PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043891

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043891

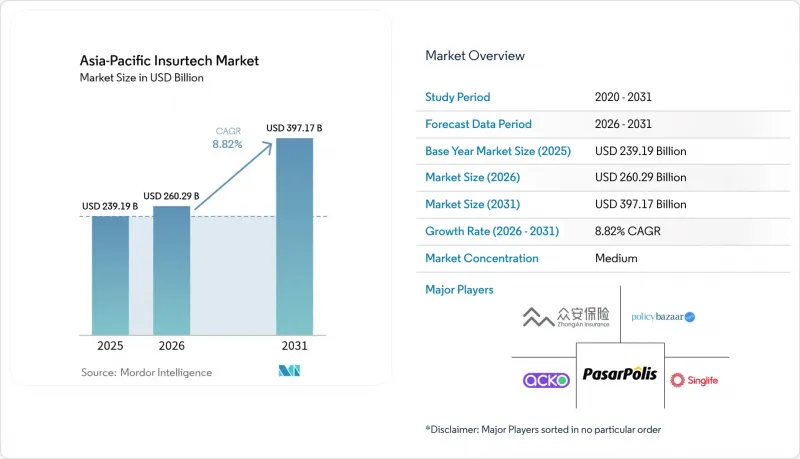

Asia-Pacific Insurtech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Asia-Pacific Insurtech Market size is expected to grow from USD 239.19 billion in 2025 to USD 260.29 billion in 2026 and is forecast to reach USD 397.17 billion by 2031 at 8.82% CAGR over 2026-2031.

This resilient growth is rooted in smartphone-first distribution economics, regulatory sandbox acceleration, and the use of advanced analytics that enhance underwriting precision and claims automation. Embedded-insurance ecosystems now secure previously unreachable retail and SME customers, while cross-border regulatory harmonization inside ASEAN lowers entry barriers for multi-market platforms. Falling mobile-acquisition costs, a surge in specialty-risk awareness, and fresh capital flowing into parametric solutions further reinforce the upside for the Asia-Pacific insurtech market. Competitive dynamics remain fluid as AI-enabled underwriting erodes traditional loss-ratio advantages and encourages incumbents to form strategic alliances with fintechs.

Asia-Pacific Insurtech Market Trends and Insights

Rise of Embedded-Insurance Ecosystems

Embedded platforms place cover inside everyday purchase journeys, letting users buy protection without leaving the host app. This seamless flow removes agent friction and cuts acquisition costs by up to 40%, a saving that improves unit economics at scale. Ant Group's partnership with Alibaba shows the model's reach as premiums emerge from e-commerce, travel, and wallet transactions. Singapore's clear API guidelines allow non-insurers to distribute products under existing fintech licenses, keeping compliance overhead low. Higher engagement across multiple touchpoints feeds behavioral data back to underwriters, raising pricing accuracy and lowering loss ratios. These network effects reinforce adoption, positioning embedded insurance as a structural growth engine for the Asia-Pacific insurtech market.

Sharp Increase in Asia-Pacific Cyber-Risk Exposure

Digital transformation widens attack surfaces across health care, finance, and manufacturing, driving urgent demand for cyber cover. Singapore's 2024 AI Model Risk Management rules compel financial firms to prove robust controls, pushing buyers toward policies that document compliance. Insurtechs respond with parametric cyber products that pay automatically on metrics like downtime minutes, avoiding long investigations. Real-time pricing engines ingest threat-intel feeds and vulnerability scans, letting underwriters match premiums to each client's security posture. Cloud concentration risk grows as hyperscale providers expand regional centers, adding urgency for bespoke policies. Together, these forces raise cyber insurance penetration yet leave ample protection gaps for agile entrants.

Persistent Data-Privacy Fragmentation by Jurisdiction

APAC regulators each impose unique consent, storage, and transfer rules, forcing insurtechs to build separate data stacks for every market. Compliance teams must master Singapore's PDPA, India's Digital Personal Data Protection Act, and China's Cybersecurity Law, driving costs 25-35% higher than single-market peers. Fragmentation slows embedded-insurance rollouts because real-time data sharing with partners may breach residency rules. Reinsurers struggle to pool risks across borders when one jurisdiction's strictest requirement governs all shared data. Ongoing changes add further uncertainty as governments tighten or relax clauses with short notice. The resulting complexity diverts capital from product development and constrains the Asia-Pacific insurtech market's regional scaling.

Other drivers and restraints analyzed in the detailed report include:

- Smartphone-First Customer Acquisition Costs Falling

- Sandbox-Style Regulatory Fast-Tracks Across Asia-Pacific

- Thin Actuarial Loss Histories for New-Risk Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Property & Casualty retained 40.62% of 2025 premiums, giving it the largest slice of the Asia-Pacific insurtech market share. Stable claim patterns, long-standing regulatory familiarity, and highly digitized motor and household lines underpin this dominance, yet growth momentum is slowing as pricing competition intensifies and catastrophe losses pressure underwriting margins. Specialty Lines, in contrast, are expanding at a 9.86% CAGR, lifting their contribution to the Asia-Pacific insurtech market size year after year as cyber, pet, and travel covers gain recognition across corporate and consumer segments. Parametric cyclone pilots in the Philippines and Fiji illustrate how rapid-payout products can fill long-standing protection gaps and attract multilateral donor funding, giving specialty carriers both social relevance and profitable scale.

Cyber insurance remains the specialty headline as ransomware costs rise, yet actuarial thinness keeps reinsurance attachment points high, tempering near-term penetration. Insurtechs mitigate data scarcity by fusing threat-intelligence feeds, endpoint telemetry, and cloud-service uptime metrics into dynamic underwriting models that reward strong security hygiene with lower premiums. Pet insurance follows a similar data-rich trajectory as tele-vet usage supplies continuous behavioral information that sharpens pricing. Marine and inland transit lines leverage satellite cargo tracking to trigger parametric payouts for voyage disruptions, cutting claims friction for exporters. Together, these innovations lift average premium growth well above the market baseline, positioning Specialty Lines as the primary long-run value engine of the Asia-Pacific insurtech market.

The Asia-Pacific Insurtech Market Report is Segmented by Product Line (Life Insurance, Health Insurance, Property & Casualty, Specialty Lines), Distribution Channel (Direct-To-Consumer Digital, Aggregators/Marketplaces, and More), End User (Retail/Individual, SME/Commercial, and More), and Geography (India, China, Japan, Australia, South Korea, South-East Asia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ZhongAn

- Policybazaar

- Acko

- PasarPolis

- Singlife

- OneDegree

- CXA Group

- Waterdrop

- Koala

- CoverGo

- Bolttech

- Shift Technology

- CarDekho (Insurance arm)

- Turtlemint

- Tokio Marine & Nichido (Digital Lab)

- Ping An OneConnect

- Munich Re Digital Partners

- FWD Group

- Sompo Himaraya

- NTUC Income (Income Insurance)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of embedded-insurance ecosystems

- 4.2.2 Sharp increase in Asia-Pacific cyber-risk exposure

- 4.2.3 Smartphone-first customer acquisition costs falling

- 4.2.4 Sandbox-style regulatory fast-tracks across Asia-Pacific

- 4.2.5 Advanced analytics/Gen-AI driving underwriting accuracy

- 4.2.6 Climate-linked parametric products gaining traction

- 4.3 Market Restraints

- 4.3.1 Persistent data-privacy fragmentation by jurisdiction

- 4.3.2 Thin actuarial loss histories for new-risk products

- 4.3.3 Profit-pool concentration in incumbents limits exits

- 4.3.4 Rising reinsurance pricing & capacity constraints

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Product Line (Insurance Type)

- 5.1.1 Life Insurance

- 5.1.2 Health Insurance

- 5.1.3 Property & Casualty (Motor, Home, Commercial, Liability)

- 5.1.4 Specialty Lines (Cyber, Pet, Marine, Travel)

- 5.2 By Distribution Channel

- 5.2.1 Direct-to-Consumer (Digital)

- 5.2.2 Aggregators / Marketplaces

- 5.2.3 Digital Brokers / MGAs

- 5.2.4 Embedded Insurance Platforms

- 5.2.5 Traditional Agents / Brokers (digitally enabled)

- 5.2.6 Bancassurance (digitally enabled)

- 5.2.7 Other Channels

- 5.3 By End User

- 5.3.1 Retail / Individual

- 5.3.2 SME / Commercial

- 5.3.3 Large Enterprise / Corporate

- 5.3.4 Government / Public Sector

- 5.4 By Country

- 5.4.1 India

- 5.4.2 China

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 South-East Asia

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ZhongAn

- 6.4.2 Policybazaar

- 6.4.3 Acko

- 6.4.4 PasarPolis

- 6.4.5 Singlife

- 6.4.6 OneDegree

- 6.4.7 CXA Group

- 6.4.8 Waterdrop

- 6.4.9 Koala

- 6.4.10 CoverGo

- 6.4.11 Bolttech

- 6.4.12 Shift Technology

- 6.4.13 CarDekho (Insurance arm)

- 6.4.14 Turtlemint

- 6.4.15 Tokio Marine & Nichido (Digital Lab)

- 6.4.16 Ping An OneConnect

- 6.4.17 Munich Re Digital Partners

- 6.4.18 FWD Group

- 6.4.19 Sompo Himaraya

- 6.4.20 NTUC Income (Income Insurance)

7 Market Opportunities & Future Outlook

- 7.1 Cross-border expansion patterns and market consolidation trends

- 7.2 Emerging technology applications and regulatory changes