PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035087

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035087

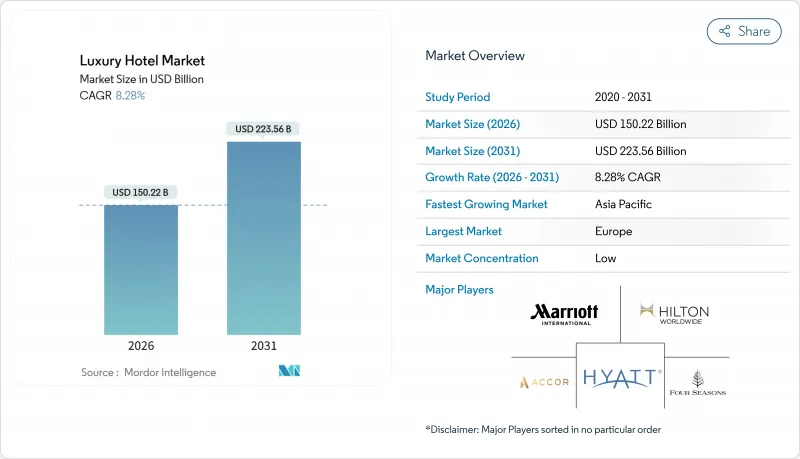

Luxury Hotel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The luxury hotel market size is USD 150.22 billion in 2026 and is projected to reach USD 223.56 billion by 2031, reflecting an 8.28% CAGR over the forecast period.

Momentum builds as high-end travel continues to scale on the back of steady international arrivals, renewed corporate budgets, and wider adoption of experiential and wellness-led itineraries that sustain rate power in both urban and resort settings. Operators enhance digital touchpoints around discovery, booking, and in-stay personalization, while aligning with procurement preferences that favor verifiable sustainability credentials and third-party certifications. The recovery in international travel is broad-based, with Europe welcoming 625 million tourists through September 2025 and Asia-Pacific reaching 90% of its 2019 baseline, which sustains occupancy and mix in key destinations and supports the rate-led strength now visible in upscale and luxury categories. Certification programs such as LEED and Green Key continue to expand across upscale portfolios, giving certified properties procurement advantages, efficiency benefits, and reputational gains that reinforce competitive positioning in the luxury hotel market.

Global Luxury Hotel Market Trends and Insights

Rebound Of International Tourism Post-Pandemic

International travel has reset at higher levels, with global tourist arrivals up 5% year over year through September 2025 and above 2019 by 3%, which provides a strong demand base for the luxury hotel market as premium travelers return to cross-border itineraries. Europe captured 625 million tourists over the same period, while Asia-Pacific recovered to 90% of 2019 levels, signaling that both traditional gateways and fast-rising leisure hubs can support length-of-stay and rate integrity as connectivity improves and visa regimes stabilize. Luxury portfolios gain additional lift from the reorientation toward more purposeful travel, including wellness, culinary immersion, and culture-led programming that deepens spend per stay and sustains a premium mix in the luxury hotel market. Procurement preferences also evolve alongside travel normalization, with many buyers screening for credible sustainability credentials where third-party certification qualifies properties for corporate programs and travel-policy compliance. This alignment between traveler intent and supplier capability narrows the performance gap between mature city centers and secondary destinations as more operators bring certified, experience-rich offerings to market, reinforcing a positive outlook for the luxury hotel market. As capacity returns and airlift broadens, the channel mix continues to diversify, with operators using data-driven personalization to defend direct relationships while leveraging the discovery reach of intermediaries, adding resilience to the demand base that supports the sector's forecast CAGR.

Rising Disposable Incomes in Emerging Asian Economies

Broadening middle and upper-middle cohorts across Asia reinforces the growth runway for the luxury hotel market as intra-regional trips scale and premium segments migrate from goods toward experience-led spending, raising the ceiling for resort and lifestyle assets in tier-1 and select tier-2 cities. Operators are positioning ahead of this curve, with signings across Asia-Pacific accelerating in 2024 and 2025 as brands seek first-mover advantage in under-supplied leisure corridors and fast-growing urban nodes. Pipeline breadth in Greater China and Southeast Asia suggests that a broader base of affluent households will support premium ADRs in coastal resorts, nature-led destinations, and urban lifestyle districts as connectivity and retail ecosystems expand around these investments. At the same time, Europe and North America continue to attract Asian outbound travelers, which further balances geographic demand in the luxury hotel market as flight capacity stabilizes and traveler confidence improves. The demand mix also benefits from younger affluent cohorts who prioritize wellness, design, and culinary experiences, elevating brands that can tailor offerings with flexible inventory and integrative programming. This interplay of rising affluence and brand expansion into new nodes supports both occupancy stability and rate growth in the forecast period for the luxury hotel market.

High Capex & Long ROI Cycles

Luxury projects require significant capital and multi-year delivery timelines, which stretch payback periods and expose owners to interest-rate and construction-cost risk as projects move from design to opening in the luxury hotel market. Renovations and repositionings can depress near-term profitability even for high-performing assets, although the long-run value proposition remains intact once new products and amenities reset price ceilings. Owners balance new-build risk with conversion strategies, leaning into brand upgrades that lower time-to-market while retaining the benefits of scale, loyalty, and distribution that come with major flags in the luxury hotel market. Even so, conversions require targeted property-improvement plans and capital outlays to align with brand standards and to compete effectively for premium guests, especially in gateway cities where benchmarks are exacting. Business disruption from extreme weather and demand shocks can complicate forecasting and underwriting for luxury portfolios, as seen in reporting from leading United States REITs that detail renovation impacts and insurance dynamics in quarterly results. Workforce constraints can further elevate operating costs and slow ramp schedules, with staffing shortages still widely reported by United States properties, which adds friction to opening timelines and service deployment in the luxury hotel market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Branded Luxury Chains into Tier-2 Cities

- Growth Of Ultra-High-Net-Worth Individuals from Tech IPOs

- Geopolitical Instability on Key Luxury Corridors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Business Hotels retained the largest position with 46.36% in 2025, while resorts are the fastest-expanding service type with a projected 13.47% CAGR through 2031, underscoring the shift toward experience-led leisure in the luxury hotel market. This gap reflects diverging demand patterns, where integrated wellness, nature-forward design, and high-amenity beachfront and mountain resorts sustain premiums that are accretive to portfolio ADRs. Urban luxury continues to benefit from the return of corporate travel, with high-end groups optimizing mix by combining group, corporate, and premium leisure, yet the resort thesis grows faster as travelers prioritize rejuvenation and immersion in the luxury hotel market. Leading groups are also activating multi-format strategies that weave in branded residences and curated journeys, which expand the spend universe around flagship resorts. Large-scale projects in emerging leisure destinations, including regenerative resort clusters, further anchor the medium-term growth narrative for resort-led offerings in the luxury hotel market.

The performance spread across service types depends on place, positioning, and programming, with certified resorts showing procurement advantages and operating efficiencies that strengthen cash flow over time in the luxury hotel market. Operators that align guest journeys with local culture, design integrity, and sustainability measures can support both occupancy and rate across peak and shoulder months. Urban luxury retains pricing influence in global gateways where airlift, events calendars, and corporate activity stabilize demand, yet resort inventory remains the momentum leader as new supply opens in secondary leisure corridors. This mix of stable city demand and accelerating resort growth contributes to the broader durability observed in the luxury hotel market. As portfolios scale across formats, loyalty ecosystems help cross-sell urban and resort stays, raising retention and lifetime value as the cycle advances in the luxury hotel industry.

The Luxury Hotel Market Report is Segmented by Service Type (Business Hotels, Airport Hotels, Suite Hotels, Resorts, and Other Service Types), Room Type (Standard Luxury Room, Suites, Villas and Others ), Booking Channel (Direct Booking, Online Travel Agencies, and Others), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained 37.38% of the luxury hotel market share in 2025, with international arrivals through September reaching 625 million, which reinforces the region's mix of gateway city strength and destination leisure momentum. Major groups maintain robust development plans across Europe's capitals and cultural hubs, supported by investment in premium renovations, brand refreshes, and targeted conversions that keep product fresh. Sustainability credentials see consistent adoption, with many properties engaging third-party certification programs to align with procurement requirements and consumer expectations. Luxury portfolios continue to balance leisure destinations in Southern Europe with business-oriented stock in Northern Europe, while extending into secondary cities on the back of improved air and rail connectivity. As festival, sports, and culture calendars fill out, Europe remains a core anchor for the luxury hotel market through the forecast period.

Asia-Pacific is projected to be the fastest-growing region with an 11.43% CAGR to 2031, supported by intra-regional travel growth and an expanding base of affluent consumers who favor experience-led stays in premium resorts and urban lifestyle hotels. The region reached 90% of 2019 arrival levels by September 2025, reflecting the late-but-strong rebound that is now translating into sustained room-night demand for the luxury hotel market. Development pipelines highlight strategic emphasis on coastal leisure corridors, nature-led retreats, and tier-2 cities where infrastructure upgrades compress travel friction. International brands are broadening their footprints and formats, with signings in Greater China, Japan, and Southeast Asia pointing to multi-year supply growth, mixed-use plays, and branded residence integration. As certification programs and national sustainability roadmaps gain traction, premium assets with verifiable progress are set to capture procurement-led demand advantages across the region.

North America remains a stable pillar of demand, supported by resilient high-income household spending, a deep group calendar, and a balanced mix across urban and resort destinations in the luxury hotel market. Portfolio activity includes renovations, selective conversions, and expansion of longer-stay and apartment-style offerings that target hybrid work patterns and family travel. Transaction and development strategies remain disciplined, with owners calibrating capital programs and phasing to align with demand pacing in urban cores and leisure destinations. In the Middle East and Africa, arrivals by late 2025 exceeded pre-pandemic baselines in several hubs, with large-scale coastal and desert projects creating new destination clusters that elevate the region's profile in the luxury hotel market. New luxury openings and branded residences play in flagship developments reinforce the region's long-run demand thesis and deepen global brand exposure across high-spend segments.

- Marriott International (The Ritz-Carlton, St. Regis)

- Hilton Worldwide (Waldorf Astoria, Conrad)

- Accor (Fairmont, Raffles)

- Hyatt Hotels Corporation (Park Hyatt, Andaz)

- Four Seasons Hotels & Resorts

- InterContinental Hotels Group (Regent, InterContinental)

- Mandarin Oriental Hotel Group

- Kempinski Hotels

- Shangri-La Hotels and Resorts

- Rosewood Hotel Group

- Belmond Ltd.

- The Leading Hotels of the World

- Aman Resorts

- Six Senses Hotels Resorts Spas

- Banyan Tree Holdings

- Auberge Resorts Collection

- Dorchester Collection

- Oetker Collection

- Minor Hotels (Anantara)

- Jumeirah Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rebound of international tourism post-pandemic

- 4.2.2 Rising disposable incomes in emerging Asian economies

- 4.2.3 Expansion of branded luxury chains into tier-2 cities

- 4.2.4 Hybrid work trends boosting long-stay bleisure demand

- 4.2.5 Growth of ultra-high-net-worth individuals from tech IPOs

- 4.2.6 Carbon-neutral certification premiums influencing bookings

- 4.3 Market Restraints

- 4.3.1 High capex & long ROI cycles

- 4.3.2 Geopolitical instability on key luxury corridors

- 4.3.3 Regulatory scrutiny on foreign ownership of landmark assets

- 4.3.4 Talent scarcity for bespoke service roles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Business Hotels

- 5.1.2 Airport Hotels

- 5.1.3 Suite Hotels

- 5.1.4 Resorts

- 5.1.5 Other Service Types

- 5.2 By Room Type

- 5.2.1 Standard Luxury Room

- 5.2.2 Suites

- 5.2.3 Villas / Bungalows

- 5.2.4 Penthouses & Presidential Suites

- 5.3 By Booking Channel

- 5.3.1 Direct Booking (Brand Website, Call Center)

- 5.3.2 Online Travel Agencies (OTA)

- 5.3.3 Travel Agents / Tour Operators

- 5.3.4 Corporate Contracts

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Marriott International (The Ritz-Carlton, St. Regis)

- 6.4.2 Hilton Worldwide (Waldorf Astoria, Conrad)

- 6.4.3 Accor (Fairmont, Raffles)

- 6.4.4 Hyatt Hotels Corporation (Park Hyatt, Andaz)

- 6.4.5 Four Seasons Hotels & Resorts

- 6.4.6 InterContinental Hotels Group (Regent, InterContinental)

- 6.4.7 Mandarin Oriental Hotel Group

- 6.4.8 Kempinski Hotels

- 6.4.9 Shangri-La Hotels and Resorts

- 6.4.10 Rosewood Hotel Group

- 6.4.11 Belmond Ltd.

- 6.4.12 The Leading Hotels of the World

- 6.4.13 Aman Resorts

- 6.4.14 Six Senses Hotels Resorts Spas

- 6.4.15 Banyan Tree Holdings

- 6.4.16 Auberge Resorts Collection

- 6.4.17 Dorchester Collection

- 6.4.18 Oetker Collection

- 6.4.19 Minor Hotels (Anantara)

- 6.4.20 Jumeirah Group

7 Market Opportunities & Future Outlook

- 7.1 Ultra-luxury eco-conscious retreats in secondary destinations

- 7.2 AI-driven hyper-personalization across the guest journey