PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043884

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043884

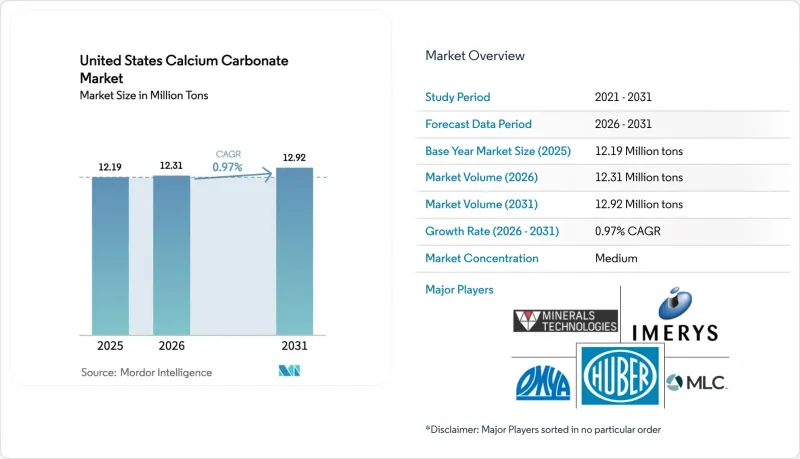

United States Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States Calcium Carbonate Market size is expected to grow from 12.19 million tons in 2025 to 12.31 million tons in 2026 and is forecast to reach 12.92 million tons by 2031 at 0.97% CAGR over 2026-2031.

Recent growth in volume terms has been modest, but there is a notable shift in value creation towards carbon-capture-derived precipitated calcium carbonate (PCC) and ultrafine specialty grades, both commanding premium pricing. Ground calcium carbonate (GCC) continues to dominate high-tonnage concrete and aggregate outlets. However, on-site PCC satellites at paper mills, along with emerging CCU facilities, are expanding the profit pool while cutting down transport emissions. Infrastructure projects, bolstered by the federal Infrastructure Investment and Jobs Act (IIJA), are tightening limestone supply chains, nudging converters towards higher-performance PCC grades. In the paints and plastics sector, formulators have increased calcium carbonate loadings to offset the structurally elevated costs of titanium dioxide and polymers, thus strengthening demand resilience. Moreover, heightened regulatory scrutiny on respirable crystalline silica is driving dust-suppression investments at quarries, giving a competitive edge to dust-free synthetic PCC.

United States Calcium Carbonate Market Trends and Insights

Rising Demand for Paints and Coatings

Formulators are increasing calcium carbonate extender ratios in paints and coatings to counteract persistently high titanium dioxide prices. This move comes as paints and coatings emerge as the fastest-growing outlet in the industry. A significant portion of the IIJA's allocation is directed to the Highway Trust Fund, boosting demand for protective coatings on bridges, overpasses, and airport facilities. Suppliers are ramping up sub-2 micron grinding capacity and investing in stearic-acid surface modification to achieve stringent rheology targets in high-performance architectural paints. Ultrafine and surface-treated grades enhance dispersion and reduce viscosity, allowing for greater filler loading without compromising film integrity. Notably, this substitution trend is pronounced in value-tier formulations, where increased extender levels lead to reduced raw-material costs.

Growth in the Paper and Packaging Industry

Thanks to decades of integrating PCC satellites, paper remains the dominant consumer, with on-site PCC constituting a substantial portion of a typical sheet. Domtar's Nekoosa Mill in Wisconsin, fed by a satellite launched in 2024, has successfully reduced carbon emissions annually and avoided significant trucking miles through its co-location strategy. While graphic paper has seen a decline, containerboard and e-commerce packaging are on the rise, bolstered by calcium carbonate coatings that enhance printability on corrugated boxes. Minerals Technologies, with numerous satellites globally, is channeling more capital into emerging Asia-Pacific, hinting at a maturing North American base. Yet, domestic mills are enhancing PCC particle-size control to compete for high-brightness specialty packaging orders, ensuring steady demand.

Competition from Talc, Kaolin, and Synthetic Fillers

Thanks to its superior heat resistance and dimensional stability, talc has become the preferred choice for polypropylene automotive parts. Kaolin, with its brightness advantage, is preferred in paper-coating niches. Meanwhile, precipitated silica and alumina fillers are gaining traction in high-gloss plastics and scratch-resistant coatings. Formulators are increasingly blending talc with calcium carbonate in new plastic recipes to enhance stiffness and impact properties. In the coatings sector, while synthetic silica matting agents challenge calcium carbonate in premium wood finishes, cost considerations limit their widespread adoption. Regional supply chains play a pivotal role: talc is mainly sourced from Montana and Texas, while calcium carbonate's nationwide availability offers a freight advantage in numerous high-volume applications.

Other drivers and restraints analyzed in the detailed report include:

- Plastics Industry Adoption of CaCO3 Fillers

- United States Infrastructure Spending (IIJA) Boosting GCC Demand

- Stricter United States Quarrying and Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Ground Calcium Carbonate (GCC) dominated the market, accounting for 75.69% of the total volume. For example, Michigan's Port Calcite ships millions of tons annually via lake freighters, achieving low unit costs for clients in the Midwest cement and aggregate sectors. While Precipitated Calcium Carbonate (PCC) holds a smaller market share, its output is on the rise, growing at a 2.26% CAGR through the forecast period of 2026-2031. This growth is fueled by the emergence of satellite plants near paper mills and various CCU projects. Even though starting from a smaller base, the U.S. market for PCC is on a steady upward trajectory. CarbonFree's Gary Works project is not only capturing CO2 but also marketing it as premium food-grade PCC. This strategy aligns with 45Q incentives and highlights CCU's transformative potential. Fortera and Graymont's ReAct partnership is introducing vaterite PCC, which can serve as a partial substitute for cement clinker, addressing the increasing demand for green concrete. However, the supply chain faces hurdles: the processes of capturing, purifying, and liquefying CO2 elevate capital expenditures. Fortunately, federal grants and state cap-and-trade credits are helping to level the playing field with mined GCC.

Commercial-scale PCC, known for its finer particle size, elevated purity, and customizable morphology, commands a premium over commodity GCC. This makes it highly desirable in sectors such as food, pharmaceuticals, and high-gloss coatings. Meanwhile, upgraded grinding circuits producing ultrafine GCC are enhancing GCC's average unit value, especially in matte architectural coatings. In the realm of digital-print papers and low-VOC water-based paints, hybrid filler systems are emerging. Here, ultrafine GCC provides volume, while PCC contributes opacity or brightness. While GCC is likely to retain its volume leadership, the distinct advantages of PCC and the benefits from CCU are set to bridge the historical price-to-performance gap in the U.S. calcium carbonate market.

The United States Calcium Carbonate Market Report is Segmented by Type (Ground Calcium Carbonate and Precipitated Calcium Carbonate), and End-User Industry (Paper, Plastic, Adhesive and Sealant, Paints and Coatings, and Other End-User Industries). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Blue Mountain Minerals

- Carmeuse

- Cerne Calcium Company

- Chememan Public Company Limited.

- CIMBAR RESOURCES, INC.

- Columbia River Carbonates

- GLC Minerals LLC

- Graymont

- ILC Resources

- Imerys

- J.M. Huber Corporation

- Lhoist

- Minerals Technologies Inc.

- Mississippi Lime Company

- Newpark Resources Inc.

- Omya AG

- Sibelco

- The Cary Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Rising demand from paints and coatings

- 4.1.2 Growth in paper and packaging industry

- 4.1.3 Plastics industry adoption of CaCO3 fillers

- 4.1.4 United States infrastructure spending (IIJA) boosting GCC demand

- 4.1.5 On-site PCC produced via carbon-capture utilization

- 4.2 Market Restraints

- 4.2.1 Health hazards from respirable CaCO3 dust

- 4.2.2 Competition from talc, kaolin and synthetic fillers

- 4.2.3 Stricter United States quarrying and emission regulations

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

- 4.5 Mine Locations

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Ground Calcium Carbonate

- 5.1.2 Precipitated Calcium Carbonate

- 5.2 By End-user Industry

- 5.2.1 Paper

- 5.2.2 Plastic

- 5.2.3 Adhesive and Sealant

- 5.2.4 Paints and Coatings

- 5.2.5 Other End-User Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Blue Mountain Minerals

- 6.4.2 Carmeuse

- 6.4.3 Cerne Calcium Company

- 6.4.4 Chememan Public Company Limited.

- 6.4.5 CIMBAR RESOURCES, INC.

- 6.4.6 Columbia River Carbonates

- 6.4.7 GLC Minerals LLC

- 6.4.8 Graymont

- 6.4.9 ILC Resources

- 6.4.10 Imerys

- 6.4.11 J.M. Huber Corporation

- 6.4.12 Lhoist

- 6.4.13 Minerals Technologies Inc.

- 6.4.14 Mississippi Lime Company

- 6.4.15 Newpark Resources Inc.

- 6.4.16 Omya AG

- 6.4.17 Sibelco

- 6.4.18 The Cary Company

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment