PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043897

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043897

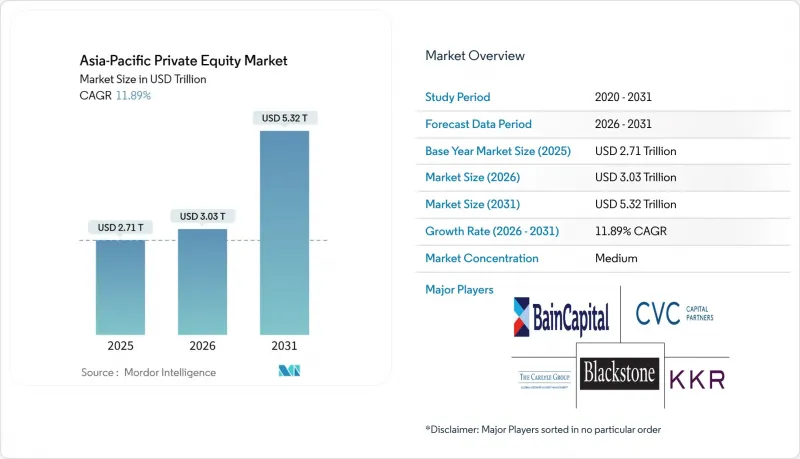

Asia-Pacific Private Equity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Asia-Pacific Private Equity Market size is expected to grow from USD 2.71 trillion in 2025 to USD 3.03 trillion in 2026 and is forecast to reach USD 5.32 trillion by 2031 at 11.89% CAGR over 2026-2031.

The region has become a priority destination for global institutional capital as investors rebalance exposure away from slower-growing developed economies. Large sovereign wealth and pension investors continue to amplify deal sizes, while a widening bank-funding gap lifts direct-lending volumes. Geopolitical realignment is prompting sponsors to diversify holdings beyond mainland China into India, Japan, and selected ASEAN economies. Meanwhile, digitalisation, ageing demographics, and energy transition are expanding thematic deal pipelines across technology, healthcare, and infrastructure sectors, supporting long-term growth prospects within the Asia-Pacific private equity market.

Asia-Pacific Private Equity Market Trends and Insights

Record Dry-Powder Deployment Transforms Capital Allocation

Sovereign wealth and pension investors hold roughly 34% of global sovereign assets and lifted private-market allocations by 10% annually during the past decade. The pool of undeployed capital has pushed deal tickets higher, with Asia-Pacific sovereign funds alone steering USD 79.4 billion into private-equity deals in 2023. Gulf investors joined Singapore's GIC in multi-billion-dollar co-investments, confirming a trend toward fee-saving, governance-rich structures. Deployment, however, is now more selective as Singapore state entities trimmed aggregate commitments by more than 50% in 2023 while Gulf peers accelerated exposure in technology and infrastructure assets. The new capital mix is compressing entry yields but simultaneously deepening the liquidity stack available to general partners. Overall, ample dry-powder continues to anchor bid momentum across the Asia-Pacific private equity market.

Japan-Korea Succession Crisis Accelerates Corporate Restructuring

Ageing ownership profiles and governance reform have propelled Japanese companies to divest USD 56 billion in non-core units since 2022, the highest cumulative value since the global financial crisis. Carve-outs now represent 12.6% of Asia-Pacific buyouts, up from 5.7% just three years ago, signalling a structural rather than cyclical shift. The USD 15 billion Toshiba take-private illustrates sponsor appetite for complex, multi-business restructurings, while Carlyle's USD 3 billion Japan-focused vehicle underscores long-duration commitment to the theme. South Korean chaebols face parallel demographic pressures, spurring cross-border M&A that allows regional PE houses to consolidate industrial supply chains. Dedicated on-the-ground teams give global firms execution speed and cultural fluency, translating into competitive advantages in bilateral negotiations. These factors together lift the short-term growth contribution embedded in the Asia-Pacific private equity market.

Geopolitical Bifurcation Fragments Cross-Border Capital Flows

Roughly USD 1.5 trillion of Chinese assets remain locked inside older PE vintages, with secondary buyers requesting discounts above 60% versus 15% in the United States and Europe. Leading global franchises executed only five new onshore China deals in 2024 after completing 30 in 2021, while Sequoia split into three regional brands to ring-fence regulatory exposure. CFIUS has expanded filing mandates, adding diligence costs and potentially civil penalties for non-compliance, thereby raising friction for cross-border LP funding. Chinese LPs are reshuffling Western fund stakes, evidenced by the USD 1 billion secondary sale plan tabled by China Investment Corporation. The cumulative effect is a liquidity logjam that redirects sponsor focus toward India, Japan and Southeast Asia. This fragmentation dilutes historical return correlations but subtracts near-term growth impulse from the Asia-Pacific private equity market.

Other drivers and restraints analyzed in the detailed report include:

- Private Credit Surge Fills Traditional Banking Void

- Digital Platform Proliferation Drives Mid-Market Innovation

- Extended Holding Periods Compress Investment Returns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Buyout & Growth strategies retained 28.35% of the Asia-Pacific private equity market share in 2025, anchored by large-ticket transactions like the USD 7.11 billion ESR take-private. The segment benefits from stronger governance control and the ability to drive operational turnarounds. Venture Capital, however, is forecast to advance at a 13.97% CAGR between 2026 and 2031 as digital adoption accelerates in ASEAN and South Asia. This growth pulls increasing allocations from family offices and global university endowments seeking early-stage technology positions, reinforcing the Asia-Pacific private equity market as an innovation gateway.

The Asia-Pacific private equity market size attributed to Venture Capital deals is projected to expand rapidly, whereas Mezzanine & Distressed strategies profit from corporate deleveraging in Japan and Korea, where ageing owners pursue liquidity solutions. Secondaries and Fund-of-Funds managers are scaling regional platforms as limited partners demand portfolio rebalancing and interim liquidity. The broader Asia-Pacific private equity industry is also witnessing rising hybrid strategies that blend minority equity stakes with private credit tranches to optimise risk-adjusted returns.

The Asia-Pacific Private Equity Market is Segmented by Fund Type (Buyout and Growth, Venture Capital, Mezzanine, and More), Sector (Technology, Healthcare, Real Estate, Financial Services, Industrials, Telecom, and More), Investments (Large Cap, Upper-Middle Market, and More), and Country (India, China, Japan, Australia, South Korea and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Blackstone

- KKR

- Carlyle Group

- Bain Capital

- CVC Capital Partners

- Warburg Pincus

- Nippon Sangyo Suishin Kiko (NSSK)

- Everstone Capital

- J-STAR

- Ascent Capital

- TPG Capital

- EQT

- Permira

- PAG

- Ares Management

- Brookfield Asset Management

- Hillhouse Capital

- Temasek Holdings

- GIC

- SoftBank Investment Advisers (Vision Fund)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Record dry-powder levels from sovereign & pension LPs

- 4.2.2 Surge in succession-driven corporate carve-outs (Japan/Korea)

- 4.2.3 Rapid growth of private-credit deals filling bank-funding gap

- 4.2.4 Digital-native mid-market platforms in ASEAN & India

- 4.2.5 Regulatory liberalization of foreign ownership caps

- 4.2.6 Net-zero infrastructure push (renewables, EV supply chains)

- 4.3 Market Restraints

- 4.3.1 US-China geo-political bifurcation dampening cross-border exits

- 4.3.2 Muted IPO window extending holding periods & IRR compression

- 4.3.3 FX volatility & rate divergence eroding leveraged-buyout returns

- 4.3.4 ESG-driven DD delays & green-washing litigation risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Investors (LPs)

- 4.7.2 Bargaining Power of Portfolio Targets

- 4.7.3 Threat of New PE Entrants & Emerging Managers

- 4.7.4 Threat of Alternative Assets (Private Credit, Infrastructure)

- 4.7.5 Competitive Rivalry among PE Funds

- 4.8 ESG & Sustainability Trends Shaping Deals

5 Market Size & Growth Forecasts

- 5.1 By Fund Type

- 5.1.1 Buyout & Growth

- 5.1.2 Venture Capital

- 5.1.3 Mezzanine & Distressed

- 5.1.4 Secondaries & Fund of Funds

- 5.2 By Sector

- 5.2.1 Technology (Software)

- 5.2.2 Healthcare

- 5.2.3 Real Estate and Services

- 5.2.4 Financial Services

- 5.2.5 Industrials

- 5.2.6 Consumer & Retail

- 5.2.7 Energy & Power

- 5.2.8 Media & Entertainment

- 5.2.9 Telecom

- 5.2.10 Others (Transportation, etc.)

- 5.3 By Investments

- 5.3.1 Large Cap

- 5.3.2 Upper Middle Market

- 5.3.3 Lower Middle Market

- 5.3.4 Small & SMID

- 5.4 By Geography

- 5.4.1 India

- 5.4.2 China

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves & Deal Flow

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Blackstone

- 6.4.2 KKR

- 6.4.3 Carlyle Group

- 6.4.4 Bain Capital

- 6.4.5 CVC Capital Partners

- 6.4.6 Warburg Pincus

- 6.4.7 Nippon Sangyo Suishin Kiko (NSSK)

- 6.4.8 Everstone Capital

- 6.4.9 J-STAR

- 6.4.10 Ascent Capital

- 6.4.11 TPG Capital

- 6.4.12 EQT

- 6.4.13 Permira

- 6.4.14 PAG

- 6.4.15 Ares Management

- 6.4.16 Brookfield Asset Management

- 6.4.17 Hillhouse Capital

- 6.4.18 Temasek Holdings

- 6.4.19 GIC

- 6.4.20 SoftBank Investment Advisers (Vision Fund)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment