raise press speeds 30-50% without new capital outlay, the addressable installed base widens and barriers to entry fall. At the same time, photoinitiator supply risks and emerging water-based or EB-curable alternatives inject competitive pressure that suppliers must manage through innovation and sourcing agility.

Global UV Cured Printing Inks Market Trends and Insights

Growing Demand from Digital and Inkjet Printing

Print-on-demand adoption lets publishers slash warehousing expenses and meet rapid turnaround expectations, and UV-cured inks enable crisp imagery on coated and uncoated substrates without post-press drying delays. Direct mail volumes are rebounding as brands integrate tactile pieces with digital campaigns, reinforcing demand for durable, scuff-resistant UV impressions that withstand postal handling. Research and development momentum is visible in FUJIFILM's patent covering surfactant-modified inkjet formulations that reduce inter-color bleeding and heighten gloss uniformity, an advance that strengthens UV compatibility with high-speed piezo heads. Commercial shops that add web-to-print storefronts tap short-run personalized jobs where instant curing shortens job queues. Although legacy publication volumes keep shrinking, the value shift to variable-data and specialty substrates produces a net positive pull on UV-cured printing inks market growth.

Expansion of Packaging and Label Converters

Converter capacity is rising across Indonesia, India, and Vietnam as regional FMCG demand climbs and global brands nearshore supply chains; each new press line typically specifies LED UV or hybrid curing to cut make-ready waste and satisfy factory ESG benchmarks. Flexographic press upgrades, exemplified by Miraclon's FLEXCEL NX platform, let converters match gravure aesthetics while using thinner plates and lower ink laydowns that suit UV formulations. Brand-owner sustainability scorecards increasingly credit energy savings from UV LED curing, nudging converters toward technology refresh. The dual need to meet food-contact rules and lower total cost of ownership cements packaging's pull on the UV-cured printing inks market.

Decline of Conventional Commercial Printing

Newspaper and magazine pagination keeps sliding as advertisers channel budgets into digital platforms, eroding legacy UV offset ink demand. Commercial printers that fail to pivot toward packaging, labels, or value-added embellishments face press under-utilization that directly reduces ink consumption. While high-margin short runs temper revenue loss, volume attrition persists, marking this restraint as a structural headwind.

Other drivers and restraints analyzed in the detailed report include:

- Stricter VOC/Sustainability Regulations

- Rapid Shift to Energy-Efficient LED UV Systems

- Competition from Water-Based and EB-Curable Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LED systems accounted for 56.14% of the UV-cured printing inks market size in 2025 and are forecast to post a 9.13% CAGR to 2031, underlining the technology's broad acceptance among converters focused on energy metrics. The retrofit option lowers capital hurdles, letting operators preserve existing press platforms while sharply reducing downtime. Lower stack temperatures eliminate sheet distortion on thin films and enable higher nip pressures that maintain registration accuracy at press speeds above 18,000 sph. These attributes collectively sustain LED's leadership in the UV-cured printing inks market.

Arc-lamp curing retains a toehold in certain wide-web and screen-printing applications that need broadband spectra to trigger cationic photochemistry. However, recent high-output LED diodes reaching 25 W/cm2 narrow the former gap in cure depth, and hybrid lamp housings let users toggle modes mid-shift, hastening the migration curve. As government restrictions on mercury escalate, arc-lamp economics will further erode, reinforcing LED's dominant trajectory.

The UV-Cured Printing Inks Report is Segmented by Curing Process (Arc Curing and LED Curing), Ink Type (UV Flexo Inks, UV Offset Inks, UV Low Energy/LED Offset Inks, and More), Application (Packaging, Commercial and Publication, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 48.05% of 2025 revenue and is tracking a 9.08% CAGR to 2031, led by China's nationwide GB 4806.14-2023 compliance deadline and India's IS:15495 enforcement that restricts toluene in food packaging inks. Local leaders such as UFlex have introduced polyester acrylates that bond to metallized films, enabling converters to meet both barrier and migration goals in a single pass. Government incentives that refund up to 30% of energy-saving equipment costs further accelerate LED UV adoption across new gravure and flexo halls, cementing the region's pull on the UV-cured printing inks market.

North America holds a technology-rich base where early adopters embraced LED units as early as 2016. The U.S. EPA's endorsement and the Inflation Reduction Act's clean-manufacturing credits financed numerous retrofits during 2024-25. Resin and additive capacity expansions, exemplified by Lubrizol's doubling of Solsperse hyperdispersant output in Ohio, bolster supply assurance for domestic ink makers.

The Middle East and Africa, and South America contribute modest volume shares today, yet represent latent upside as packaging converters migrate from solvent lines to LED platforms to comply with export customer audits. Brazilian label printers installing hybrid UV-EB flexo lines attest to an emerging technology leapfrog that could compress adoption timelines once macroeconomic conditions stabilize.

- ALTANA

- APV Engineered Coatings

- artience Co. Ltd. (TOYO INK CO., LTD.)

- Avery Dennison Corporation

- DIC Corporation

- Flint Group

- FUJIFILM Corporation

- Huber Group

- Marabu GmbH & Co. KG

- MIMAKI ENGINEERING CO., LTD.

- Nazdar

- SAKATA INX CORPORATION

- Siegwerk Druckfarben AG & Co. KGaA

- T&K TOKA Corporation

- TOKYO PRINTING INK MFG. CO., LTD.

- Van Son Ink Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from Digital and Inkjet Printing

- 4.2.2 Expansion of Packaging and Label Converters

- 4.2.3 Stricter VOC/Sustainability Regulations

- 4.2.4 Rapid Shift to Energy-Efficient LED UV Systems

- 4.2.5 Adoption of Low-Migration Inks in Food and Pharma Packs

- 4.3 Market Restraints

- 4.3.1 Decline of Conventional Commercial Printing

- 4.3.2 Competition from Water-Based and EB-Curable Systems

- 4.3.3 Photoinitiator Supply-Chain Volatility (China Clampdowns)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Curing Process

- 5.1.1 Arc Curing

- 5.1.2 LED Curing

- 5.2 By Ink Type

- 5.2.1 UV Flexo Inks

- 5.2.2 UV Offset Inks

- 5.2.3 UV Low Energy/LED Offset Inks (Except UV Offset Inks)

- 5.2.4 UV Screen Printing Inks

- 5.2.5 Other UV Cured Printing Inks Type

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Commercial and Publication

- 5.3.3 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JV, Partnerships)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ALTANA

- 6.4.2 APV Engineered Coatings

- 6.4.3 artience Co. Ltd. (TOYO INK CO., LTD.)

- 6.4.4 Avery Dennison Corporation

- 6.4.5 DIC Corporation

- 6.4.6 Flint Group

- 6.4.7 FUJIFILM Corporation

- 6.4.8 Huber Group

- 6.4.9 Marabu GmbH & Co. KG

- 6.4.10 MIMAKI ENGINEERING CO., LTD.

- 6.4.11 Nazdar

- 6.4.12 SAKATA INX CORPORATION

- 6.4.13 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.14 T&K TOKA Corporation

- 6.4.15 TOKYO PRINTING INK MFG. CO., LTD.

- 6.4.16 Van Son Ink Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment