PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043847

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043847

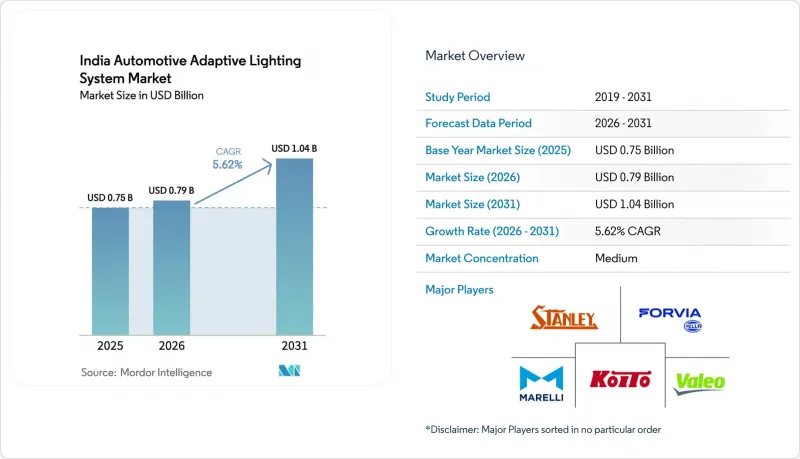

India Automotive Adaptive Lighting System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Indian automotive adaptive lighting system market size is expected to increase from USD 0.75 billion in 2025 to USD 0.79 billion in 2026, reaching USD 1.04 billion by 2031, growing at a CAGR of 5.62% over 2026-2031.

Recent rule-making, notably the draft AIS-199 photometric standard, is nudging original equipment manufacturers (OEMs) to treat adaptive front lighting as a compliance feature rather than a luxury add-on. Meanwhile, persistent unit-cost pressures confine full-feature systems to premium and upper-mid trims, even as LED die-cost declines slowly narrow the affordability gap. Suppliers are localizing critical sensors and camera modules to qualify for production-linked incentives (PLI) and thereby shorten lead times and mitigate currency exposure. Growth prospects remain tied to OEM electrification roadmaps because energy-efficient lighting helps maximize real-world range, an attribute buyers value as charging infrastructure scales. Competitive intensity is moderate, with five global tier-1 suppliers leveraging established OEM relationships and in-house software stacks to defend share.

India Automotive Adaptive Lighting System Market Trends and Insights

Rapid LED Cost Declines Enabling Mid-Segment Adoption

ED headlamp prices have come down sharply as die-size optimization improves yield, allowing OEMs to equip cars with adaptive functions without breaching price ceilings. Indigenous prototypes validated by the Automotive Research Association of India prove that locally engineered LED adaptive modules can meet AIS-127 benchmarks at competitive costs. Added volumes from mid-segment trims improve scale economics for sensor and actuator suppliers. As price sensitivity remains a defining feature of India's passenger-vehicle buyers, each incremental cost reduction unlocks a broader customer pool. Consequently, mid-segment electrified platforms increasingly specify automatic high-beam as standard.

AIS-199 Regulation Mandating AFS Photometric Standards (2024 Draft)

The 2024 draft standard consolidates illumination norms and references UN R-123, pushing carmakers to add glare-control logic, camera inputs, and adaptive optics to new platforms launched after 2026. Tier-1 suppliers that already certify products for Europe can repurpose validated designs, easing homologation. Because the rule applies across vehicle classes, compliance pressure trickles into commercial-vehicle segments by the decade's end. Export-oriented OEMs value this alignment because a single module can serve multiple regions, reducing engineering overhead. In the short term, AIS-199 effectively makes adaptive lighting mandatory for most new passenger models.

High Unit-Cost Limits Mass-Market Penetration

Full adaptive front-lighting assemblies cost well, forming a steep barrier for budget vehicles that dominate sales. Import dependence for sensor ASICs keeps bills of materials elevated, exposing OEMs to currency swings. Tier-1 suppliers are testing modular approaches that scale features with trim level, but fragmented volumes dilute cost savings. Until controller and camera prices drop through local fabrication, adaptive lighting remains a premium signifier rather than a mainstream safety norm.

Other drivers and restraints analyzed in the detailed report include:

- OEM Demand for ADAS Bundle-Features in Low-Budget Vehicles

- Growing EV Penetration Raising Demand for Energy-Efficient Lighting

- Semiconductor Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars dominated the Indian automotive adaptive lighting system market share in 2025, holding 55.67% and growing at an 8.47% CAGR, largely because private buyers value the safety features and styling cues that adaptive headlamps offer. Regulatory deadlines tied to AIS-199 spur OEMs to launch compliant passenger platforms first, leaving trucks and buses on legacy setups. Electrified passenger cars further reinforce uptake, as low-wattage LEDs help extend driving range.

Supplier roadmaps, therefore, concentrate engineering resources on car-specific beam-shaping algorithms and compact sensor clusters. Commercial vehicles trail because fleet operators scrutinize return on investment more tightly. Nonetheless, rising night-haul logistics and stricter insurance norms may pull adaptive high beam into select LCV fleets sooner than heavy trucks. Over time, economies of scale achieved in the passenger domain are expected to lower cost barriers, enabling a gradual spill-over into goods carriers and intercity buses.

Exterior lighting accounts for the majority of the Indian automotive adaptive lighting system market because headlamps sit at the intersection of safety regulations and consumer visibility needs. In 2025, the category accounted for 72.87% of total value and is set to post the fastest expansion, clocking a 9.77% CAGR through 2031 as adaptive front lighting and dynamic bending modules move down-segment. Interior applications such as ambient cabin lighting grow from a lower base, anchored mostly in premium vehicles where personalization outweighs strict safety calculus. Suppliers, therefore, direct most engineering budgets into forward-lighting optics, sensors, and beam-forming software.

The exterior focus also reflects higher per-unit revenue, as complete headlamp assemblies integrate actuators, ECUs, and LEDs. Interior modules remain important for brand differentiation, yet they lack regulatory tailwinds, limiting their penetration. Over time, synchronized cabin-exterior light sequences may spur incremental demand once centralized body-domain controllers become common. For the forecast period, however, exterior headlamps remain the clear volume and value driver within adaptive lighting portfolios.

The India Automotive Adaptive Lighting System Market Report is Segmented by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and More), Application (Exterior Lighting and Interior Lighting), Component Type (Controllers, Sensors/Cameras, and More), Technology (LED and More), Sales Channel (OEM and Aftermarket), and Functionality (Automatic High Beam and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Koito Manufacturing Co. Ltd.

- Valeo SA

- HELLA GmbH & Co KGaA (FORVIA)

- Magneti Marelli SpA

- Stanley Electric Co. Ltd.

- Varroc Engineering Ltd.

- Lumax Industries Ltd.

- Hyundai Mobis Co. Ltd.

- OSRAM Continental GmbH

- Texas Instruments Inc.

- Philips Automotive Lighting

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Uno Minda Ltd.

- Neolite ZKW Lighting Pvt. Ltd.

- LG Innotek Co. Ltd.

- ZKW Group GmbH

- SL Corporation

- Yazaki Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid LED Cost Declines Enabling Mid-Segment Adoption

- 4.2.2 AIS-199 Regulation Mandating AFS Photometric Standards (2024 Draft)

- 4.2.3 OEM Demand for ADAS Bundle-Features in Low-Budget Vehicles

- 4.2.4 Growing EV Penetration Raising Demand for Energy-Efficient Lighting

- 4.2.5 Tier-1 Localisation Incentives Under PLI Auto Components Scheme

- 4.2.6 Integration of Micro-LED/Pixel ADB With Embedded Sensors for V2X

- 4.3 Market Restraints

- 4.3.1 High Unit-Cost Limits Mass-Market Penetration

- 4.3.2 Semiconductor Supply-Chain Volatility

- 4.3.3 Fragmented Aftermarket and Warranty-Void Risk for Retrofits

- 4.3.4 Low Awareness of Glare-Free Benefits Among Fleet Owners

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

5 Market Size and Growth Forecasts (Value)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Light Commercial Vehicles (LCV)

- 5.1.3 Medium and Heavy Commercial Vehicles (MHCV)

- 5.2 By Application

- 5.2.1 Exterior Lighting

- 5.2.2 Interior Lighting

- 5.3 By Component Type

- 5.3.1 Controllers

- 5.3.2 Sensors / Cameras

- 5.3.3 Lamp Assemblies

- 5.3.4 Actuators

- 5.3.5 Others

- 5.4 By Technology

- 5.4.1 LED

- 5.4.2 Xenon / HID

- 5.4.3 Halogen

- 5.4.4 Laser Lighting

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Functionality

- 5.6.1 Automatic High Beam

- 5.6.2 Dynamic Bending Light

- 5.6.3 Cornering Lights

- 5.6.4 Adaptive Front Lighting

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Koito Manufacturing Co. Ltd.

- 6.4.2 Valeo SA

- 6.4.3 HELLA GmbH & Co KGaA (FORVIA)

- 6.4.4 Magneti Marelli SpA

- 6.4.5 Stanley Electric Co. Ltd.

- 6.4.6 Varroc Engineering Ltd.

- 6.4.7 Lumax Industries Ltd.

- 6.4.8 Hyundai Mobis Co. Ltd.

- 6.4.9 OSRAM Continental GmbH

- 6.4.10 Texas Instruments Inc.

- 6.4.11 Philips Automotive Lighting

- 6.4.12 Continental AG

- 6.4.13 Denso Corporation

- 6.4.14 Robert Bosch GmbH

- 6.4.15 Uno Minda Ltd.

- 6.4.16 Neolite ZKW Lighting Pvt. Ltd.

- 6.4.17 LG Innotek Co. Ltd.

- 6.4.18 ZKW Group GmbH

- 6.4.19 SL Corporation

- 6.4.20 Yazaki Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment