PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035138

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035138

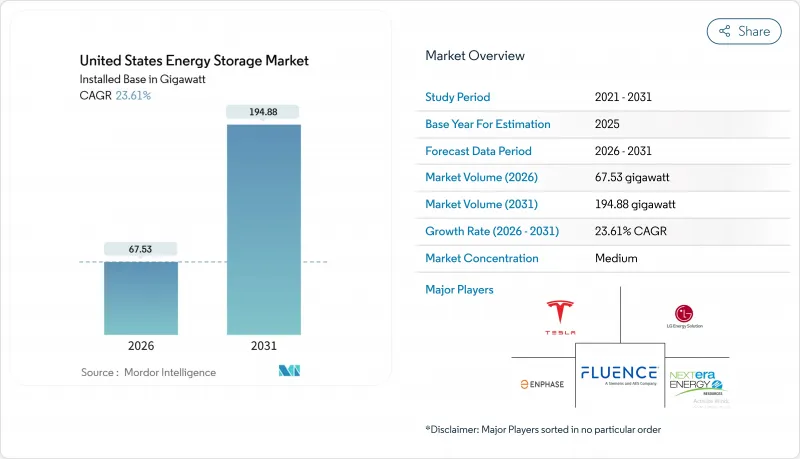

United States Energy Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States Energy Storage Market size in terms of installed base is expected to grow from 67.53 gigawatt in 2026 to 194.88 gigawatt by 2031, at a CAGR of 23.61% during the forecast period (2026-2031).

Declining battery costs, federal tax credits, and ISO/RTO market reforms are aligning to shorten payback periods and accelerate project pipelines. Section 45X production incentives are cutting the landed cost of domestic lithium-ion packs by 15%, while FERC rules that let aggregated batteries earn capacity, energy-arbitrage, and ancillary-service revenues have created entirely new income streams. Utilities are turning to storage to replace retiring coal units and to support solar and wind additions, and commercial customers view batteries as insurance against outages and peak charges. Supply-chain localization, long-duration technology breakthroughs, and virtual power plant enrollment programs together are expected to keep the growth trajectory intact even as wholesale prices soften.

United States Energy Storage Market Trends and Insights

Federal Investment Tax Credit Extension Boosting Residential Storage Demand

The 30% standalone storage credit now available until 2032 unlocked a surge of retrofit sales as households add batteries to existing rooftop solar arrays. Residential installations rose 42% year over year in 2025, with California, Texas, and Arizona responsible for 68% of those additions. Tesla's Powerwall 3, featuring 13.5 kWh usable capacity and an integrated hybrid inverter, captured roughly 35% of the residential segment by mid-2025. Enphase Energy shipped 29% more IQ Battery units during Q1 2025 as installers bundled storage with new solar projects to maximize customer tax savings. Time-of-use rates that peak during evening hours let homeowners trim monthly bills by USD 80-150, and virtual power plant programs add USD 300-700 in annual grid-service revenue per participant. The decade-long policy certainty is therefore accelerating adoption and smoothing demand cycles.

FERC Order 841 & 2222 Accelerating Wholesale-Market Participation of Storage

Regional transmission organizations have opened roughly 15 GW of incremental market access since 2024. CAISO registered 6.2 GW of active battery participation by Q3 2025, with storage supplying up to 18% of evening peak demand on high-load days. ERCOT activated its aggregated-resource protocol in early 2025, enrolling more than 800 MW of behind-the-meter batteries within six months. PJM cleared 2.1 GW of storage in its 2025 capacity auction after revising rules that now pay batteries meeting four-hour duration thresholds. NYISO participation tripled between 2024 and 2025 to 1.8 GW as developers capitalized on locational premiums in densely populated zones. These reforms reposition storage from a niche ancillary-service asset into a dependable dispatchable resource that directly displaces gas peakers.

Interconnection Queue Congestion Delaying Large-Scale Projects

Backlogs in PJM, MISO, and SPP exceeded 120 GW of storage and hybrid capacity by mid-2025, with average wait times surpassing 42 months. FERC's cluster-study directive will help, but regional implementation lags, and developers face upgrade fees above USD 50 per kW that erode project economics. MISO recorded a 38% withdrawal rate in 2024 as sponsors abandoned delayed projects. SPP's 18 GW storage queue delivered only 1.2 GW of commercial operations between 2024 and 2025. These constraints push new capacity toward ERCOT and CAISO, which process interconnections within two years and offer clearer cost allocations.

Other drivers and restraints analyzed in the detailed report include:

- Solar-plus-Storage Pipeline Growth Across ERCOT and WECC

- IRA-Linked Domestic Battery-Manufacturing Credits Lowering BESS Cost

- PFAS Li-ion Electrolyte Safety Concerns Triggering Stricter Fire Codes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The energy storage systems in the United States market saw batteries secure 81.7% of installed capacity in 2025, leveraging lithium-ion packs that cost USD 271 per kWh for utility-scale projects in 2024. Lithium-iron-phosphate and high-nickel NMC chemistries together account for about 95% of shipments, supported by domestic gigafactories that enjoy 45X credits. Lead-acid retains a 3% niche, while vanadium-flow and zinc-bromine pilots address applications needing 6- to 10-hour discharge. The energy storage systems in the United States market share for pumped hydro remains minimal for new builds because siting options are limited, though existing facilities continue to provide inertia.

Hydrogen storage is poised for a 30.5% CAGR through 2031, spurred by utility solicitations for 100-hour discharge capability. Mitsubishi Power is converting a Utah coal plant into a 300 MW hydrogen-fueled generator that will store electrolytic hydrogen in salt caverns. Compressed-air projects, such as Hydrostor's 500 MW California development, offer 8-hour durations at lower capital cost than hydrogen. Flywheel and thermal systems continue to serve frequency and industrial heat niches, respectively, each well under 1% of capacity.

The 10-100 MWh class held 38.6% of 2025 capacity, reflecting utility preference for modular 20-50 MW blocks that match solar projects and avoid complex transmission upgrades. Fluence Gridstack and Powin Centipede dominate this tier with factory-assembled containers that compress construction schedules. Energy storage systems in the United States market size for this band is set to rise steadily as distribution utilities deploy feeder-scale assets to defer substation upgrades.

Projects above 100 MWh are expanding at a 36.1% CAGR. Vistra's Moss Landing site in California reached 750 MW / 3,000 MWh in 2024, demonstrating the economic case for gigawatt-hour-scale batteries. AES and LS Power have multiple 300 MWh-plus projects underway in Texas and Nevada to exploit scarcity pricing and capacity payments. Sub-1 MWh systems serve the residential sector, where attachment rates in California exceeded 85% for new rooftop solar in 2025.

The United States Energy Storage Market Report is Segmented by Technology (Batteries, Pumped Hydro Storage, Hydrogen Energy Storage, and More), Capacity Rating (Up To 1 MWh, 1 To 10 MWh, 10 To 100 MWh, and Above 100 MWh), Installation (Front-Of-The-Meter and Behind-The-Meter), Application (Renewable Integration, Peak Shaving and Demand Charge Management, and More), and End User (Residential, Commercial and Industrial, and Utility).

List of Companies Covered in this Report:

- Tesla Inc.

- Fluence Energy LLC

- LG Energy Solution Ltd.

- Sungrow Power Supply Co. Ltd.

- BYD Co. Ltd.

- Enphase Energy Inc.

- NextEra Energy Resources LLC

- AES Corporation

- Powin Energy Corp.

- Samsung SDI Co. Ltd.

- Panasonic Holdings Corp.

- Eos Energy Enterprises Inc.

- EnerSys

- KORE Power Inc.

- Form Energy Inc.

- CATL

- Honeywell International Inc.

- Hydrostor Inc.

- Voith GmbH & Co. KGaA

- Andritz AG

- Siemens Energy AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal Investment Tax Credit Extension Boosting Residential Storage Demand

- 4.2.2 FERC Order 841/2222 Accelerating Wholesale?Market Participation of Storage

- 4.2.3 California Rule 21 & NEM 3.0 Driving Behind-the-Meter Deployments

- 4.2.4 Solar-plus-Storage Pipeline Growth Across ERCOT and WECC

- 4.2.5 IRA-Linked Domestic Battery-Manufacturing Tax Credits Lowering BESS Cost

- 4.2.6 Aggressive Utility IRPs Retiring Coal and Adding Long-Duration Storage

- 4.3 Market Restraints

- 4.3.1 Interconnection Queue Congestion Delaying Large-Scale Projects

- 4.3.2 PFAS Li-ion Electrolyte Safety Concerns Triggering Stricter Fire Codes

- 4.3.3 Uneven State-Level Incentives Undermining National Roll-out

- 4.3.4 Supply-Chain Critical-Minerals Exposure (Li, Ni, Co) to Geopolitical Risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Installed Capacity Analysis

- 4.9 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Batteries (Lithium-ion, Lead-acid, Flow Batteries, Sodium-sulfur and Others)

- 5.1.2 Pumped Hydro Storage

- 5.1.3 Compressed Air Energy Storage

- 5.1.4 Flywheel Storage

- 5.1.5 Thermal Energy Storage

- 5.1.6 Hydrogen Energy Storage

- 5.2 By Capacity Rating

- 5.2.1 Below 1 MWh

- 5.2.2 1 to 10 MWh

- 5.2.3 10 to 100 MWh

- 5.2.4 Above 100 MWh

- 5.3 By Installation

- 5.3.1 Front-of-the-Meter

- 5.3.2 Behind-the-Meter

- 5.4 By Application

- 5.4.1 Renewable Integration

- 5.4.2 Peak Shaving and Demand Charge Management

- 5.4.3 Frequency Regulation

- 5.4.4 Backup Power/Resilience

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial and Industrial

- 5.5.3 Utility

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tesla Inc.

- 6.4.2 Fluence Energy LLC

- 6.4.3 LG Energy Solution Ltd.

- 6.4.4 Sungrow Power Supply Co. Ltd.

- 6.4.5 BYD Co. Ltd.

- 6.4.6 Enphase Energy Inc.

- 6.4.7 NextEra Energy Resources LLC

- 6.4.8 AES Corporation

- 6.4.9 Powin Energy Corp.

- 6.4.10 Samsung SDI Co. Ltd.

- 6.4.11 Panasonic Holdings Corp.

- 6.4.12 Eos Energy Enterprises Inc.

- 6.4.13 EnerSys

- 6.4.14 KORE Power Inc.

- 6.4.15 Form Energy Inc.

- 6.4.16 CATL

- 6.4.17 Honeywell International Inc.

- 6.4.18 Hydrostor Inc.

- 6.4.19 Voith GmbH & Co. KGaA

- 6.4.20 Andritz AG

- 6.4.21 Siemens Energy AG

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment