PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043887

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043887

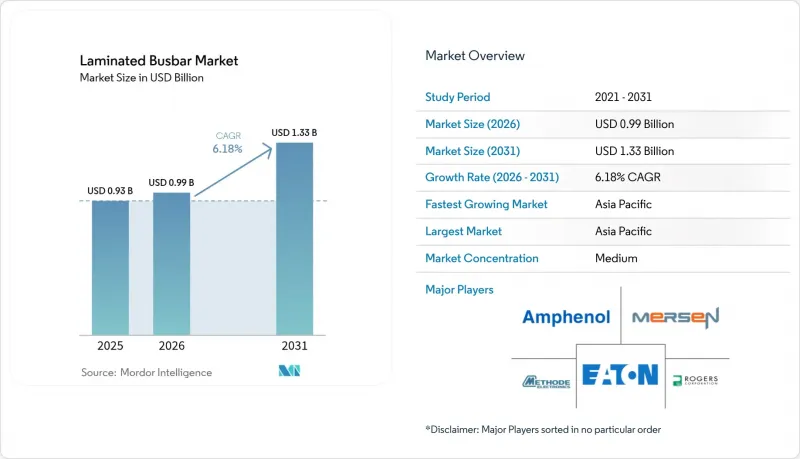

Laminated Busbar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Laminated Busbar market size in 2026 is estimated at USD 987.47 million, growing from 2025 value of USD 0.93 billion with 2031 projections showing USD 1.33 billion, growing at 6.18% CAGR over 2026-2031.

Momentum comes from electrified transportation, renewable energy inverters, and high-density data center power backplanes, all of which demand compact power distribution assemblies with low inductance and high thermal efficiency. Copper remains the baseline conductor for performance-critical systems, while aluminum and hybrid metal combinations build traction in weight-sensitive applications. Supply security for raw materials and continuing advances in wide-bandgap power modules underpin new design requirements that favor laminated architectures over conventional bar or cable harnesses. Pricing pressure from volatile copper costs is partially offset by manufacturing productivity gains and the growing willingness of end users to pay a premium for enhanced safety and space savings.

Global Laminated Busbar Market Trends and Insights

EV & HEV Proliferation Drives Compact Power Solutions

Automakers are accelerating the adoption of laminated busbars to reduce battery-pack footprints and improve thermal performance. Tesla's structural battery and BYD's blade format demonstrate how laminated conductors reduce assembly complexity by 40% while maintaining high current density.[1] Aluminum-copper hybrids produced via cold-cladding now combine weight savings with conductivity, and ultrasonic welding, along with silver coatings, resolve aluminum oxidation hurdles. Vehicle platforms shifting to 400 V-800 V systems require flexible busbar geometries that accommodate changing cell chemistries without compromising safety margins. The cascading effect is a broadened supply base, with materials specialists and tier-one integrators vying for long-term supply awards, boosting the laminated busbar market.

Renewable-Energy Inverter Roll-outs Expand Grid Integration

Solar and wind OEMs specify laminated busbars for low-inductance, high-current inverter stages. SiC and GaN switches now operate well past 50 kHz, and laminated geometries cut stray inductance by up to 90%, improving conversion efficiency and enabling bidirectional power flow in storage-combined assets.[2] Standardized interfaces simplify the swapping of energy-storage modules, while embedded sensors enable predictive maintenance that prevents inverter downtime in utility-scale parks, further expanding the laminated busbar market.

Volatile Copper & Aluminum Prices

Copper reached USD 6.20 per pound in July 2024, prompting component suppliers to increase their price lists by up to 45%, as raw materials account for up to 70% of the cost. Multi-year inverter or grid contracts limit pass-through ability, eroding margins. Aluminum swings add another layer of uncertainty just as hybrids gain share. Some OEMs hedge their bets with long-term supply agreements or explore copper-clad aluminum conductors that reduce exposure without compromising conductivity.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center Power-Backplane Demand Spike

- Industrial Electrification & Automation Surge

- Heat-Dissipation & Delamination Beyond 1 kV

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Copper captured 71.05% of the laminated busbars market share in 2025, driven by its unmatched conductivity and mature processing routes. This dominance is anchored by high-power inverters and battery packs that cannot compromise on resistive losses or heat rise. However, aluminum sections are expected to accelerate at an 7.85% CAGR as vehicle OEMs trade density for weight savings and achieve a 40% reduction in raw-material costs. Cold-clad bimetal strip from Samuel Taylor and similar suppliers enables jointless aluminum-copper interfaces that maintain current paths and mechanical integrity. As a result, specification engineers increasingly approve hybrids for 800 V traction inverters and charging modules, reshaping bill-of-materials norms.

Aluminum adoption forces insulation labs to rethink dielectric thickness for lower melting-point conductors, while silver-flash or nickel-plate coatings extend mating-surface life. Weight-optimized rail designs trim pack mass in long-range EVs, unlocking extra kilowatt-hours or payload. Suppliers targeting the laminated busbars industry invest in ultrasonic welding lines and automated quality control to guarantee consistent clad integrity across large production batches.

Epoxy powder coating accounted for 37.45% of the revenue in 2025 by combining robust mechanical protection with low per-part costs, making it the default choice for switchgear and factory automation cabinets. Yet polyester and polyimide films are gaining traction at a 7.55% CAGR because thinner stacks translate to lower inductance and better thermal pathways. Specialty films withstand the rapid temperature swings commonly seen in SiC traction modules, supporting junction temperatures exceeding 175°C without cracking.

Film laminates enable busbars under 2 mm thick that snake through cramped battery-pack cavities. Heat-resistant fiber reinforcements and ceramic fillers raise breakdown voltage while maintaining flexibility. Environmental, health, and safety teams also note that newer solvent-free film adhesives lower volatile organic compound emissions in production, advancing corporate sustainability targets without sacrificing product lifespan.

The Laminated Busbar Market Report is Segmented by Conducting Material (Copper, Aluminum, and Hybrid), Insulation Material (Epoxy Powder Coating, Polyester, and More), Busbar Configuration (Multi-Layer, High-Layer, and Flex/Thin Busbars), Voltage Rating (Low Voltage, and More), Application (Renewable Energy, and More), End-User (Power Utilities, Transportation OEMs, and More), and Geography (North America, Asia-Pacific, and More).

Geography Analysis

The Asia-Pacific region dominated the laminated busbars market in 2025, with a 40.95% share, and is expected to expand at a 7.2% CAGR as vertically integrated supply chains in China, Japan, and South Korea compress lead times and reduce costs. The laminated busbars market size in the region benefits from large-volume EV production lines that secure multiyear busbar contracts tied to battery-pack ramps. India accelerates renewable-energy inverter deployment, adding further pull for regional lamination capacity.

North America ranked second, driven by hyperscale data-center retrofits and ambitious automotive electrification timelines. Tesla's structural battery programs alone create recurring demand spikes for custom conductor layouts, while 48V rack conversions in cloud campuses secure steady orders for pre-engineered backplane kits. Federal incentives to localize critical-component manufacturing add momentum to US-based lamination investments.

Europe relies on stringent environmental directives and industry automation to maintain steady adoption. Wind-energy OEMs rely on busbars that pair with SiC power modules in offshore converter stations, whereas German machine-tool makers retrofit factory panels with laminated boards to shrink cabinet footprints. Regional suppliers differentiate through low-carbon copper sourcing and cradle-to-grave recycling programs, resonating with EU sustainability goals.

- Eaton Corporation plc

- Rogers Corporation

- Mersen SA

- Methode Electronics Inc.

- Amphenol Corporation

- Molex LLC

- Sun.King Power Electronics Group Ltd

- Zhuzhou CRRC Times Electric Co., Ltd

- Storm Power Components

- Segue Electronics Inc.

- EMS Industrial & Service Company

- Ryoden Kasei Co., Ltd

- Shanghai Eagtop Electronic Technology Co., Ltd

- Suzhou West Deane Machinery Inc.

- Raychem RPG Private Limited

- Zhejiang RHI Electric Co., Ltd

- Electronic Systems Packaging LLC

- Idealec SAS

- Advanced Energy Industries, Inc.

- Delta Electronics, Inc.

- Siemens AG

- ABB Ltd

- Schneider Electric SE

- Littelfuse Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV & HEV proliferation

- 4.2.2 Renewable energy inverter roll-outs

- 4.2.3 Data-center power-backplane demand spike

- 4.2.4 Industrial electrification & automation surge

- 4.2.5 SiC/GaN-based high-voltage modules adoption

- 4.2.6 Modular eVTOL battery pack architectures

- 4.3 Market Restraints

- 4.3.1 Volatile copper & aluminum prices

- 4.3.2 Low-cost conventional busbars as substitutes

- 4.3.3 Heat-dissipation & delamination beyond 1 kV

- 4.3.4 Aerospace qualification/documentation burden

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Conducting Material

- 5.1.1 Copper

- 5.1.2 Aluminum

- 5.1.3 Hybrid (Cu-Al composite)

- 5.2 By Insulation Material

- 5.2.1 Epoxy Powder Coating

- 5.2.2 Polyvinyl Fluoride Film

- 5.2.3 Polyester

- 5.2.4 Heat-Resistant Fiber

- 5.2.5 Polyimide/Kapton

- 5.2.6 Others

- 5.3 By Busbar Configuration

- 5.3.1 Multi-layer (3 to 5 layers)

- 5.3.2 High-layer (More Than 5 layers)

- 5.3.3 Flex/Thin busbars

- 5.4 By Voltage Rating

- 5.4.1 Low Voltage (Below 1 kV)

- 5.4.2 Medium Voltage (1 to 35 kV)

- 5.4.3 High Voltage (Above 35 kV)

- 5.5 By Application

- 5.5.1 Electric and Hybrid Vehicles

- 5.5.2 Renewable Energy (Solar, Wind, ESS)

- 5.5.3 Data Centers and Cloud Infrastructure

- 5.5.4 Industrial Drives and Machinery

- 5.5.5 Rail and Mass Transit

- 5.5.6 Aerospace and eVTOL

- 5.6 By End-User

- 5.6.1 Power Utilities

- 5.6.2 Industrial OEMs

- 5.6.3 Transportation OEMs

- 5.6.4 Residential and Commercial Construction

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germnay

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 ASEAN Countries

- 5.7.3.7 Rest of Asia Pacific

- 5.7.4 South America

- 5.7.4.1 Argentina

- 5.7.4.2 Brazil

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Eaton Corporation plc

- 6.4.2 Rogers Corporation

- 6.4.3 Mersen SA

- 6.4.4 Methode Electronics Inc.

- 6.4.5 Amphenol Corporation

- 6.4.6 Molex LLC

- 6.4.7 Sun.King Power Electronics Group Ltd

- 6.4.8 Zhuzhou CRRC Times Electric Co., Ltd

- 6.4.9 Storm Power Components

- 6.4.10 Segue Electronics Inc.

- 6.4.11 EMS Industrial & Service Company

- 6.4.12 Ryoden Kasei Co., Ltd

- 6.4.13 Shanghai Eagtop Electronic Technology Co., Ltd

- 6.4.14 Suzhou West Deane Machinery Inc.

- 6.4.15 Raychem RPG Private Limited

- 6.4.16 Zhejiang RHI Electric Co., Ltd

- 6.4.17 Electronic Systems Packaging LLC

- 6.4.18 Idealec SAS

- 6.4.19 Advanced Energy Industries, Inc.

- 6.4.20 Delta Electronics, Inc.

- 6.4.21 Siemens AG

- 6.4.22 ABB Ltd

- 6.4.23 Schneider Electric SE

- 6.4.24 Littelfuse Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment