PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043888

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043888

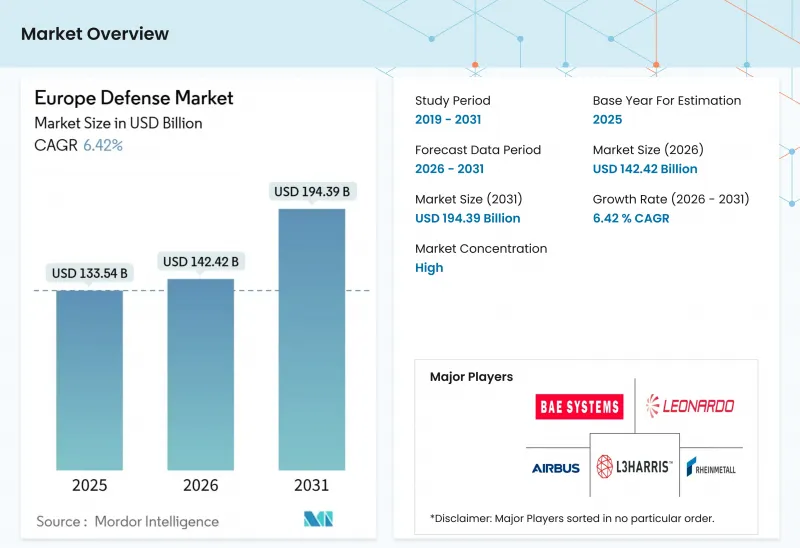

Europe Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe defense market size is expected to grow from USD 133.54 billion in 2025 to USD 142.42 billion in 2026 and is forecasted to reach USD 194.39 billion by 2031 at a 6.42% CAGR over 2026-2031.

Expanding NATO commitments to higher, sustained defense outlays are pushing multi-year procurement pipelines and capacity investments across land, air, maritime, and space programs, reinforcing structural growth in the Europe defense market. Russia's 2024 defense budget reached USD 149 billion, equal to 7.1% of GDP, which sharpened focus on munitions production, integrated air defense, and naval deterrence in frontline and near-frontline countries. Governments are elevating resilience through common procurement frameworks and local industrialization rules that favor European content and interoperable systems across alliances. The European defense market is also seeing a shift toward network-centric concepts, where software and data integration drive battlefield advantage and create opportunities for new entrants to complement legacy primes.

Europe Defense Market Trends and Insights

NATO Defense Spending Threshold Accelerates National Budget Alignments

Allied governments are anchoring defense allocations to GDP formulas that reduce annual volatility and enable industry to plan multi-year capacity expansions in the Europe defense market. NATO members signaled a path to higher, sustained outlays beyond the longstanding 2% guidance, and all Allies continued to prioritize readiness and stockpile rebuilding in 2026 after a notable step-up in 2025. The UK has committed to reaching 2.5% of GDP by 2027, with an ambition to reach 3% in the next Parliament, which tightens the demand outlook for air power, land systems, and maritime protection. Sweden met the 2.0% benchmark in its first year of NATO membership, reinforcing the broader European pivot to territorial defense and deterrence. Germany's new Act on Accelerated Planning and Procurement, effective January 15, 2026, is designed to streamline acquisitions and give preference to interoperable, off-the-shelf European solutions that support scale efficiencies in the Europe defense market. As these measures take hold, budget automaticity is creating predictability for contractors to expand ammunition, air-defense, and C4ISR capacity without overexposure to stop-start cycles in the Europe defense market.

EU Defense Fund Incentives Boost Cross-Border R&D and Capability Programs

EU instruments are bringing together Member States and industry into larger, cross-border teams that share risk across research, development, and early procurement in the Europe defense market. The European Defence Industry Programme embeds a "Buy European" presumption that caps non-EU content at 35% on common procurements and permits up to 25% EU co-funding when nations aggregate demand, which lifts participation by mid-tier suppliers and dual-use innovators. EDF and EDIP create incentives for at least three entities from three countries to collaborate, accelerating technology transfer between primes and software-centric suppliers across sensors, AI, and counter-UAS. The Commission's Defence Readiness Roadmap, published in October 2025, outlined a pathway to scale defense and space within the post-2027 budget framework, signaling durable institutional support for the Europe defense market. As these mechanisms mature, common standards and pooled logistics are likely to compress unit costs and reduce fragmentation in key product lines. This architecture encourages suppliers to invest in modular designs and digital engineering that meet both national requirements and joint European specifications.

Budget Constraints Due to Competing Energy Transition Priorities

Member States are balancing a multi-year rearmament push with the financing demands of the energy transition, keeping budget trade-offs in focus in the Europe defense market. REPowerEU requires significant additional public and private investment through 2027, and compliance costs for carbon-intensive inputs continue to influence production economics for heavy industry. Italy's 2026 defense allocation stands at EUR 31.3 billion (USD 36.83 billion), around 1.2% of GDP, according to European Commission projections, underscoring fiscal constraints in Southern Europe. EU fiscal rules have been adapted to improve flexibility, but national deficit procedures still limit the speed at which some countries can lift spending to alliance targets. Where governments have created special funds or procurement fast-tracks, execution remains the key variable that determines industrial throughput in the Europe defense market. Over the medium term, the pacing challenge is to lock in stable defense cash flows without crowding out energy transition priorities in already tight budgets.

Other drivers and restraints analyzed in the detailed report include:

- Russia-Ukraine Conflict Intensifies Defense Preparedness and Threat Awareness

- Adoption of Multi-Domain Operations Reshapes European Force Planning

- Supply Chain Disruptions in Energetic Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Army held 42.67% of the Europe defense market share in 2025, reflecting the renewed emphasis on territorial defense, integrated air and missile defense, and mechanized formations. This share aligns with the shift toward higher readiness levels and deeper munitions and spares stocks across European land forces. The Navy is projected to expand the fastest at 7.67% CAGR through 2031, supported by Baltic and North Atlantic initiatives that prioritize anti-submarine warfare, surface combatants, and maritime domain awareness. Cross-domain integration is also lifting demand for maritime ISR and command-and-control nodes that connect naval assets with joint fires networks in the Europe defense market. Kongsberg's December 2025 agreements to provide combat-system elements and navigation systems for German and Norwegian 212CD submarines illustrate momentum in undersea capabilities and industry partnerships.

Across air forces, upgrades continue on sensors, electronic warfare, and air policing, while planning for next-generation combat air emphasizes sovereign data pipelines and joint effectors. Exercises such as Dynamic Front 25 validate coalition fire coordination and logistics at scale, reinforcing procurement of interoperable radios, data links, and software-defined capabilities in the Europe defense market. Naval modernization goals are drawing attention to shipyards able to deliver on time with proven systems integration, a factor that is consolidating orders with vendors demonstrating reliable execution. Interoperability within NATO is driving purchases of munitions and communications that meet standardized standards, reducing sustainment risk and accelerating fielding in the Europe defense market. The Army's enduring share and the Navy's growth profile underscore a portfolio rebalancing that supports deterrence across land corridors and maritime chokepoints.

Vehicles captured 48.85% of the European defense market in 2025, underpinned by main battle tank recapitalization, infantry fighting vehicle procurement, and self-propelled artillery programs. Orders for layered air defense and integrated firepower continue to complement ground combat systems, with suppliers integrating sensors and effectors into digital command networks across the European defense market. Unmanned systems are forecast to grow the fastest, at a 7.12% CAGR, as drone swarms, counter-UAS, and loitering effectors reshape the tactical edge and compress the targeting cycle. Germany's rollout of AI-enabled reconnaissance processing for brigade-level formations highlights how autonomy and software lift operational tempo and survivability, including against massed aerial threats. Orders for mobile air-defense cannons such as Skyranger also reflect the urgency of kinetic counter-UAS solutions that can be fielded fast and sustained at scale in the Europe defense market.

Munitions and missile production are accelerating with multi-year funding visibility and factory expansions, reinforcing strategic depth for deterrence and allied support. MBDA's intake surged in 2024 and 2025 versus pre-2021 levels, signaling multi-layer air-defense demand and long-range precision fires momentum in the Europe defense market. Software-centric C4ISR, EW, and training solutions are also gaining share as doctrine moves toward multi-domain operations where data fusion and targeting automation define advantage. The United Kingdom's force-mix concept, which balances crewed and uncrewed systems, prioritizes reusable platforms and consumable effectors, a shift that favors modularity and high-volume production. Taken together, the mix of vehicles, missiles, and autonomy underscores a cycle favoring iterative upgrades, rapid prototyping, and plug-and-play architectures in the Europe defense market.

The Europe Defense Market Report is Segmented by Armed Forces (Air Force, Army, and Navy), Type (Personnel Training and Protection, Vehicles, Weapons and Ammunition, Unmanned Systems, and More), Domain (Land, Air, Naval, and More), Procurement Nature (Indigenous Production and Foreign Procurement), and Geography (United Kingdom, Germany, France, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Airbus SE

- BAE Systems plc

- Leonardo S.p.A.

- Thales Group

- Rheinmetall AG

- Saab AB

- KNDS N.V.

- Dassault Aviation S.A.

- MBDA

- Rolls-Royce Holdings plc

- HENSOLDT AG

- Diehl Stiftung & Co. KG (Diehl Group)

- Kongsberg Gruppen ASA

- Elbit Systems Ltd.

- L3Harris Technologies, Inc.

- RTX Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- General Dynamics Corporation

- United Aircraft Corporation (UAC)

- Ukroboronprom

- thyssenkrupp AG

- General Atomics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NATO defense spending threshold accelerates national budget alignments

- 4.2.2 EU defense fund incentives boost cross-border R&D and capability programs

- 4.2.3 Russia-Ukraine conflict intensifies defense preparedness and threat awareness

- 4.2.4 Adoption of multi-domain operations reshapes European force planning

- 4.2.5 Rapid prototyping pathways (EDIDP, ASAP)

- 4.2.6 Sovereign missile defense development gains traction through initiatives like Sky Shield

- 4.3 Market Restraints

- 4.3.1 Budget constraints due to competing energy transition priorities

- 4.3.2 Supply chain disruptions in energetic materials

- 4.3.3 Inconsistent export licensing policies across EU member states

- 4.3.4 Limited availability of skilled labor for systems integration

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Armed Forces

- 5.1.1 Air Force

- 5.1.2 Army

- 5.1.3 Navy

- 5.2 By Type

- 5.2.1 Personnel Training and Protection

- 5.2.2 C4ISR and Electronic Warfare

- 5.2.3 Vehicles

- 5.2.4 Weapons and Ammunition

- 5.2.5 Unmanned Systems

- 5.2.6 Space and Cyber Systems

- 5.3 By Domain

- 5.3.1 Land

- 5.3.2 Air

- 5.3.3 Naval

- 5.3.4 Space

- 5.3.5 Cyber and Electromagnetic Spectrum

- 5.4 By Procurement Nature

- 5.4.1 Indigenous Production

- 5.4.2 Foreign Procurement

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Sweden

- 5.5.7 Poland

- 5.5.8 Netherlands

- 5.5.9 Norway

- 5.5.10 Russia

- 5.5.11 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 BAE Systems plc

- 6.4.3 Leonardo S.p.A.

- 6.4.4 Thales Group

- 6.4.5 Rheinmetall AG

- 6.4.6 Saab AB

- 6.4.7 KNDS N.V.

- 6.4.8 Dassault Aviation S.A.

- 6.4.9 MBDA

- 6.4.10 Rolls-Royce Holdings plc

- 6.4.11 HENSOLDT AG

- 6.4.12 Diehl Stiftung & Co. KG (Diehl Group)

- 6.4.13 Kongsberg Gruppen ASA

- 6.4.14 Elbit Systems Ltd.

- 6.4.15 L3Harris Technologies, Inc.

- 6.4.16 RTX Corporation

- 6.4.17 Lockheed Martin Corporation

- 6.4.18 Northrop Grumman Corporation

- 6.4.19 General Dynamics Corporation

- 6.4.20 United Aircraft Corporation (UAC)

- 6.4.21 Ukroboronprom

- 6.4.22 thyssenkrupp AG

- 6.4.23 General Atomics

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment