PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035102

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035102

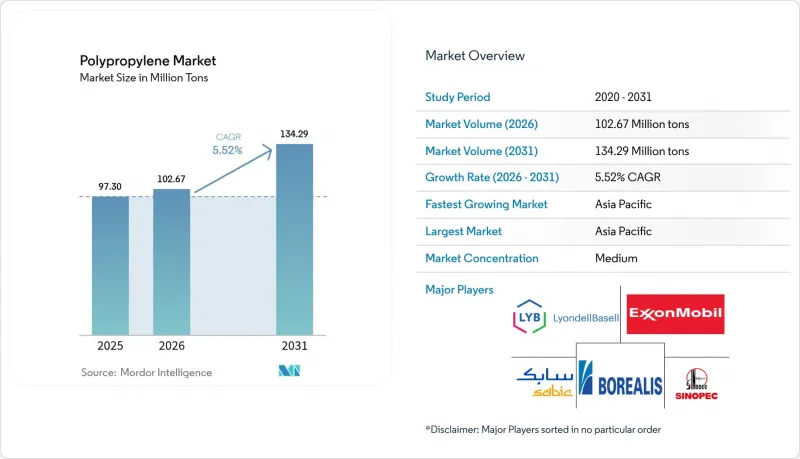

Polypropylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Polypropylene Market size was valued at 97.30 million tons in 2025 and estimated to grow from 102.67 million tons in 2026 to reach 134.29 million tons by 2031, at a CAGR of 5.52% during the forecast period (2026-2031).

Sustained demand in flexible packaging, automotive lightweighting, and non-woven fiber applications underpins this expansion, while propane-dehydrogenation (PDH) investments compress cash costs and shore up regional competitiveness. Producers are channeling capital toward specialty catalyst systems that yield high-melt-strength grades, enabling foamed parts that cut material use and vehicle weight. Rapid scale-up of chemical-recycling supply agreements is opening premium outlets for recycled feedstocks, although virgin resin volumes still dominate. At the same time, regulatory divergence-exemplified by the EU plastics tax-nudges converters toward mono-material structures, intensifying competition with polyethylene terephthalate and advanced polyethylene films.

Global Polypropylene Market Trends and Insights

Lightweighting Push in Automotive and E-Mobility

Automakers targeting extended battery range are replacing metal assemblies with high-melt-strength polypropylene foams that cut part mass by up to 40% while retaining crashworthiness, particularly in instrument panels and under-hood shields Integrated catalyst systems now produce propylene-based elastomers that displace rubber grommets and seals, offering designers consolidation opportunities that trim assembly time. Tier-one suppliers are shifting tooling strategies toward thin-wall injection molding to optimize cycle times, spurring a fresh wave of press retrofits across Europe. North American OEMs are aligning resin selection matrices with end-of-life recyclability targets, giving an additional boost to mono-material interiors. The resulting 6.29% CAGR for automotive applications positions the polypropylene market as a pivotal beneficiary of electrification trends.

Exploding Demand for Mono-Material Flexible Packaging

Global brands have fast-tracked voluntary targets demanding 100% recyclable packaging by 2025, prompting converters to abandon multi-layer laminates in favor of barrier-coated polypropylene films. European supermarkets now specify shelf-ready pouches made from single-polymer structures to minimize extended-producer-responsibility fees, sparking a surge in proprietary surface-treatment lines. Asia-Pacific packagers, capitalizing on economies of scale, are adopting solvent-free lamination technologies that deliver high-speed runs while meeting food-contact compliance. As a result, packaging retains the largest volume base yet transitions toward higher-margin barrier formats that command premium pricing. The migration also elevates bale purity in mechanical recycling streams, indirectly raising demand for recycled polypropylene pellets among fast-moving consumer-goods companies in the polypropylene market.

Availability of High-Performance Substitute Resins

Product developers in flexible packaging are increasingly testing metallized polyethylene films that match polypropylene's oxygen barrier while delivering lower sealing temperatures, eroding polypropylene's historic cost advantage. In beverage closures, polyester suppliers tout chemical-recycling content and superior clarity to capture sustainability-oriented brand guidelines. Acrylonitrile-butadiene-styrene (ABS) continues to win share in consumer electronics m-covers through higher surface gloss and impact resistance, pressuring polypropylene in premium aesthetics. Resin makers counter by launching inspired polypropylene grades with boosted stiffness-to-impact ratios, but adoption hinges on converter willingness to requalify molds. The tug-of-war intensifies as material selection teams weigh mechanical performance against recyclability targets, creating a net 0.9 percentage-point drag on forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Surge of PDH Units Lowering Cash Cost

- High-Melt-Strength PP Enabling Foamed, Low-Density Applications

- Crude-Oil and Propylene Price Volatility Squeezing Converter Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Homopolymer accounted for 69.53% of polypropylene market share in 2025, reflecting price sensitivity in caps, closures, and yarns where stiffness-to-weight ratio is paramount. The segment is forecast to post a 5.63% CAGR supported by PDH-driven cost competitiveness, with the polypropylene market size for homopolymers expected to reach 93.37 million tons by 2031. Producers are narrowing molecular-weight distributions using loop-reactor technology, enhancing clarity without sacrificing rigidity, which aids transition from random copolymer in dairy containers. Copolymers, while smaller in tonnage, secure premium pricing in impact-critical parts such as automotive bumpers and washing-machine tubs. Continuous catalyst upgrades blur the historical performance gap, enabling hybrid products that echo copolymer toughness at near-homopolymer economics. This convergence keeps procurement teams attentive to total-installed-cost rather than headline resin price, sustaining homopolymer's dominant share even as specialty grades expand.

Second-generation gas-phase reactors allow rapid grade switches, reducing transition scrap and favoring just-in-time logistics demanded by consumer-goods converters. Impact copolymers leveraging ethylene-propylene rubber domains gain traction in cold-climate automotive fascia owing to reliable low-temperature ductility. Random copolymers maintain a niche in medical syringes requiring gamma-sterilization stability. Yet rising sterilization-resistant additives in homopolymer blends signal potential future cannibalization. As additive master-batch formulations mature, homopolymer volumes could siphon incremental growth from copolymer, cementing their scale advantage.

The Polypropylene Market Report is Segmented by Type (Homopolymer, Copolymer), Processing Technology (Injection Molding, Blow Molding, Extrusion Molding, and Others), End-User Industry (Packaging, Automotive, Consumer Products, Electrical and Electronics, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific's 58.78% share underscores the region's manufacturing heft, but China's 68% production surge in 2025 spawned oversupply that pressured margins and spurred anti-dumping actions in Indonesia and the Philippines. Provincial governments are now scrutinizing environmental approvals for new PDH projects, tempering future capacity creep. India's downstream demand is accelerating as consumer-goods penetration deepens; the country's upcoming USD 8 billion ethane cracker promises to narrow import dependency, reshuffling intra-Asian trade.

North America leverages PDH feedstock advantages and proximity to a resurgent automotive sector in the polypropylene market, translating into competitive export offerings to South America and Europe. Ethane-rich shale gas underpins low propylene cash costs, enabling Gulf Coast plants to run at high utilization despite global volatility. Canada's Sarnia-based crackers feed into Midwestern converters through well-established rail logistics, fortifying regional supply security.

Europe faces twin headwinds of elevated energy pricing and stringent waste regulations. Producers are evaluating permanent shutdowns or conversions to recycled-feedstock platforms to stay compliant with the EU Packaging and Packaging Waste Regulation. Concurrently, polymer trade flows from the Middle East into Europe expand as integrated refinery-petrochemical hubs exploit low naphtha costs, while Turkish converters act as trading gateways into the EU customs union. South America, largely import-dependent, is courting upstream investment; however, currency volatility and policy uncertainty delay large-scale grassroots projects.

- Borealis AG

- Braskem

- China National Petroleum Corporation

- Ducor Petrochemicals

- Exxon Mobil Corporation

- Formosa Plastics Corporation

- Hanwha Total Petrochemical Co., Ltd

- HMC Polymers Company Limited

- INEOS

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals Inc.

- OQ SAOC

- PJSC SIBUR Holding

- Reliance Industries Limited

- SABIC

- Sinopec

- Sumitomo Chemical Co. Ltd.

- TotalEnergies

- Trinseo PLC

- Vioneo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting Push in Automotive and E-Mobility

- 4.2.2 Exploding Demand for Mono-Material Flexible Packaging

- 4.2.3 Capacity Surge of Propane-Dehydrogenation (PDH) Units Lowering Cash-Cost

- 4.2.4 High-Melt-Strength PP Enabling Foamed, Low-Density Applications

- 4.2.5 Rapid Scale-Up of Chemical-Recycling Supply Agreements

- 4.3 Market Restraints

- 4.3.1 Availability of High-Performance Substitute Resins (PE, PET, ABS)

- 4.3.2 Crude-Oil and Propylene Price Volatility Squeezing Converter Margins

- 4.3.3 EU Plastics Tax Steering Converters Toward Mono-PE Laminates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Price Trends

- 4.7 Import-Export Trends

- 4.8 Feedstock Analysis

- 4.9 Technological Snapshot

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Homopolymer

- 5.1.2 Copolymer

- 5.2 By Processing Technology

- 5.2.1 Injection Molding

- 5.2.2 Blow Molding

- 5.2.3 Extrusion Molding

- 5.2.4 Others

- 5.3 By End-user Industry

- 5.3.1 Packaging

- 5.3.2 Automotive

- 5.3.3 Consumer Products

- 5.3.4 Electrical and Electronics

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Borealis AG

- 6.4.2 Braskem

- 6.4.3 China National Petroleum Corporation

- 6.4.4 Ducor Petrochemicals

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Formosa Plastics Corporation

- 6.4.7 Hanwha Total Petrochemical Co., Ltd

- 6.4.8 HMC Polymers Company Limited

- 6.4.9 INEOS

- 6.4.10 LG Chem

- 6.4.11 LyondellBasell Industries Holdings B.V.

- 6.4.12 Mitsubishi Chemical Group Corporation

- 6.4.13 Mitsui Chemicals Inc.

- 6.4.14 OQ SAOC

- 6.4.15 PJSC SIBUR Holding

- 6.4.16 Reliance Industries Limited

- 6.4.17 SABIC

- 6.4.18 Sinopec

- 6.4.19 Sumitomo Chemical Co. Ltd.

- 6.4.20 TotalEnergies

- 6.4.21 Trinseo PLC

- 6.4.22 Vioneo

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment