PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035153

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035153

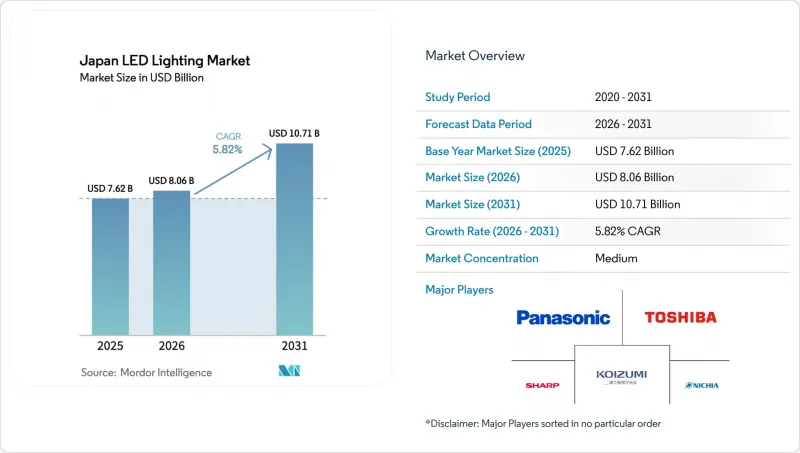

Japan LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Japan's LED lighting market size in 2026 is estimated at USD 8.06 billion, growing from 2025 value of USD 7.62 billion with 2031 projections showing USD 10.71 billion, growing at 5.82% CAGR over 2026-2031.

Steady expansion stems from the 2027 fluorescent-lamp ban mandated by the Minamata Convention, stringent revisions to the Energy Conservation Law, and the acceleration of smart-city programs that make connected luminaires an essential municipal asset. Supply-side resilience strategies adopted after China's export controls on gallium and germanium further reinforce domestic value addition, while premium applications such as UV-C disinfection and horticulture lighting preserve margins amid rising import competition. Retrofit upgrades dominate demand because Japan possesses a highly built urban fabric; however, new installations tied to smart poles and plant factories provide incremental volume. E-commerce also continues to reshape consumer access, especially in the residential segment, where deadline-driven replacement purchases are on the rise.

Japan LED Lighting Market Trends and Insights

Stringent Energy-Efficiency Mandates and Mercury-Lamp Phase-Out

Japan's convergence of the Minamata Convention's 2027 ban on fluorescent lighting and the upgraded Energy Conservation Law eliminates any remaining cost-benefit debate, making LED adoption compulsory across all sectors. Municipal subsidies such as Iwata City's JPY 30 million (USD 0.2 million) incentive accelerate residential conversions ahead of the deadline. Revised JIS Z 9112:2019 standards classify luminaires by application, creating premium niches for high-color-rendering units. Despite 60% consumer awareness, nearly half of households have not yet acted, underscoring latent demand that will be unlocked as the cutoff nears. Mandatory replacement removes uncertainty and ensures a structural growth runway for the Japan LED lighting market.

Post-Fukushima Retrofit Boom in Commercial and Residential Buildings

Electricity tariffs have surged 59% for households and 92% for industrial users since 2011, making energy-efficient lights integral to cost management. ESCO contracts, pioneered by firms such as Azbil, allow property owners to implement upgrades without upfront capital, guaranteeing future savings. Local governments lead by example: Yatsushiro City is auditing 290 facilities for complete LED conversion as part of its Zero Carbon strategy. National building codes require new structures to meet Net Zero Energy House standards by 2030, embedding advanced lighting into every construction plan. Retrofits, therefore, remain a dependable volume driver for the Japan LED lighting market well beyond the initial Fukushima recovery.

High Upfront Cost versus Legacy Fluorescents

Household consumers confront immediate out-of-pocket spending, and 45.7% have yet to begin replacements despite understanding the ban, confirming that price remains a hurdle. Many existing fixtures are incompatible with plug-in LED tubes, necessitating the replacement of entire luminaire fixtures, which further increases costs. Municipal programs, such as Iwata City's subsidy, partially ease the burden but cover a limited geography. The price barrier primarily delays the uptake of residential LED lighting in Japan; however, ongoing declines in LED costs and expanding incentives are expected to mitigate this constraint.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Smart-City and Smart-Pole Deployments

- OEM Shift to LED Headlamps in Japan-Built Vehicles

- Margin Squeeze from Low-Cost Imports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires captured 62.20% of Japan's LED lighting market share in 2025, reflecting user preference for integrated solutions with superior thermal management. Lamps, although smaller, are advancing at an 8.35% CAGR as consumers accelerate pre-deadline replacements of fluorescent bulbs. The luminaire's edge is rooted in safety: manufacturers such as Panasonic caution against retrofitting LED tubes into aging fluorescent housings due to the risk of fire. Integrated units also permit embedded wireless controls and occupancy sensors, features increasingly requested in premium office renovations.

Advanced fixture designs from Fukunishi Denki exhibit Panasonic's LiBecoM system, enabling activity-based dimming for further savings. Meanwhile, lamp-level growth benefits from high-CRI tube offerings specifically designed for photography studios and retail displays. Together, these trends ensure both categories contribute to sustained gains in the Japan LED lighting market.

Wholesale outlets accounted for 54.30% of 2025 sales, remaining vital for contractor-led projects and municipal tenders. Yet e-commerce is projected to clock a 7.12% CAGR through 2031, buoyed by Amazon Japan storefront launches from premium players like Lipro. BicCamera typifies hybrid strategies: its LED ceiling-light catalog combines online ordering with showroom demonstrations to reassure consumers about specifications.

Direct-sales integrators respond by bundling luminaires with installation and maintenance, defending share in complex commercial jobs. For standard residential fixtures, web platforms offer price transparency and next-day delivery, reinforcing the shift in consumer behavior. Digital purchasing thus unlocks new reach for the Japan LED lighting market, particularly among younger households.

The Japan LED Lighting Market Report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and E-Commerce), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, Hospitality, Industrial, and More), and End User (Indoor, Outdoor, and Automotive). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nichia Corporation

- Panasonic Holdings Corp.

- Toshiba Lighting and Technology Corp.

- Sharp Corporation

- Koizumi Lighting Technology Corp.

- Iwasaki Electric Co., Ltd.

- Endo Lighting Corp.

- Stanley Electric Co., Ltd.

- Citizen Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Odelic Co., Ltd.

- Iris Ohyama, Inc.

- Ushio Lighting, Inc.

- Mitsubishi Electric Lighting Corp.

- Rohm Co., Ltd.

- NEC Lighting, Ltd.

- Yamagiwa Corporation

- MinebeaMitsumi Inc.

- Optoelec Japan Co., Ltd.

- ICHIKOH Industries, Ltd.

- Kyocera SLD Laser Japan

- Kagoshima Murata Manufacturing Co., Ltd.

- Ushio Inc. (Spectral LED)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent energy-efficiency mandates and mercury-lamp phase-out

- 4.2.2 Post-Fukushima retrofit boom in commercial and residential buildings

- 4.2.3 Accelerating smart-city and smart-pole deployments

- 4.2.4 OEM shift to LED headlamps in Japan-built vehicles

- 4.2.5 Hospital demand for UV-C disinfection luminaires

- 4.2.6 Vertical-farm and horticulture LED demand spike

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs. legacy fluorescents

- 4.3.2 Margin squeeze from low-cost imports

- 4.3.3 Phosphor supply constraints for high-CRI devices

- 4.3.4 Strict WEEE recycling compliance costs

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale Retail

- 5.2.3 E-commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Others (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Panasonic Holdings Corp.

- 6.4.3 Toshiba Lighting and Technology Corp.

- 6.4.4 Sharp Corporation

- 6.4.5 Koizumi Lighting Technology Corp.

- 6.4.6 Iwasaki Electric Co., Ltd.

- 6.4.7 Endo Lighting Corp.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Citizen Electronics Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Odelic Co., Ltd.

- 6.4.12 Iris Ohyama, Inc.

- 6.4.13 Ushio Lighting, Inc.

- 6.4.14 Mitsubishi Electric Lighting Corp.

- 6.4.15 Rohm Co., Ltd.

- 6.4.16 NEC Lighting, Ltd.

- 6.4.17 Yamagiwa Corporation

- 6.4.18 MinebeaMitsumi Inc.

- 6.4.19 Optoelec Japan Co., Ltd.

- 6.4.20 ICHIKOH Industries, Ltd.

- 6.4.21 Kyocera SLD Laser Japan

- 6.4.22 Kagoshima Murata Manufacturing Co., Ltd.

- 6.4.23 Ushio Inc. (Spectral LED)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment