PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035093

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035093

Edge Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

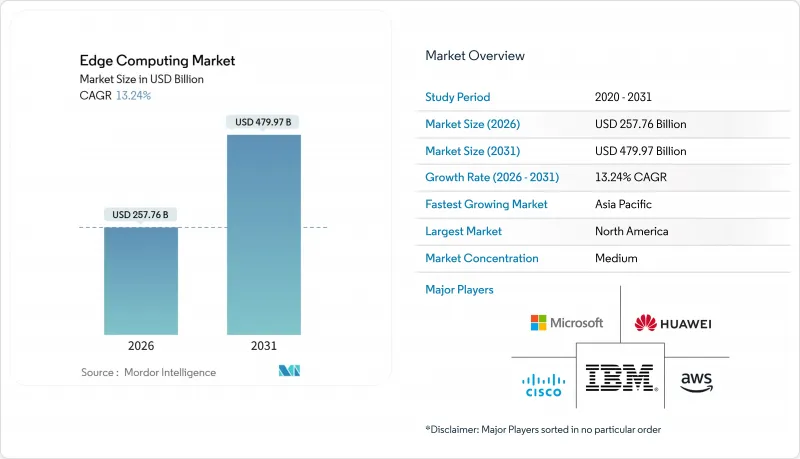

The edge computing market size reached USD 257.76 billion in 2026 and is projected to advance to USD 479.97 billion by 2031 at a 13.24% CAGR, underscoring a decisive pivot toward distributed processing architectures that minimize round-trip latency and comply with emerging data-sovereignty rules.

5G standalone roll-outs, jurisdictional data-localization mandates, and an explosion of AI-enabled endpoints concentrate demand at the network perimeter, while declining ASIC and system-on-chip prices lower the entry barrier for on-premise inference. Hyperscalers extend public-cloud control planes into carrier facilities and enterprise campuses, blending cloud convenience with local processing. Industrial IoT installs, real-time clinical diagnostics, and autonomous systems fuel near-term spending, whereas carbon-reduction targets and chiplet-based custom silicon shape longer-run innovation. Competitive advantage gravitates to providers that orchestrate heterogeneous nodes through a single Kubernetes-native plane and embed zero-trust security from silicon to workload.

Global Edge Computing Market Trends and Insights

5G Roll-Out Catalysing Ultra-Low-Latency Use-Cases

Standalone 5G cores now steer traffic to base-station micro data centers, trimming round-trip latency below 10 milliseconds. Asian operators had installed 1.8 million edge-enabled 5G sites by mid-2025, enabling factory automation and remote-surgery pilots. Europe shows slower uptake because many carriers still depend on 4G cores, limiting multi-access edge compute despite high radio coverage. Spectrum licenses in the 3.5 GHz band now include edge-hosting clauses, pushing telcos to colocate compute with radios. Equipment vendors bundle orchestration software with radios, letting enterprises deploy container workloads through familiar cloud APIs. These conditions make 5G the primary on-ramp for ultra-reliable low-latency edge applications across mobility, gaming, and industrial control.

Proliferation of IoT Endpoints and Data Gravity at the Edge

Enterprise IoT connections exceeded 19 billion in 2025, producing exabyte-scale telemetry that swamps backhaul links and raises egress fees. A single automotive plant now streams terabytes daily, yet only a fraction of that data merits long-term storage, pushing analytics to on-site gateways. Edge processing lowers cloud bills and tightens control loops, boosting equipment uptime by double-digit percentages. IEC 62443 security guidelines further mandate local anomaly detection to shield operational technology from network faults. As AI models compress onto watt-scale chips, companies ship insights rather than raw data, reinforcing the gravity of the pull toward edge locations. This dynamic reallocates budget from central servers to ruggedized nodes and fleet-management software.

Cyber-Attack Surface Expansion at Distributed Nodes

Each edge gateway adds another ingress point, and Mirai variants already exploit weak credentials on industrial controllers for DDoS campaigns. NIST's Cybersecurity Framework 2.0 now includes edge-specific controls, yet many SMEs lack the staff to implement secure boot, certificate rotation, and microsegmentation. Firmware refresh cycles stretch five to seven years, leaving devices exposed long after new vulnerabilities appear. Supply-chain directives require signed firmware, but enforcement outside critical infrastructure sectors remains patchy. Insurance premiums for edge deployments climbed 12% in 2025 as carriers priced in the likelihood of breaches. Without automated remediation and stronger baseline hardening, security fears could deter late adopters.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Data-Sovereignty Mandates (EU Data Act)

- Declining ASIC/SoC Costs for Edge Inference Accelerators

- Skills Gap in Deploying and Managing Heterogeneous Edge Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is on track to eclipse appliance sales as customers shift capital outlays into operational budgets. In 2025, hardware still accounted for 47.13% of the edge computing market, yet managed services are forecast to grow at 13.87% annually through 2031, supported by hyperscaler bundles that fuse compute, orchestration, and security under subscription pricing. Dell noted a 19% jump in edge-infrastructure revenue, but its services attach rate hit 68% as clients demanded lifecycle management. Hewlett Packard Enterprise's GreenLake contracts, billed per workload, eliminate capacity-planning risk and improve time-to-value for factories retrofitting AI inspection. Hardware commoditization persists as DRAM and NAND costs fluctuate; ODM rivalry tempers server ASPs, prompting vendors to focus on software differentiation and professional services.

Edge-native software, including slim Kubernetes distributions and eventually consistent databases, grows at 13.45% through 2031. Red Hat OpenShift and SUSE Rancher square off for enterprise control-plane dominance, while open-source K3s captures resource-constrained deployments. System integrators such as Capgemini Engineering saw OT-edge engagements rise 34% in 2024, reflecting demand for domain expertise to translate shop-floor processes into microservice architectures. Overall, services convert one-time margin into multiyear cash flows, positioning vendors to capture long-run value once hardware marginal gains plateau.

Cloud-connected installations commanded 58.19% of the edge computing market share in 2025 and will expand at a 13.61% CAGR through 2031 as AWS Wavelength, Azure Edge Zones, and Google Distributed Cloud push hyperscaler APIs into carrier facilities. These offerings deliver sub-10-millisecond latency without demanding proprietary edge SDKs, lowering developer friction. Microsoft expanded Azure Edge Zones to 47 metro areas and publicly promotes single-control-plane management from the cloud to the factory floor.

On-premise deployments persist in regulated verticals that bar external data transit - pharma batch records, PCI-DSS card data, and safety-critical automation. Even there, organizations increasingly adopt cloud-native orchestration to avoid divergent toolchains. Hybrid topologies blend gateway hardware installed behind corporate firewalls with cloud-managed configuration, striking a balance between data residency and operational agility. EU Data Act portability clauses accelerate this pattern because enterprises must demonstrate switching readiness, favoring open Kubernetes over proprietary edge stacks.

The Edge Computing Market Report is Segmented by Component (Hardware, Software, Services), Deployment Mode (On-Premise, and Cloud), End-User Industry (Energy and Utilities, and More), Application (Video Analytics and Surveillance, Autonomous Vehicles and Drones, and More), Organisation Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 33.91% of 2025 spending, anchored by hyperscaler footprints and early standalone 5G launches from Verizon and AT&T. The United States alone hosts 108 AWS Wavelength zones and 23 Azure Edge Zones, giving developers nationwide low-latency endpoints. Canada's Bell and Telus added multi-access edge compute to support industrial IoT across resource-extraction sites, while Mexican factories deploy edge quality inspection under nearshoring incentives introduced by the T-MEC accord.

Asia-Pacific is forecast to expand at a 14.21% CAGR through 2031, driven by China Mobile's 1.8 million edge-enabled 5G base stations. India's Digital India initiative earmarked 100 smart cities for edge-powered municipal services, while Southeast Asia's manufacturing migration is accelerating local edge adoption. Japan's NTT Docomo and South Korea's SK Telecom integrate edge into autonomous vehicle pilots, while Australia exploits edge compute in remote mining where satellite backhaul is constrained.

Europe held roughly 24% of global spend in 2025, buoyed by the EU Data Act's sovereignty requirements and 1,836 documented nodes. Germany, France, and the Netherlands host 61% of these installations, covering automotive, finance, and healthcare. Smart-city mega-projects in Saudi Arabia's NEOM and the UAE's Dubai Smart City spearhead Middle East demand, whereas South America clusters center on Brazilian industrial automation and Argentine telecom modernization. Regional spending profiles mirror policy commitments: the U.S. CHIPS and Science Act injects USD 52 billion into domestic semiconductors, and the EU Digital Decade targets 10,000 nodes by 2030, ensuring sustained capex pipelines.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Dell Technologies Inc.

- Google LLC (Alphabet Inc.)

- Intel Corporation

- NVIDIA Corporation

- Juniper Networks Inc.

- Advantech Co. Ltd.

- ADLINK Technology Inc.

- Schneider Electric SE

- Siemens AG

- Capgemini Engineering

- MachineShop Inc.

- Vapor IO Inc.

- Litmus Automation

- FogHorn Systems

- Lumen Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G Roll-Out Catalysing Ultra-Low-Latency Use-Cases

- 4.2.2 Proliferation of IoT Endpoints and Data Gravity at the Edge

- 4.2.3 Regulatory Data-Sovereignty Mandates (e.g., EU Data Act)

- 4.2.4 Declining ASIC/SoC Costs for Edge Inference Accelerators

- 4.2.5 Energy-Efficiency Targets Driving Micro-Data-Centres (ESG)

- 4.2.6 Rise of RISC-V and Chiplet Architectures Enabling Custom Edge Silicon

- 4.3 Market Restraints

- 4.3.1 Cyber-Attack Surface Expansion at Distributed Nodes

- 4.3.2 Skills Gap in Deploying and Managing Heterogeneous Edge Stacks

- 4.3.3 Inter-Operability and Standards Fragmentation (MEC, Open-RAN, LF Edge)

- 4.3.4 Inefficient ROI for Brown-Field Industrial Retro-Fits

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Industry

- 5.3.1 Manufacturing and Industrial

- 5.3.2 Energy and Utilities

- 5.3.3 Healthcare and Life Sciences

- 5.3.4 Retail and E-Commerce

- 5.3.5 Banking, Financial Services, and Insurance (BFSI)

- 5.3.6 Telecommunications and IT

- 5.3.7 Other End-User Industries

- 5.4 By Application

- 5.4.1 Industrial IoT and Predictive Maintenance

- 5.4.2 Video Analytics and Surveillance

- 5.4.3 Autonomous Vehicles and Drones

- 5.4.4 Other Applications

- 5.5 By Organisation Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Huawei Technologies Co. Ltd.

- 6.4.5 IBM Corporation

- 6.4.6 Hewlett Packard Enterprise (HPE)

- 6.4.7 Dell Technologies Inc.

- 6.4.8 Google LLC (Alphabet Inc.)

- 6.4.9 Intel Corporation

- 6.4.10 NVIDIA Corporation

- 6.4.11 Juniper Networks Inc.

- 6.4.12 Advantech Co. Ltd.

- 6.4.13 ADLINK Technology Inc.

- 6.4.14 Schneider Electric SE

- 6.4.15 Siemens AG

- 6.4.16 Capgemini Engineering

- 6.4.17 MachineShop Inc.

- 6.4.18 Vapor IO Inc.

- 6.4.19 Litmus Automation

- 6.4.20 FogHorn Systems

- 6.4.21 Lumen Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment