PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044138

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044138

Automotive Adaptive Lighting System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

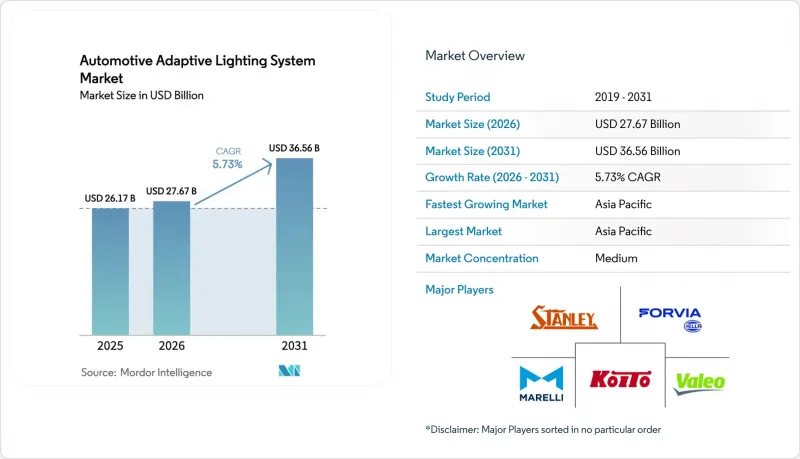

The automotive adaptive lighting market size is expected to increase from USD 26.17 billion in 2025 to USD 27.67 billion in 2026 and reach USD 36.56 billion by 2031, growing at a CAGR of 5.73% over 2026-2031.

Near-synchronous regulatory changes in Europe and North America are erasing the split-engineering costs that once slowed the rollout of advanced beams, enabling global platforms to scale faster. Automakers are pairing high-resolution headlamps with over-the-air functionality so that feature upgrades can be sold long after the initial vehicle purchase, supporting new recurring-revenue streams. Suppliers are racing to localize production of LED, laser, and micro-LED modules in Mexico, Poland, Turkiye, and Thailand to blunt currency risk and shipping delays. Software-defined lighting is moving from luxury branding to mainstream safety, with embedded sensors and AI algorithms constantly adjusting beam shape in real time based on traffic, terrain, and weather.

Global Automotive Adaptive Lighting System Market Trends and Insights

Stringent Global Lighting Regulations (ADB, ECE R123)

The United States legalized adaptive driving beams in 2022, aligning with Europe's ECE R123 and ending decades of suppression of the feature. This convergence lets automakers certify one hardware stack for multiple regions while fine-tuning beam patterns in software to satisfy each local photometric clause. China's GB 4599-2024 and companion rules came into force in 2025 with explicit approval for road-projection symbols, opening the door for lane guidance and pedestrian alerts. India validated a home-grown adaptive front lighting design that mirrors European optics, signaling an intent to mandate the feature on trucks by 2027. Together, these moves increase the addressable volume for suppliers, spur economies of scale, and accelerate investments in pixelated LEDs and laser-on-chip arrays.

Growing Demand for Advanced Safety Systems and ADAS

Automotive lighting now serves as an outward-facing sensor, not just illumination. Mercedes-Benz embedded adaptive beams into Active Brake Assist so the lamps actively highlight vulnerable road users when radar or camera flags a threat. Bosch pairs its Gen3 multi-purpose camera with headlamps on heavy trucks to shrink nighttime crash rates, a big win for fleet insurers. As OEMs deeply couple lighting with braking, steering, and perception ECUs, buyers are effectively locked into the tier-1 supplier that owns the entire stack. That establishment, and the prospect of subscription-based light upgrades delivered over-the-air, make adaptive lighting a priority line item on future product plans.

High Upfront Cost of Adaptive Modules vs. Fixed Lamps

Adaptive headlamps still cost 2-4 times as much as fixed LEDs, so OEMs usually bundle them with premium trim lines or paid software unlocks. On the 2026 BMW 3 Series, an adaptive ambient option adds nearly EUR 1,850 (~USD 2,135.15) to the sticker, limiting uptake in cost-sensitive markets. Dealership retrofits are scarce because extra harnesses void electrical warranties, cutting off a quick aftermarket path. Some suppliers now offer tiered packages that separate the expensive MEMS mirrors from basic auto-high-beam logic so that entry cars can at least comply with emerging regulations without big price jumps.

Other drivers and restraints analyzed in the detailed report include:

- Rising Premium and SUV Sales Lifting Feature-Take Rates

- Rapid LED Cost Reduction and Performance Gains

- Thermal Management Limits in High-Lumen LED/Laser Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger vehicles retained the largest 73.76% share of the automotive adaptive lighting market in 2025, helped by steady model-year refreshes that make matrix and pixel LEDs standard on mid-trim crossovers. Carmakers bundle the lamps with infotainment upgrades so buyers view them as part of a single comfort-and-safety package rather than a costly stand-alone option. Styling freedom in SUVs also gives designers more space for heatsinks and sensors, which further encourages rapid rollout. As volume rises, tier-1 suppliers gain scale economies that lower per-module costs and improve reliability through shared electronics platforms.

Medium and heavy commercial vehicles are expected to post the fastest 9.62% CAGR through 2031, driven by regulations that pair adaptive beams with collision-mitigation braking on long-haul rigs. Fleet operators accept the added expense because better nighttime visibility cuts accident downtime and insurance premiums. Lamp makers now offer modular housings that slide into existing apertures, letting trucks upgrade during scheduled maintenance without repainting surrounding panels. The resulting retrofit path accelerates adoption and provides suppliers with a second revenue cycle once factory warranties expire.

Exterior systems held a commanding 93.22% share in 2025, reflecting global laws that require glare-free beams and daytime running lamps on every new vehicle. Automakers migrate to single global lamp architectures that can be recalibrated in software, limiting tooling changes across regions. That strategy shortens development cycles and lets design teams focus on signature graphics that reinforce brand identity. Suppliers, in turn, compete on thermal management and optical efficiency rather than on basic compliance.

Interior adaptive lighting is rising fastest at an 8.27% CAGR, largely because electric and autonomous models use color and intensity shifts to substitute for engine sound as feedback to occupants. Cabin-centric systems integrate with voice assistants and biometric sensors so light scenes match the driver's mood or route conditions. Software updates can add new themes just like smartphone wallpapers, giving OEMs an ongoing revenue stream. As screens proliferate inside vehicles, ambient LEDs also cut eye strain by balancing overall luminance.

The Automotive Adaptive Lighting Market Report is Segmented by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and More), Application (Exterior Lighting and Interior Lighting), Component Type (Controllers and More), Technology (LED and More), Sales Channel (OEM and Aftermarket), Functionality (Automatic High Beam and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific captured 45.55% of the automotive adaptive lighting market revenue in 2025 and is growing at an 8.91% CAGR through 2031, driven by China's rapidly evolving rules that allow road-projection features. Domestic brands deploy adaptive beams as a status symbol in electric models competing head-to-head with German luxury imports. Japanese suppliers such as Koito and Stanley are expanding factories across ASEAN and Latin America to hedge against currency shifts while staying close to global vehicle platforms. India is shaping up as the next inflection market; an indigenous lighting standard mirroring Europe's optics clears the path for a mandate covering trucks from 2027 onward.

Europe maintains technology leadership and will advance at a measured 4.49% CAGR to 2031. ECE R123 sets a high bar for glare-free performance, nudging all new platforms toward matrix LEDs or lasers. German premium OEMs continue to trickle down high-resolution lamps into sub-EUR 40,000 (~USD 46,178.20) models, forcing volume brands to adopt similar tech or risk market share erosion. Production costs are being squeezed as suppliers shift assembly to Poland, Hungary, and Morocco, where wages are lower, but logistics still favor on-time delivery to EU plants.

North America is finally unlocking pent-up demand now that the NHTSA green-lit adaptive beams. Growth of 4.78% CAGR through 2031 may seem modest, yet the base is small after decades of prohibition. Over-the-air activations on existing vehicles, led by Tesla, prove that a latent install base already waits in the driveway. Suppliers are localizing micro-LED lines in Mexico to capitalize on the United States-Mexico-Canada Agreement's rules-of-origin credits, all while trimming shipping lead times. South America and the Middle East follow in tandem; revenue lifts come from SUV-heavy lineups where buyers accept feature premiums, but the lack of stringent lighting rules still limits full matrix rollouts.

- Hella GmbH & Co. KGaA

- Valeo SA

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- OSRAM Continental GmbH

- Marelli Automotive Lighting

- Lumileds Holding B.V.

- Hyundai Mobis Co., Ltd.

- Panasonic Automotive Systems

- ZKW Group

- J.W. Speaker Corporation

- Denso Corporation

- Varroc Lighting Systems

- Signify N.V. (Philips Automotive)

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Aptiv PLC

- Bosch Mobility

- Continental AG

- Lear Corporation

- Infineon Technologies AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global Lighting Regulations (ADB, ECE R123)

- 4.2.2 Growing Demand for Advanced Safety Systems and ADAS

- 4.2.3 Rising Premium and SUV Sales Lifting Feature-Take Rates

- 4.2.4 Rapid LED Cost Reduction and Performance Gains

- 4.2.5 OTA-Enabled Beam-Pattern Upgrades Post-Sale

- 4.2.6 V2X-Triggered Pedestrian-Communication Lighting

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Adaptive Modules Vs. Fixed Lamps

- 4.3.2 Thermal Management Limits in High-Lumen LED/Laser Units

- 4.3.3 ECU Cybersecurity Risks Via CAN-FD Gateways (Under-Radar)

- 4.3.4 GaN Substrate Supply Bottlenecks for Laser Diodes (Under-Radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Light Commercial Vehicles (LCV)

- 5.1.3 Medium and Heavy Commercial Vehicles (MHCV)

- 5.2 By Application

- 5.2.1 Exterior Lighting

- 5.2.2 Interior Lighting

- 5.3 By Component Type

- 5.3.1 Controllers

- 5.3.2 Sensors / Cameras

- 5.3.3 Lamp Assemblies

- 5.3.4 Actuators

- 5.3.5 Others

- 5.4 By Technology

- 5.4.1 LED

- 5.4.2 Xenon / HID

- 5.4.3 Halogen

- 5.4.4 Laser Lighting

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Functionality

- 5.6.1 Automatic High Beam

- 5.6.2 Dynamic Bending Light

- 5.6.3 Cornering Lights

- 5.6.4 Adaptive Front Lighting

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Turkey

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Hella GmbH & Co. KGaA

- 6.4.2 Valeo SA

- 6.4.3 Koito Manufacturing Co., Ltd.

- 6.4.4 Stanley Electric Co., Ltd.

- 6.4.5 OSRAM Continental GmbH

- 6.4.6 Marelli Automotive Lighting

- 6.4.7 Lumileds Holding B.V.

- 6.4.8 Hyundai Mobis Co., Ltd.

- 6.4.9 Panasonic Automotive Systems

- 6.4.10 ZKW Group

- 6.4.11 J.W. Speaker Corporation

- 6.4.12 Denso Corporation

- 6.4.13 Varroc Lighting Systems

- 6.4.14 Signify N.V. (Philips Automotive)

- 6.4.15 Renesas Electronics Corporation

- 6.4.16 Texas Instruments Incorporated

- 6.4.17 Aptiv PLC

- 6.4.18 Bosch Mobility

- 6.4.19 Continental AG

- 6.4.20 Lear Corporation

- 6.4.21 Infineon Technologies AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment