PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035159

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035159

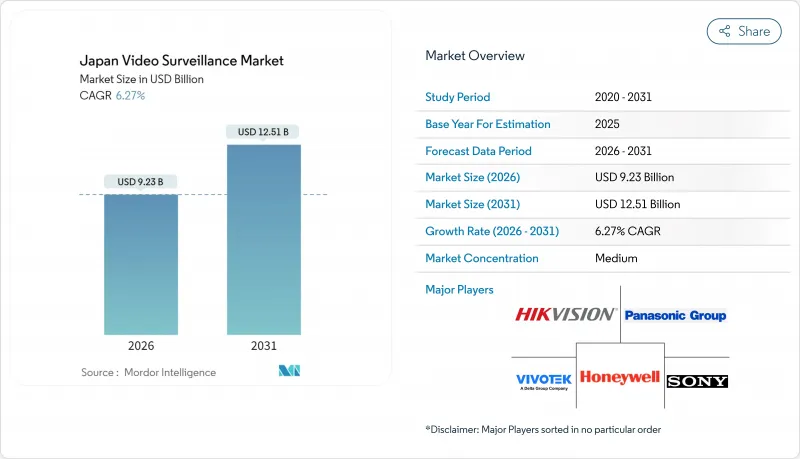

Japan Video Surveillance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan video surveillance market size stood at USD 9.23 billion in 2026, and it is projected to reach USD 12.51 billion by 2031, registering a CAGR of 6.27% over the forecast period.

Rising urban density, an aging demographic profile, and nationwide infrastructure-modernization mandates are reshaping procurement priorities across public and private sectors, pushing end users toward intelligent cameras, hybrid-cloud storage, and subscription licensing. Local authorities in Tokyo, Osaka, and Fukuoka now embed edge-capable sensors into smart-city platforms that visualize pedestrian flows and traffic anomalies in real time. Enterprises face labour shortages that make automated analytics attractive, while ministries enforce tighter data-protection rules that reward vendors able to anonymize footage on device. Hardware still dominates shipments, yet services are accelerating fastest, signalling a durable shift away from capex-heavy recorder swaps toward Video Surveillance as a Service. Collectively, these forces keep the Japan video surveillance market on a steady mid-single-digit growth trajectory despite component shortages and compliance frictions.

Japan Video Surveillance Market Trends and Insights

Smart City and Infrastructure Modernization Projects Accelerating Camera Deployment

Tokyo's 2024 Digital Twin roadmap obliges every new public-works site to stream high-resolution video into a municipal data lake that supports crowd-management dashboards. Rail operators follow suit: Keisei installed facial-recognition gates in January 2025, and JR Central began real-time overcrowding analytics on Tokaido Shinkansen platforms in January 2026. Airports updated security guidelines in 2024 to specify NEC and Secom biometrics, further enlarging the procurement pool. Collectively, these mandates elevate demand for ONVIF-compliant 4K cameras, low-latency encoders, and cloud-ready VMS. As deployments scale, the Japan video surveillance market benefits from stable multiyear budget allocations that mitigate cyclical spending dips.

Rapid Adoption of Edge-AI Cameras to Reduce Cloud Bandwidth Costs in Dense Urban Areas

NTT's 4K low-power LSI, announced in 2024, runs object detection on camera boards, cutting upstream bandwidth by up to 80%. i-PRO's 2024 U-series introduces on-site learning so retailers can train custom classifiers without exporting raw footage. Ambarella chipsets now promise scene-to-text conversion at the edge, enabling natural-language search across distributed fleets. Early adopters include logistics depots and factory floors that require sub-100-millisecond responses to avoid robotic downtime. Because edge inference slashes recurring egress fees, it directly supports subscription uptake, reinforcing the long-term growth profile of the Japan video surveillance market.

Stringent Data Protection Regulations Limiting Facial Recognition Use

The 2022 revision of the Act on the Protection of Personal Information, enforced aggressively from 2024, brands facial images as sensitive data that require explicit opt-in or statutory carve-outs. Retailers piloting continuous recognition faced backlash, prompting JR East to pause one line's trial in April 2025. Compliance now demands anonymization filters, consent dashboards, and audit logs capabilities smaller integrators struggle to fund. These overheads lengthen sales cycles and trim near-term uptake, shaving growth off the Japan video surveillance market until vendors standardize low-friction privacy guards.

Other drivers and restraints analyzed in the detailed report include:

- Aging Population Driving Demand for Elderly-Care Monitoring in Smart Homes and Hospitals

- Integration of Video Surveillance with Digital Twins in Manufacturing for Predictive Maintenance

- Semiconductor Supply Volatility Increasing Hardware Lead Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is rising at a 7.11% CAGR to 2031, outpacing both hardware and software as businesses favour predictable operating costs over capex. In 2025, hardware still delivered 57.01% of turnover, reflecting the large installed camera base and the necessity to swap aging analog units. Safie manages 186,000 cloud cameras and posts 31% annual subscriber growth, illustrating the appeal of frictionless onboarding for small retailers. Software sits in the middle, leveraging AI modules that auto-index footage and accelerate incident review. Milestone's 2025 natural-language plug-in reduces search time by 70% in pilots. As firmware moves to the cloud, hardware vendors embed AI chips and sell licenses per analytic function, blurring category lines. Because these shifts reallocate value capture, the Japan video surveillance market now rewards platforms that bundle upgrade paths across the lifecycle.

The Japan video surveillance market size linked to services is projected to climb from USD 2.9 billion in 2026 to more than USD 4.1 billion by 2031 as VSaaS converts legacy NVR estates. Hybrid bundles that pair on-premises recorders with cloud retention help industrial plants satisfy air-gap requirements without forfeiting remote dashboards. Hardware revenues plateau in unit terms yet stay resilient in value because buyers migrate to 4K sensors with higher ASPs. Software maintains low-double-digit growth as analytics expand from security to business intelligence, such as queue-length detection and merchandising heat maps.

Commercial premises generated 38.54% of 2025 revenue, making offices, malls, and hospitality chains the largest buyers of multi-site VMS. Yet residential installations are slated to post the fastest 6.56% CAGR, widening smart-home penetration as homeowners integrate cameras with HVAC and energy dashboards. Panasonic's HomeX crossed 100,000 users by March 2025, validating bundled ecosystems. Subsidies in the 2025 rural digital-inclusion plan pay up to 30% of device costs, narrowing the affordability gap outside major metros.

Infrastructure applications, including airports, rail, and highways, gain funding through the Tokyo Digital Twin and MLIT airport guidelines. Industrial demand intensifies as factories overlay video onto digital twins for predictive maintenance, reinforcing the Japan video surveillance market share held by manufacturing hubs. Defense and critical-infrastructure clients prioritize encrypted streams and long firmware support, favouring domestic suppliers with local service teams. Across all verticals, integration depth rather than camera count dictates spend, a dynamic that shifts margins toward vendors offering open APIs and analytics libraries.

The Japan Video Surveillance Market Report is Segmented by Component (Hardware [Camera, and Storage], Software, and Services), End-User Vertical (Commercial, Infrastructure, Institutional, Industrial, Defense, and Residential), Deployment Mode (On-Premise, Hosted VSaaS, Managed VSaaS, and Hybrid VSaaS), and Camera Resolution (Standard Definition, High Definition, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Panasonic Connect Co., Ltd.

- Honeywell International Inc.

- Sony Corporation

- Hangzhou Hikvision Digital Technology Co. Ltd

- Zhejiang Dahua Technology Co., Ltd.

- Axis Communications AB

- NEC Corporation

- Canon Inc.

- VIVOTEK Inc.

- Johnson Controls International plc

- Bosch Sicherheitssysteme GmbH

- Hanwha Vision Co. Ltd

- Avigilon Corporation

- Genetec Inc.

- Milestone Systems A/S

- Eagle Eye Networks, Inc.

- Verkada Inc.

- SECOM Co., Ltd.

- Fujitsu Limited

- TESCOM Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Public and Private Investments in Security and Surveillance Systems

- 4.2.2 Technological Innovation in Video Surveillance Solutions

- 4.2.3 Smart City and Infrastructure Modernization Projects Accelerating Camera Deployment

- 4.2.4 Rapid Adoption of Edge AI Cameras to Reduce Cloud Bandwidth Costs in Dense Urban Areas

- 4.2.5 Integration of Video Surveillance with Digital Twins in Manufacturing for Predictive Maintenance

- 4.2.6 Aging Population Driving Demand for Elderly Care Monitoring in Smart Homes and Hospitals

- 4.3 Market Restraints

- 4.3.1 Privacy and Security Concerns

- 4.3.2 Stringent Data Protection Regulations Limiting Facial Recognition Use

- 4.3.3 Semiconductor Supply Volatility Increasing Hardware Lead Times

- 4.3.4 Shortage of Skilled Video Analytics Professionals Hindering VSaaS Adoption

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Snapshot

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Camera

- 5.1.1.1.1 Analog

- 5.1.1.1.2 IP Cameras

- 5.1.1.1.3 Hybrid

- 5.1.1.2 Storage

- 5.1.1.1 Camera

- 5.1.2 Software

- 5.1.2.1 Video Analytics

- 5.1.2.2 Video Management Software

- 5.1.3 Services (VSaaS)

- 5.1.1 Hardware

- 5.2 By End-user Vertical

- 5.2.1 Commercial

- 5.2.2 Infrastructure

- 5.2.3 Institutional

- 5.2.4 Industrial

- 5.2.5 Defense

- 5.2.6 Residential

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Hosted VSaaS

- 5.3.3 Managed VSaaS

- 5.3.4 Hybrid VSaaS

- 5.4 By Camera Resolution

- 5.4.1 Standard Definition (SD)

- 5.4.2 High Definition (HD)

- 5.4.3 Full HD (1080p)

- 5.4.4 4K and Above

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Panasonic Connect Co., Ltd.

- 6.4.2 Honeywell International Inc.

- 6.4.3 Sony Corporation

- 6.4.4 Hangzhou Hikvision Digital Technology Co. Ltd

- 6.4.5 Zhejiang Dahua Technology Co., Ltd.

- 6.4.6 Axis Communications AB

- 6.4.7 NEC Corporation

- 6.4.8 Canon Inc.

- 6.4.9 VIVOTEK Inc.

- 6.4.10 Johnson Controls International plc

- 6.4.11 Bosch Sicherheitssysteme GmbH

- 6.4.12 Hanwha Vision Co. Ltd

- 6.4.13 Avigilon Corporation

- 6.4.14 Genetec Inc.

- 6.4.15 Milestone Systems A/S

- 6.4.16 Eagle Eye Networks, Inc.

- 6.4.17 Verkada Inc.

- 6.4.18 SECOM Co., Ltd.

- 6.4.19 Fujitsu Limited

- 6.4.20 TESCOM Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment