PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043912

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043912

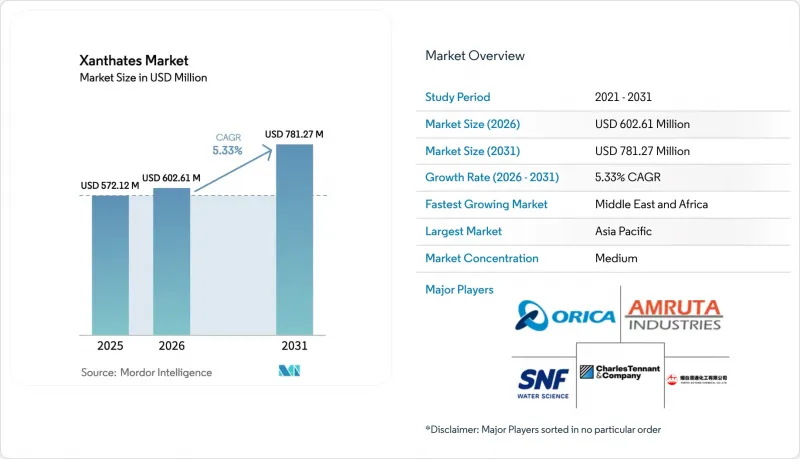

Xanthates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Xanthates Market size is projected to expand from USD 572.12 million in 2025 and USD 602.61 million in 2026 to USD 781.27 million by 2031, registering a CAGR of 5.33% between 2026 to 2031.

Collector demand is surging in the Democratic Republic of Congo (DRC), Zambia, Chile, and Peru, driven by new flotation circuits for copper, cobalt, and lithium. These projects are pushing sulfide-ore throughput beyond historical levels. While the Asia-Pacific region continues to anchor consumption, the Middle-East is poised to outpace all others. This shift is evident as Congolese concentrators and Zambian smelter-feed operations expand their reagent budgets. Liquid xanthate formulations are becoming increasingly popular. They mitigate dust-handling risks and reduce carbon-disulfide (CS2) off-gassing. This trend aligns with the United States and European Union's stringent limits on occupational exposure and tailings water. Concurrently, artificial-intelligence (AI) dosing platforms are boosting overall collector consumption. They achieve this by maximizing net present value from lower-grade stockpiles, even as the intensity of reagents per tonne decreases.

Global Xanthates Market Trends and Insights

Booming Critical-Minerals Projects in Africa and Latin America

In 2025, Ivanhoe Mines' Kamoa-Kakula complex in the DRC achieved an annualized copper output. By 2027, the complex is set to roll out a Phase 3 concentrator, which is expected to increase the demand for sodium isopropyl xanthate. Simultaneously, capacity expansions at Chile's Centinela and Quebrada Blanca Phase 2, along with Argentina's PSJ Cobre Mendocino development, are projected to collectively augment copper-concentrate output by 2027. This growth is anticipated to drive new collector offtake during the forecast period of 2026-2031. With these advancements, the Andean-Corridor and the Central-African Copperbelt are solidifying their positions as leading players in the xanthates market.

Shift to Liquid Xanthate Logistics at Remote Mines

Clariant's HOSTAFLOT liquid grades have streamlined operations by eliminating the need for on-site dissolution tanks and reducing reagent preparation time. These advantages have been realized at lithium brine operations in Chile and iron ore sites in Australia. In Peru's high-Andes copper belt, both Antamina and Las Bambas reported a notable drop in reagent-handling incidents after transitioning to pre-dissolved sodium isopropyl xanthate. Furthermore, these liquid collectors, by curbing CS2 volatilization, help mines comply with the European Union's stringent cap of 50 mg/m3, and OSHA's average limit of 20 ppm over time. This regulatory push is catalyzing a rapid shift in the product mix toward liquid solutions.

Commercialisation of Ligand-Based Xanthate-Free Collectors

In Chilean pilot trials, Solvay's Aero MX 5004 thionocarbamate outperformed sodium isopropyl xanthate, achieving higher copper recovery. Additionally, it successfully reduced tailings CS2 levels to below the permissible limit, adhering to the DS 90 water-quality standard. Meanwhile, in 2025, BASF's Lupromin-D hydroxamates enabled a nickel mine in the Philippines to completely eliminate xanthate from its oxide circuits. With dosing levels significantly reduced compared to conventional methods and a decrease in waste-treatment costs, the mine realized notable operating savings. This is particularly significant in regions with stringent emissions regulations, which in turn curtail the long-term growth of the xanthates market.

Other drivers and restraints analyzed in the detailed report include:

- AI-Optimized Reagent Dosing Boosting Collector Consumption

- Surge in Alkaline Battery Recycling Requiring Xanthate Leaching Aids

- EU Tailings Directive Lowering Allowable CS2 Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, sodium isopropyl xanthate commanded a 34.28% share of the xanthates market, driven by its superior selectivity in copper-pyrite separation and a strong presence in porphyry deposits. This leading grade forms the backbone of premium blended-collector systems, achieving recovery gains over sodium-ethyl counterparts. Potassium amyl xanthate has emerged as the fastest-growing player, boasting a 6.18% CAGR through 2031. Its edge comes from a stronger adsorption on fine-grained sulfides, particularly in refractory gold and intricate polymetallic ores. Sodium isobutyl xanthate remains a favored choice in lead-zinc flowsheets, notably in Australia's Broken Hill and China's Yunnan Province. Its mid-chain length strikes an ideal balance between power and selectivity. Meanwhile, sodium ethyl xanthate, despite its cost-effectiveness, is losing traction in premium copper and gold circuits. These circuits are now leaning toward stricter CS2 limits and enhanced metallurgical performance.

Potassium salts are gaining traction in the xanthates market, primarily due to their heightened solubility. This attribute reduces handling volumes, a significant logistical advantage for remote mining sites in Africa and Australia. Another burgeoning segment is blended formulations. For instance, a 60:40 mix of isopropyl and amyl xanthate boosted combined copper-zinc recovery at a Peruvian polymetallic mine in 2025. This success underscores suppliers' momentum toward tailored pre-mixes. Such developments indicate that innovations focusing on chain length, solubility, and blending techniques will reshape the competitive landscape of the xanthates market.

The Xanthates Market Report is Segmented by Product Type (Sodium Ethyl Xanthate, Sodium Isopropyl Xanthate, Sodium Isobutyl Xanthate, Potassium Amyl Xanthate, and Other Product Types), Application (Mining, Rubber Processing, Agrochemicals, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region led the market, capturing 46.38% of total revenue. China's integrated clusters, with their robust xanthate capacity, primarily fueled exports to neighboring nations such as Indonesia, Vietnam, and the Philippines. In India, demand surged due to expansions at Hindustan Zinc's Rampura Agucha and Coal India's fine-coal flotation projects, resulting in increased collector offtake. Australia emerged as a self-sufficient sub-market, with BHP and Rio Tinto predominantly sourcing liquid xanthates from Orica and Coogee Chemicals. This strategic choice aimed to mitigate hazards in their operations located in Pilbara and Queensland.

While the Middle-East and Africa held a smaller market share, they boasted the fastest projected CAGR of 5.93% during the forecast period of 2026-2031. This growth was fueled by expansions at DRC's Kamoa-Kakula and Zambia's Kansanshi and Enterprise, which anticipated a heightened demand for collectors by 2028. In South Africa, Bushveld's platinum group augmented xanthate dosages via column flotation to compensate for reduced mechanical agitation. Simultaneously, Saudi Arabia's Ma'aden phosphate operations shifted from gravity methods to xanthate-assisted flotation, diversifying the regional reagent landscape.

North America made a significant contribution to the 2025 revenue, driven by projects in Arizona and Utah (copper and molybdenum), Ontario (gold), and zinc operations in Alaska and the Yukon. Europe experienced stagnation; while mine closures in Poland and Finland balanced out the baseline usage, new ventures like Woodsmith avoided xanthates to evade CS2 issues. South America, with a substantial market share, witnessed Codelco's widespread xanthate consumption across its divisions. The company is considering a strategic shift, aiming to substitute a segment of its sodium isopropyl volumes with Aero MX thionocarbamates starting in 2026, in line with its Scope 3 objectives. Additionally, persistent infrastructure challenges, notably the Copperbelt rail bottlenecks, elevated freight premiums and ignited interest in on-site synthesis. If this method gains traction, it holds the potential to diminish merchant volume.

- Amruta Industries

- Charles Tennant and Company

- Coogee Chemicals

- CTC Energy & Mining Company

- Florrea Chemicals

- Kemcore

- Merck KGaA

- Orica Limited

- Qingdao Ruchang Mining Industry

- QiXia TongDa Flotation Reagent Co. Ltd

- Senmin International (Pty) Ltd

- SNF Flomin

- SNF Group

- Thermo Fisher Scientific Inc.

- Tieling Flotation Reagent Co. Ltd

- Vanderbilt Chemicals LLC

- Y&X Beijing Technology

- Yantai Humon Chemical Auxiliary Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming critical-minerals projects in Africa and Latin America

- 4.2.2 Shift to liquid xanthate logistics at remote mines

- 4.2.3 AI-optimised reagent dosing boosting collector consumption

- 4.2.4 Surge in alkaline battery recycling requiring xanthate leaching aids

- 4.2.5 Tightening Asia-Pacific supply of carbon-disulfide feedstock inflates prices

- 4.3 Market Restraints

- 4.3.1 Commercialisation of ligand-based xanthate-free collectors

- 4.3.2 EU tailings directive lowering allowable CS2 emissions

- 4.3.3 On-site CS2 cracking units enabling captive collector synthesis

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Sodium Ethyl Xanthate

- 5.1.2 Sodium Isopropyl Xanthate

- 5.1.3 Sodium Isobutyl Xanthate

- 5.1.4 Potassium Amyl Xanthate

- 5.1.5 Other Product Types

- 5.2 By Application

- 5.2.1 Mining

- 5.2.2 Rubber Processing

- 5.2.3 Agrochemicals

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Amruta Industries

- 6.4.2 Charles Tennant and Company

- 6.4.3 Coogee Chemicals

- 6.4.4 CTC Energy & Mining Company

- 6.4.5 Florrea Chemicals

- 6.4.6 Kemcore

- 6.4.7 Merck KGaA

- 6.4.8 Orica Limited

- 6.4.9 Qingdao Ruchang Mining Industry

- 6.4.10 QiXia TongDa Flotation Reagent Co. Ltd

- 6.4.11 Senmin International (Pty) Ltd

- 6.4.12 SNF Flomin

- 6.4.13 SNF Group

- 6.4.14 Thermo Fisher Scientific Inc.

- 6.4.15 Tieling Flotation Reagent Co. Ltd

- 6.4.16 Vanderbilt Chemicals LLC

- 6.4.17 Y&X Beijing Technology

- 6.4.18 Yantai Humon Chemical Auxiliary Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment