PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035109

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035109

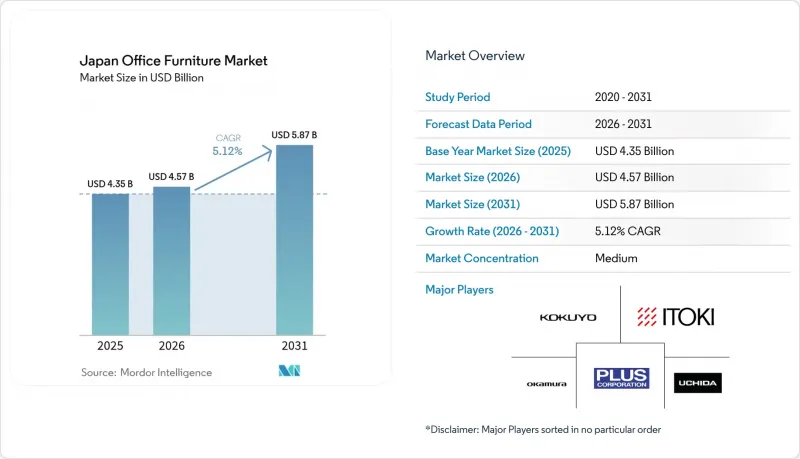

Japan Office Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Japan Office Furniture Market size in 2026 is estimated at USD 4.57 billion, growing from 2025 value of USD 4.35 billion with 2031 projections showing USD 5.87 billion, growing at 5.12% CAGR over 2026-2031.

Hybrid work models, government telework incentives, and activity-based working (ABW) layouts are reshaping purchasing criteria toward flexible, technology-enabled furnishings that improve well-being and space efficiency. Renovation cycles that were deferred during the pandemic have restarted as corporate balance sheets stabilize and as landlords compete through premium amenity upgrades. Kanto's dominance anchors national demand, yet rapid growth in Kyushu-Okinawa signals geographic diversification of corporate expansions. High market concentration enables incumbents to scale R&D on sensor-fitted furniture, though it also limits price competition for mid-sized buyers.

Japan Office Furniture Market Trends and Insights

Stagnant GDP-linked renovation cycles rebounding post-COVID

The stabilization of GDP in 2024 facilitated the release of capital budgets that had been restricted during the pandemic. This development allowed property owners and tenants to address deferred investments in workspace enhancements, reflecting a renewed focus on improving operational efficiency and meeting evolving workplace demands. Flexible desks, acoustic pods, and IoT-ready seating form the core of these upgrade packages, rewarding suppliers that bundle traditional craftsmanship with embedded connectivity. Fiscal-year 2025 budgets earmark larger allocations for workplace modernization, accelerating order volumes for modular fittings that cut installation time. Compliance with newer MHLW safety guidelines further shortens furniture life cycles within large corporates.

Corporate demand for activity-based working (ABW) layouts

Large enterprises are abandoning fixed seating in favour of zones dedicated to focus, collaboration, and relaxation, a shift proven to lift creative performance in peer-reviewed studies. Modular tables, lightweight partitions, and locker-based storage allow rapid reconfiguration as teams fluctuate between onsite and remote. Employee satisfaction surveys show 90% approval rates for ABW workstyles, enabling procurement teams to justify premium prices for specialized furniture. Manufacturers respond with quick-lock casters, stackable power rails, and upholstery options that dampen open-office noise without sacrificing visual openness. As hybrid attendance patterns normalize, ABW's emphasis on spatial adaptability positions it as a long-run growth engine for the Japan office furniture market.

Declining white-collar workforce due to aging demographics

Japan's working-age population continues to contract as retirements outpace new entrants, trimming aggregate desk demand. Leading corporations are strategically reducing their office footprints, as evidenced by the adoption of desk-sharing models and the downsizing of headquarters. This shift is particularly evident in manufacturing-centric regions, where corporate consolidations have resulted in an increased availability of office space. In urban centres, the inflow of foreign labour has mitigated some of the impacts of these changes; however, suburban suppliers are experiencing a decline in order volumes due to reduced demand. The hybrid work model has partially supported the furniture market by driving higher ergonomic standards for home offices. Nevertheless, the overall growth in furniture unit sales is projected to decelerate over the long term, reflecting a broader adjustment in market dynamics.

Other drivers and restraints analyzed in the detailed report include:

- Government tax incentives for telework-supportive furniture

- Ergonomic-related occupational-health regulations

- High urban rents are limiting large office refurbishments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wood retained 53.86% Japan office furniture market share in 2025, sustained by cultural affinity for natural aesthetics and traditional joinery. Import dependence, however, exposes costs to global timber volatility, pushing buyers to experiment with recycled and bio-based composites that lower carbon footprints. Plastics segment accelerates at 7.74% CAGR, fuelled by advances in post-consumer resin blends that satisfy ESG audits without sacrificing structural integrity. Metal frames remain indispensable for sit-stand desks where durability and motorized actuation require steel or aluminium substructures.

Plastics' growth also stems from their compatibility with embedded sensors, because moulded cavities simplify housing for IoT modules. Domestic OEMs trial biomass-derived polypropylene while international brands test ocean-bound plastics for chair shells aimed at environmentally sensitive procurement teams. Meanwhile, wood suppliers pursue chain-of-custody certification to preserve their premium positioning. Pilot projects using domestic cedar have raised utilization rates marginally above 40%, yet volume scale-up awaits mechanized drying and lamination upgrades in rural mills. Against this backdrop, circular models such as Kokuyo-ChopValue's chopstick-based panels hint at a hybrid future where waste streams supply next-generation wood composites.

Japan Office Furniture Market Report is Segmented by Material (Wood, Metal, and More), Product (Meeting Chairs, Lounge Chairs, and More), and Distribution Channel (Multi-Branded Stores, Specialty Stores, and More), and Geography (Kanto, Kansai, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kokuyo Co., Ltd.

- Itoki Corporation

- Okamura Corporation

- Plus Corporation

- Uchida Yoko Co., Ltd.

- Lion Office Products Co., Ltd.

- Askul Corporation

- Nakabayashi Co., Ltd.

- Tsubota Co., Ltd.

- Hatano Seating Co., Ltd.

- Karimoku Furniture Inc.

- Muji (Ryohin Keikaku Co., Ltd.)

- IKEA Japan K.K.

- Nitori Co., Ltd.

- Steelcase Inc.

- Herman Miller Japan

- Haworth Japan

- HNI Corporation (Japan)

- Karbox

- Sugatsune Kogyo Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stagnant GDP-linked renovation cycles rebounding post-COVID

- 4.2.2 Corporate demand for activity-based working (ABW) layouts

- 4.2.3 Government tax incentives for telework-supportive furniture

- 4.2.4 Ergonomic-related occupational-health regulations

- 4.2.5 Growing secondary-market "OFFICE-Reuse" export restrictions lift

- 4.2.6 AI-enabled space-utilisation analytics driving sensor-fitted desks

- 4.3 Market Restraints

- 4.3.1 Declining white-collar workforce due to ageing demographics

- 4.3.2 High urban rents limiting large office refurbishments

- 4.3.3 Raw-material cost volatility in engineered wood imports

- 4.3.4 Lagging standardisation of IoT protocols across furniture OEMs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Material

- 5.1.1 Wood

- 5.1.2 Metal

- 5.1.3 Plastics

- 5.1.4 Other Materials

- 5.2 By Product

- 5.2.1 Meeting Chairs

- 5.2.2 Lounge Chairs

- 5.2.3 Swivel Chairs

- 5.2.4 Office Tables

- 5.2.5 Storage Cabinets

- 5.2.6 Desks

- 5.3 By Distribution Channel

- 5.3.1 Multi-branded Stores

- 5.3.2 Specialty Stores

- 5.3.3 Online Platforms

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 Kanto

- 5.4.2 Kansai

- 5.4.3 Chubu

- 5.4.4 Kyushu-Okinawa

- 5.4.5 Tohoku

- 5.4.6 Hokkaido

- 5.4.7 Chugoku-Shikoku

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Kokuyo Co., Ltd.

- 6.4.2 Itoki Corporation

- 6.4.3 Okamura Corporation

- 6.4.4 Plus Corporation

- 6.4.5 Uchida Yoko Co., Ltd.

- 6.4.6 Lion Office Products Co., Ltd.

- 6.4.7 Askul Corporation

- 6.4.8 Nakabayashi Co., Ltd.

- 6.4.9 Tsubota Co., Ltd.

- 6.4.10 Hatano Seating Co., Ltd.

- 6.4.11 Karimoku Furniture Inc.

- 6.4.12 Muji (Ryohin Keikaku Co., Ltd.)

- 6.4.13 IKEA Japan K.K.

- 6.4.14 Nitori Co., Ltd.

- 6.4.15 Steelcase Inc.

- 6.4.16 Herman Miller Japan

- 6.4.17 Haworth Japan

- 6.4.18 HNI Corporation (Japan)

- 6.4.19 Karbox

- 6.4.20 Sugatsune Kogyo Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 Circular-economy furniture leasing models for corporate sustainability goals

- 7.2 Smart sensor-integrated ergonomic desks aligned with hybrid-work analytics