PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043922

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043922

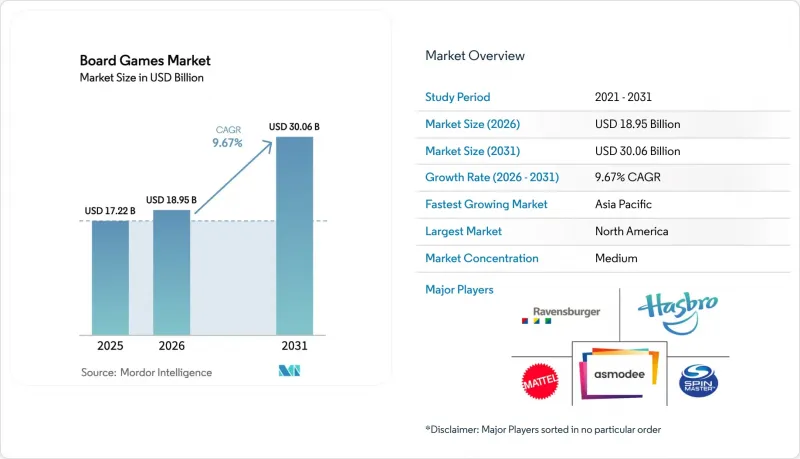

Board Games - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Board Games Market size is expected to grow from USD 17.22 billion in 2025 to USD 18.95 billion in 2026 and is forecast to reach USD 30.06 billion by 2031 at 9.67% CAGR over 2026-2031.

A structural pivot toward screen-free social recreation, greater willingness to pay for premium tactile products, and the growing profile of campaign-based formats are setting a faster growth trajectory than the wider toys and games category. Strategy and Euro-style titles remained the single largest contributor in 2025, yet cooperative and legacy games are tracking higher unit velocity as narrative depth keeps players invested for months and encourages expansion sales. Various federations and associations are championing the cause of increasing women's participation in board games. In a testament to this trend, the International Chess Federation (FIDE) revealed that in January 2025, China led the pack with its female players achieving an average top 10 rating of 2,48. Retail infrastructure is also evolving: specialty stores still anchor discovery, but double-digit e-commerce growth and convention-driven pre-orders are shifting volume to online and direct-to-consumer channels. Publisher consolidation at the top contrasts with a long tail of crowdfunded micro-studios that refresh the product cycle every quarter, sustaining consumer excitement and preventing SKU fatigue.

Global Board Games Market Trends and Insights

Growing interest in offline, screen-free entertainment

As screen fatigue becomes increasingly prevalent, leisure budgets are being redirected toward analog experiences that not only minimize blue-light exposure but also encourage authentic, face-to-face social interactions. For instance, 27% of U.S. college students felt tired or sleepy within the past seven days as of fall 2025, according to the National College Health Assessment. This growing demand is particularly noticeable among millennials and Gen Z parents. While these generations grew up immersed in digital entertainment, they are now prioritizing hands-on, tactile play experiences for their children. To cater to this shift, publishers are introducing features such as quick-start rules and tutorial videos, which are conveniently accessible through QR codes. These additions aim to reduce the mental effort that has traditionally discouraged casual buyers from engaging with analog games. Furthermore, this trend is self-perpetuating: as households accumulate collections of 5 to 10 game titles, they increasingly organize regular game nights. These gatherings not only establish analog leisure as a norm within their social networks but also significantly enhance word-of-mouth promotion and discovery.

Resurgence of analog entertainment

Over the past three years, vinyl records, film cameras, and mechanical watches have experienced significant double-digit growth. This trend underscores a broader consumer inclination toward products that defy planned obsolescence and retain their resale value over time. Board games have also capitalized on this nostalgia-driven materialism. Premium editions, which often include features such as custom miniatures, screen-printed boxes, and metal coins, command prices that are 18% higher than standard mass-market versions. Despite the higher price point, these editions frequently sell out within weeks of being fulfilled through Kickstarter campaigns. Collectors increasingly regard these premium board games as investment-grade assets. For example, out-of-print titles from publishers like CMON and Awaken Realms have appreciated by 30% to 50% in secondary markets. This dynamic has encouraged publishers to adopt strategies that intentionally limit print runs, leveraging scarcity as a powerful marketing tool. This approach not only sustains elevated pricing for premium editions but also attracts speculators, who further amplify demand and contribute to the ongoing growth of this segment.

Competition from digital gaming and streaming

Free-to-play models effectively eliminate the upfront cost barrier, making board games more accessible to casual buyers who might otherwise hesitate to invest. Additionally, live-service updates consistently provide new content on a weekly basis, ensuring players remain engaged without incurring any additional costs. By late 2025, Wizards of the Coast's Magic: The Gathering Arena had successfully attracted over 50 million players. The company leveraged its intellectual property (IP) through a dual-channel monetization strategy, combining physical booster pack sales with digital microtransactions. While this approach may reduce some traditional analog sales, it significantly expands the total addressable market by appealing to digital-first users. Many of these users eventually transition to purchasing physical cards for tournament play, further driving revenue. At the same time, streaming platforms such as Netflix and Disney+ continue to dominate discretionary leisure time. With the average U.S. household spending 4.5 hours daily on video consumption, the availability of time for 60 to 90-minute board-game sessions has become increasingly limited.

Other drivers and restraints analyzed in the detailed report include:

- Popularity of board-game cafes and social spaces

- Strong gifting culture around holidays and special occasions

- Counterfeit and IP-infringing titles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cooperative and Legacy titles are projected to grow at a 10.74% CAGR, surpassing the overall board games market by 110 basis points. In 2024, this genre recorded an additional 20 million units sold, with 70% of its customer base being female-indicating an expansion beyond the traditionally male-dominated strategy niche. Legacy mechanics, which engage groups in 12-20 session arcs, redirect spending from competing SKUs mid-campaign while increasing attach rates for expansions. Stonemaier's 2026 roadmap, which includes Wingspan and Scythe extensions, highlights the profitability of leveraging evergreen IP through high-value add-ons. Compliance with ASTM F963 toy-safety protocols remains essential for achieving widespread availability in U.S. retail outlets.

Strategy and Euro games, despite their maturity, accounted for the largest 28.02% share of 2025 revenue. Perennial favorites like Catan and Ticket to Ride benefit from steady replenishment orders, maintaining their presence in both big-box and specialty retail stores. Traditional games, Monopoly, Scrabble, Chess continue to perform well during the Q4 gifting season but are losing younger audiences to thematic games with engaging storylines. Card and Dice products, with their manufacturing costs under USD 10 and compact packaging that lowers freight expenses, remain reliable entry points for cost-conscious micro-publishers. Miniature wargames appeal to enthusiasts willing to spend over USD 100 on core sets; Tycoon Games' 2025 acquisition of Blood Rage and Rising Sun supports the idea that premium-component titles can sustain longer shelf lives. Additionally, educational hybrids designed to align with STEM curricula are being piloted in Californian and Texan school districts, reflecting a growing interest in gamified learning within educational institutions.

In 2025, adults contributed 48.26% of spending, driven by higher disposable incomes and a preference for 90-minute Eurogame sessions. Meanwhile, the children's segment is projected to grow at a strong 10.39% CAGR, as parents and educators increasingly look for screen-free, skill-building tools. In 2024, children under 12 accounted for over 60% of mass-market purchases, with school budgets expanding for products tied to curricula, such as those teaching coding logic and spatial reasoning.

Teenagers, operating within budgets of USD 20 to USD 40, are attracted to social-deduction party games like Werewolf and Secret Hitler. This trend was reinforced by Exploding Kittens' board-game launch at USD 24.99 in July 2025, which secured prominent end-cap placements at Target and Walmart. Adult preferences are diverging: casual players prefer cooperative games under an hour, while hobbyists are investing in multi-season legacy boxes. Publishers are now developing modular rules that adapt in complexity, enabling a single SKU to appeal to players with varying experience levels and optimizing returns on design investments.

The Board Games Market Report is Segmented by Game Type (Traditional, Strategy/Euro, Card/Dice, Cooperative/Legacy, Miniatures, Educational), Age Group (Children, Teenagers, Adults), Category (Mass, Premium), Distribution Channel (Hypermarkets, Specialty Stores, Online Retail, Others), and Geography (North America, South America, Europe, Asia-Pacific, MEA). Market Forecasts are in Value (USD) and Volume (Units).

Geography Analysis

In 2025, North America accounted for 38.41% of the global turnover, with the U.S. contributing over 60% of the regional value. Around 1,200 dedicated game shops support a thriving discovery and tournament ecosystem. In early 2026, tariffs on Chinese components, reaching up to 145%, reduced gross margins by 3-5 percentage points. This led to a shift towards nearshoring in Mexico, where wages are 30%-40% lower than in the U.S., and freight lead times have decreased to 10 days. Hasbro reported USD 4.7 billion in revenue for 2025, with Wizards of the Coast contributing USD 2.2 billion, highlighting the effectiveness of a dual analog-digital model that outperforms category averages. USMCA tariff exemptions are driving assembly operations to Monterrey and Toronto, strengthening North America's supply chain resilience.

Asia-Pacific is projected to grow at a 10.97% CAGR through 2031. Although China's growth is hindered by regulatory challenges such as the NPPA content review, which can extend lead times by up to 18 months, rising disposable income continues to drive demand. India is expected to lead regional growth as urban families increasingly adopt board games as an affordable entertainment option, supported by widespread English fluency. Japan and South Korea are becoming key markets for premium collector editions, with conventions in Tokyo and Seoul drawing 30,000-40,000 attendees annually. Rising labor costs in China and geopolitical tensions are prompting publishers to diversify manufacturing to Vietnam and India, enhancing supply-chain flexibility.

Europe recorded moderate growth, led by Germany and the UK. The 2023 Essen Spiel event attracted 162,000 visitors and generated EUR 15 million in sales, reinforcing Germany's position as the hub of Eurogame design. While the EU's Extended Producer Responsibility laws introduce cost pressures, they also provide a competitive advantage for early adopters. South America and the Middle East and Africa collectively contributed less than 10% of global revenue. However, Brazil and the UAE are emerging as key regional players. Brazil benefits from nearshoring trends that reduce lead times to North America, while the UAE's multilingual expatriate population drives demand for premium English-language imports.

- Hasbro Inc.

- Mattel Inc.

- Asmodee Group

- Ravensburger AG

- Spin Master Corp.

- Goliath Games BV

- CMON Limited

- IELLO Games

- Stonemaier Games LLC

- Czech Games Edition

- North Star Games LLC

- Blue Orange Games

- Thames and Kosmos

- Midlam Miniatures

- Z-Man Games

- Wizards of the Coast

- Lucky Duck Games

- Exploding Kittens LLC

- Renegade Game Studios

- Plaid Hat Games

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing interest in offline, screen?free entertainment

- 4.2.2 Resurgence of Analog Entertainment

- 4.2.3 Popularity of Board-Game Cafes and Social Spaces

- 4.2.4 Crowdfunding-Driven Democratization of Publishing

- 4.2.5 Eco-friendly Production Boosting Brand Affinity

- 4.2.6 Strong gifting culture around holidays and special occasions

- 4.3 Market Restraints

- 4.3.1 Competition from Digital Gaming and Streaming

- 4.3.2 Counterfeit and IP - infringing Titles

- 4.3.3 Localization and translation challenges

- 4.3.4 Paper and Pulp Supply Shortages

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Game Type

- 5.1.1 Traditional/Classics

- 5.1.2 Strategy/Euro

- 5.1.3 Card and Dice

- 5.1.4 Cooperative/Legacy

- 5.1.5 Miniature Wargames

- 5.1.6 Educational and Puzzle Hybrids

- 5.2 By Age Group

- 5.2.1 Children

- 5.2.2 Teenagers

- 5.2.3 Adults

- 5.3 By Category

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By Distribution Channel

- 5.4.1 Hypermarkets and Supermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Chile

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Sweden

- 5.5.3.8 Belgium

- 5.5.3.9 Poland

- 5.5.3.10 Netherlands

- 5.5.3.11 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Thailand

- 5.5.4.5 Singapore

- 5.5.4.6 Indonesia

- 5.5.4.7 South Korea

- 5.5.4.8 Australia

- 5.5.4.9 New Zealand

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Hasbro Inc.

- 6.4.2 Mattel Inc.

- 6.4.3 Asmodee Group

- 6.4.4 Ravensburger AG

- 6.4.5 Spin Master Corp.

- 6.4.6 Goliath Games BV

- 6.4.7 CMON Limited

- 6.4.8 IELLO Games

- 6.4.9 Stonemaier Games LLC

- 6.4.10 Czech Games Edition

- 6.4.11 North Star Games LLC

- 6.4.12 Blue Orange Games

- 6.4.13 Thames and Kosmos

- 6.4.14 Midlam Miniatures

- 6.4.15 Z-Man Games

- 6.4.16 Wizards of the Coast

- 6.4.17 Lucky Duck Games

- 6.4.18 Exploding Kittens LLC

- 6.4.19 Renegade Game Studios

- 6.4.20 Plaid Hat Games

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK