PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035148

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035148

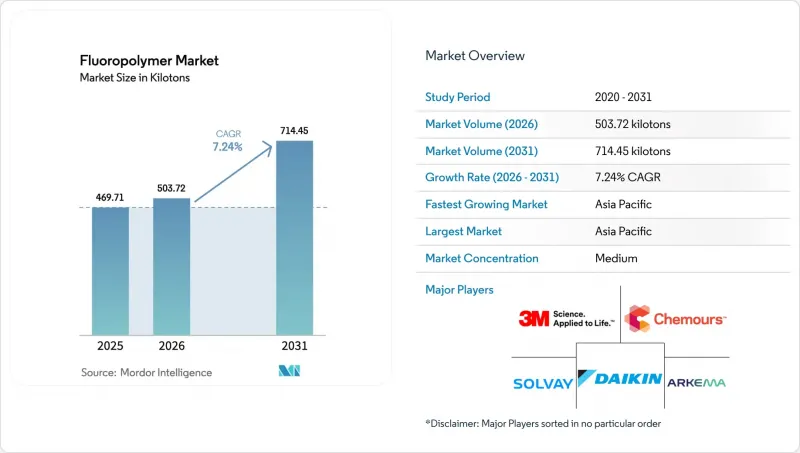

Fluoropolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Fluoropolymer market size is expected to grow from 469.71 kilotons in 2025 to 503.72 kilotons in 2026 and is forecast to reach 714.45 kilotons by 2031 at 7.24% CAGR over 2026-2031.

Sustained gains stem from electric-vehicle wire insulation, Asia-Pacific semiconductor fab expansion, and low-VOC coating mandates that favor fluoropolymer chemistries. Price resilience is linked to unmatched chemical inertness, thermal stability, and dielectric strength that extend service life and reduce maintenance costs for critical assets. Leading suppliers are deepening their vertical integration into fluorspar mining and downstream compounding to mitigate raw-material volatility. Process intensification and advances in membrane durability broaden the adoption of green-hydrogen projects. Collectively, these drivers reinforce multi-industry reliance, shielding the fluoropolymer market from cyclical downturns.

Global Fluoropolymer Market Trends and Insights

Surge in demand for high-performance wiring in EVs

Electric vehicles rely on cable insulation that withstands 800 V architectures, -40°C to 150°C thermal cycles, and electrolyte splash. PVDF and ETFE meet these stress profiles while maintaining flame retardancy that satisfies global OEM safety tests. Premium models such as Tesla Model S Plaid and Lucid Air Dream Edition specify fluoropolymer-insulated harnesses to secure continuous high-power operation under track conditions. Growth in 48 V mild-hybrid commercial vehicles broadens the addressable volume, and wire-and-cable compounders pre-qualify grades to shorten validation timelines for new EV platforms. Suppliers able to provide color-stable, irradiation-crosslinkable insulation grades gain specification wins as automakers compress development cycles. Continuous copper price pressure also pushes designers toward thinner-wall insulation, favoring high-dielectric-strength fluoropolymers.

Growing adoption of PVDF as Li-ion battery binder

PVDF replaced legacy binders by offering an electrochemical stability window to 4.6 V, enabling higher-nickel cathodes that lift pack energy density. Separator coatings and electrolyte additives extend PVDF's battery role and multiply revenue per kilowatt-hour. Chinese cell makers pair local PVDF resin with domestic lithium carbonate, minimizing import dependency and shortening lead times. Alternative water-based binders struggle with adhesion at high-temperature curing, keeping PVDF entrenched despite ongoing research and development in polyacrylic and biomaterial systems. As global gigafactory capacity surpasses 3 TWh by 2030, incremental binder demand alone sustains double-digit growth for PVDF suppliers. Producers investing in upstream VDF monomer capacity lock in feedstock and defend margins against raw-material price swings.

PFAS regulatory scrutiny in the US/EU

Broad PFAS proposals under EU REACH list more than 10,000 substances, covering fluoropolymers except where critical-use derogations apply. Uncertainty stalls expansion projects as investors weigh compliance costs against future cash flow. California's phased ban on certain food-contact articles illustrates how localized actions cascade through global supply chains, forcing OEMs to redesign. Semiconductor end-users lobby for exemptions, warning that wafer defect risk rises sharply without ultra-clean fluoropolymer tubing. Companies that proactively certify grades for low-extractable fluorinated additives improve their odds of securing derogations.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of semiconductor fab capacity in Asia

- Stringent low-VOC coating regulations

- High fluorspar costs and limited supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The PTFE category retained a 48.05% market share in the fluoropolymer market in 2025, driven by applications such as chemical-processing gaskets, aerospace seals, and semiconductor wafer carriers. The fluoropolymer market size for PTFE is expected to reach approximately 333.6 kilotons by 2031, driven by new demand for PFA-lined heat exchangers.

PVDF, by contrast, recorded an 17.1% CAGR and will cross 120 kilotons by 2031, fueled by lithium-ion cathode binders and proton-exchange membranes. China and South Korea account for 70% of incremental PVDF capacity announcements, aligning resin availability with the growth of battery gigafactory clusters. ETFE gains momentum in architectural roof membranes and 200°C EV wire jackets. FEP growth tracks semiconductor wet-bench upgrades given its ultra-low extractables profile. Smaller niches for PFA, ECTFE, and PVF persist where FDA 21 CFR compliance or photovoltaic backsheet durability is non-negotiable.

The Fluoropolymer Market Report is Segmented by Sub-Resin Type (ETFE, FEP, PTFE, PVF, and More), End-User Industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

The Asia-Pacific region owned 53.92% of the Fluoropolymer market in 2025 and is projected to grow at an 8.34% CAGR through 2031. China commands a significant portion of domestic resin capacity and dominates lithium-ion battery production, thereby ensuring a secure PVDF supply for local cathode manufacturers. Taiwan and South Korea invest heavily in sub-7 nm wafer fabrication, consuming ultra-pure PFA tubing and PTFE bellows to guard against contamination. India scales up EV manufacturing and chemical-processing projects that require corrosion-resistant fluoropolymer lining materials. Government incentives in Japan support the deployment of PEM electrolyzers, further boosting demand for PVDF and FEP membranes.

North America exhibits steady consumption in aerospace, defense, and specialty chemicals, where performance outweighs cost. The US also enforces strict VOC caps, prompting substitution toward waterborne PVDF coatings in architectural panels. Mexico's growing vehicle assembly output increases purchases of fluoropolymer tubing for battery coolant loops, and Canadian mining operations specify PTFE linings for acid-leach circuits. Overall growth is modest compared with Asia but underpinned by higher per-unit value applications that bolster margins.

Europe maintains focus on sustainability and regulatory compliance. The EU Green Deal catalyzes investment in green-hydrogen plants that require fluoropolymer membranes, while German OEMs ramp EV component lines that consume PVDF binder and cable insulation. Yet the proposed PFAS restriction under REACH injects uncertainty, delaying some capacity expansions until derogation clarity emerges. Critical-use exemptions for aerospace, medical, and semiconductor fields sustain premium-grade demand. South America, the Middle-East, and Africa register emerging growth as petrochemical and mining sectors modernize equipment with corrosion-proof linings, albeit from a smaller base, keeping their influence on the total Fluoropolymer market size moderate during the forecast.

- 3M

- Arkema

- Daikin Industries Ltd.

- Dongyue Group

- Gujarat Fluorochemicals Ltd. (GFL)

- Kureha Corporation

- Shanghai 3F New Materials

- Sinochem

- Syensqo

- The Chemours Company

- Toray Industries Inc.

- Zhejiang Juhua Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for high-performance wiring in EVs

- 4.2.2 Growing adoption of PVDF as Li-ion battery binder

- 4.2.3 Expansion of semiconductor fab capacity in Asia

- 4.2.4 Stringent low-VOC coating regulations

- 4.2.5 Green-hydrogen electrolysis membranes (PVDF, FEP)

- 4.3 Market Restraints

- 4.3.1 PFAS regulatory scrutiny in US/EU

- 4.3.2 High fluorspar costs and limited supply

- 4.3.3 Raw-material price volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Import and Export Analysis

- 4.7 Price Trends

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of Substitutes

- 4.8.4 Competitive Rivalry

- 4.8.5 Threat of New Entrants

- 4.9 End-use Sector Trends

- 4.9.1 Aerospace (Aerospace Component Production Revenue)

- 4.9.2 Automotive (Automobile Production)

- 4.9.3 Building and Construction (New Construction Floor Area)

- 4.9.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.9.5 Packaging(Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Sub-Resin Type

- 5.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.1.3 Polytetrafluoroethylene (PTFE)

- 5.1.4 Polyvinylfluoride (PVF)

- 5.1.5 Polyvinylidene Fluoride (PVDF)

- 5.1.6 Other Sub Resin Types

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Industrial and Machinery

- 5.2.6 Packaging

- 5.2.7 Other End-User Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Daikin Industries Ltd.

- 6.4.4 Dongyue Group

- 6.4.5 Gujarat Fluorochemicals Ltd. (GFL)

- 6.4.6 Kureha Corporation

- 6.4.7 Shanghai 3F New Materials

- 6.4.8 Sinochem

- 6.4.9 Syensqo

- 6.4.10 The Chemours Company

- 6.4.11 Toray Industries Inc.

- 6.4.12 Zhejiang Juhua Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs