PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043932

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043932

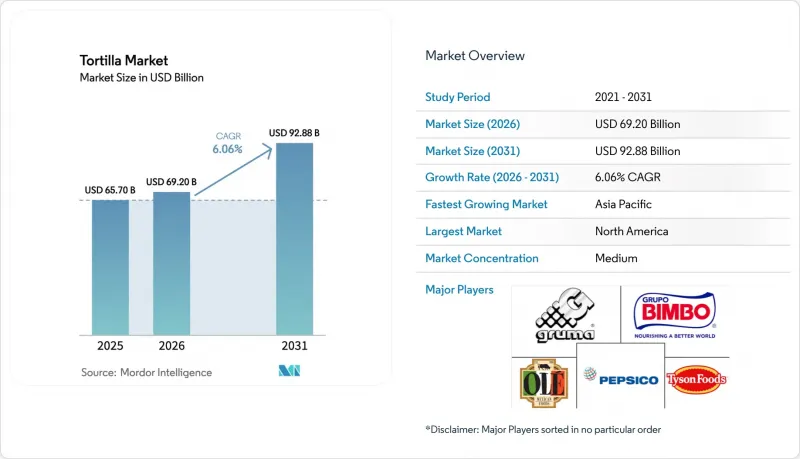

Tortilla - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The tortilla market size is projected to expand from USD 65.70 billion in 2025 and USD 69.20 billion in 2026 to USD 92.88 billion by 2031, registering a CAGR of 6.06% between 2026 to 2031.

The growing demand for convenient and portable meal options, coupled with the increasing popularity of Mexican and Texan-Mexican (Tex-Mex) cuisine, is significantly driving the expansion of the tortilla market. Quick-service restaurants are progressively shifting their focus toward tortilla-based menus, which is further contributing to market growth. Frozen tortillas have emerged as the fastest-growing segment, supported by advancements in cold-chain logistics across emerging markets. While gluten-free formulations account for a smaller share of the market, they command premium shelf space, underscoring the impact of health-conscious segmentation on profit margins. The competitive intensity within the market remains moderate, as major players like GRUMA (Gruma, S.A.B. de C.V.) and Grupo Bimbo leverage their scale advantages. However, niche brands are increasingly fragmenting the market share by catering to specific micro-segments, including grain-free and clean-label product categories.

Global Tortilla Market Trends and Insights

Rising demand for convenient, portable meal options like wraps and burritos

Time-constrained consumers are driving a shift toward grab-and-go formats, with tortillas serving as the base for burritos, wraps, and quesadillas that provide complete nutrition in a portable form. This trend is particularly evident in urban areas where commute times exceed one hour, and limited time for meal preparation has increased demand for products requiring minimal assembly and suitable for on-the-go consumption. The frozen burrito category has grown significantly, supported by cryogenic freezing technologies that maintain texture and flavor, allowing manufacturers to distribute products nationally without compromising quality. An example is West Liberty Foods' BBQ Chicken Wrap Ingredient Pack, which includes flour tortillas, pre-cooked proteins, and sauces in a 70-day refrigerated format, helping reduce labor and improve efficiency in foodservice kitchens. Retail channels are also adapting to this trend, with supermarkets allocating more shelf space to refrigerated tortilla sections featuring flavored wraps such as tomato basil, spinach herb, and garlic herb, which are designed to enhance meal quality without requiring advanced culinary skills.

Growing popularity of ethnic cuisines, especially Tex-Mex and Mexican fusion globally

Mexican and Tex-Mex cuisines have seen significant growth in popularity across non-traditional markets, with tortillas now commonly available in mainstream European and Asian supermarkets alongside local flatbreads. In Europe, Spain is at the forefront of this trend, with tortilla sales increasing as consumers embrace fusion dishes that blend Spanish ingredients with Mexican culinary techniques, such as chorizo-filled tacos and patatas bravas quesadillas. In the Asia-Pacific region, localized flavor innovations reflect this trend, including seaweed-infused tortillas in Japan, curry-spiced versions in India, and kimchi wraps in South Korea. These adaptations align with regional taste preferences while retaining the convenience of the tortilla format. The expansion of this culinary fusion is further supported by social media, which amplifies food trends, and by younger consumers who prioritize experiential dining over traditional meal formats. To take advantage of this trend, brands should invest in regional flavor research and development and collaborate with local chefs to strengthen their position in high-growth markets. In contrast, brands that depend solely on standardized products risk becoming commoditized.

Stringent food safety and labeling regulations varying by region

Regulatory fragmentation across jurisdictions increases compliance costs, placing a heavier burden on smaller manufacturers that lack dedicated regulatory affairs teams. For example, California's requirement for folic acid fortification in corn masa products differs from federal Food and Drug Administration (FDA) standards, compelling producers serving the state to maintain separate formulations and labeling. Similarly, the European Union's upcoming restrictions on certain preservatives and the Food and Drug Administration's ban on titanium dioxide necessitate reformulation efforts, straining research and development budgets and delaying product launches. The European Food Safety Authority's differing stance on enzyme use in dough conditioning further complicates transatlantic trade, as products approved in the United States may require re-certification for European markets, extending time-to-market and increasing legal expenses [2]. These regulatory differences benefit larger companies such as GRUMA and Grupo Bimbo, which have dedicated compliance functions and can spread certification costs across high-volume production. In contrast, regional players must either limit their geographic reach or accept reduced margins to manage compliance costs across multiple jurisdictions.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of quick-service restaurants and fast-casual chains using tortillas

- Increasing adoption of gluten-free corn-based tortillas for dietary needs

- Short shelf life of fresh tortillas leading to spoilage risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tortilla chips are projected to grow at a compound annual growth rate (CAGR) of 7.32% through 2031, surpassing other product types as manufacturers focus on flavor innovation and functional nutrition to expand snacking occasions beyond traditional dip-and-chip consumption. Examples include PepsiCo's Tostitos Mexican Street Corn and Doritos Protein (10 grams per serving), which demonstrate how established players utilize research and development capabilities to introduce limited-edition flavors and protein-enriched variants. These products command premium pricing and appeal to health-conscious millennial consumers. Corn tortillas accounted for 39.11% of the product-type share in 2025, driven by their cultural authenticity in Mexican cuisine and gluten-free attributes. However, their growth is slowing as flour tortillas gain popularity in fusion applications, where their larger diameter and greater flexibility support wrap-style formats. Tostadas and taco shells remain niche products, primarily used by foodservice operators seeking pre-formed shells for labor efficiency and portion control. Despite this, their combined market share remains below 15% due to limited versatility compared to flat tortillas, which can be shaped post-production.

Flour tortillas are experiencing growth driven by the increasing popularity of wraps and burritos, particularly in North America and Europe, where consumers associate larger-diameter tortillas with meal completeness and value. The segment faces a strategic balance between authenticity and functionality: corn tortillas provide cultural authenticity and health benefits, while flour tortillas offer better tear resistance and a neutral flavor profile suitable for diverse fillings. Manufacturers are addressing this by introducing hybrid formulations such as corn-flour blends, whole-grain options, and flavored wraps (e.g., spinach, tomato basil), which combine the strengths of both types. Mission Foods' variety packs, which include multiple flavors in foodservice-sized cases, illustrate how operators are leveraging assortment strategies to gauge consumer preferences without committing to single stock-keeping units (SKUs).

Fresh and shelf-stable tortillas accounted for 63.82% of the form-based market share in 2025, while frozen variants are growing at a compound annual growth rate (CAGR) of 6.99%, driven by advancements in enzyme technologies and improved packaging that address texture degradation issues. Enzymes such as maltogenic amylase and phospholipase are being utilized to maintain pliability after thawing, while hydrocolloids like guar and carob gums help retain moisture during freeze-thaw cycles. These innovations mitigate brittleness and dryness, which previously limited the appeal of frozen tortillas. This progress is enabling national distribution for brands without regional production facilities, providing smaller players with market access if they invest in frozen formulations. For example, Tia Lupita Foods ships cactus tortillas frozen via United States Postal Service (USPS) Priority. This logistics approach avoids the high costs of refrigerated trucking while ensuring product integrity through expedited parcel delivery timelines.

Fresh tortillas continue to dominate foodservice channels where operators prioritize authentic texture and manage short shelf lives through high turnover rates. However, in retail, consumer preferences are shifting toward frozen tortillas due to their extended storage capabilities, even if they come with minor texture differences. Manufacturers' strategies depend on their channel focus. Portfolios heavily reliant on foodservice favor fresh production with regional plants, while retail-focused strategies increasingly justify investments in frozen production capacity. These investments enable geographic expansion without proportional increases in logistics costs. Shelf-stable tortillas occupy an intermediate position, offering ambient distribution without refrigeration but requiring preservatives that conflict with clean-label preferences. This trade-off limits their appeal in premium market segments. As a result, form-based segmentation is fragmenting along channel and price-tier lines. Fresh tortillas dominate foodservice and premium retail, frozen tortillas are gaining traction in mass-market retail, and shelf-stable formats cater to price-sensitive and infrastructure-constrained markets.

The Tortilla Market Report is Segmented by Product Type (Tostadas, Corn Tortillas, Flour Tortillas, Tortilla Chips, and Taco Shells), Form (Fresh/Shelf Stable and Frozen), Category (Regular and Gluten-Free), Distribution Channel (Foodservice and Institutions and Retail), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 46.83% of the geographic market share in 2025, driven by the region's strong cultural connection to Mexican cuisine, well-established quick-service restaurant (QSR) infrastructure, and high per-capita consumption of convenience foods. However, growth is slowing due to market saturation and demographic changes that are reducing the expansion of Hispanic populations, which have historically driven category adoption. The United States continues to be the largest national market for tortillas. The retail tortilla growth rate indicates a maturing category, with incremental gains driven by premiumization trends, such as organic, gluten-free, and protein-fortified options, rather than increases in volume. In Mexico, the market is deeply rooted in cultural traditions but faces economic volatility. Tortilla prices increased significantly in 2022, following a notable rise in international maize prices. This highlights how reliance on commodity imports and limited domestic self-sufficiency exacerbate inflationary pressures on consumers. In Canada, consistent demand is supported by urban multiculturalism and the penetration of quick-service restaurants, though per-capita consumption remains lower than in the United States, which limits overall growth potential.

The Asia-Pacific region is experiencing significant growth, with a projected compound annual growth rate (CAGR) of 8.12 percent through 2031. Urbanization, rising disposable incomes, and culinary globalization are driving tortilla adoption in markets where the product was virtually unknown a decade ago. China and India are the primary growth drivers, with tortillas positioned as convenient alternatives to traditional flatbreads such as roti, naan, and baozi wrappers in urban centers where time constraints and Western food trends are reshaping meal patterns. In Japan and South Korea, localized flavor variants such as seaweed and kimchi are aligning tortillas with regional taste preferences. Meanwhile, Australia's established Mexican-food culture provides a mature base for premium and organic segments. In Southeast Asia, including Thailand, Indonesia, and Singapore, tortillas are in the early stages of adoption, primarily distributed through modern retail chains and international QSR franchises. However, infrastructure constraints and price sensitivity limit penetration beyond affluent urban populations. For brands targeting Asia-Pacific, localization is critical, including flavor adaptation, halal certification in Muslim-majority markets, and partnerships with regional retailers and foodservice operators to build category awareness and encourage trial.

Europe's tortilla market exhibits mixed growth patterns. The United Kingdom's market is relatively mature, supported by chains like Tortilla UK and widespread supermarket distribution. However, growth is slowing as the category nears saturation in urban areas. Regulatory harmonization under the European Food Safety Authority (EFSA) provides a unified compliance framework, reducing market-entry barriers for pan-European brands. Nonetheless, cultural fragmentation, such as varying taste preferences, meal structures, and retail formats, necessitates country-specific strategies rather than a one-size-fits-all approach. In South America, growth is concentrated in Brazil, Argentina, and Chile, where urbanization and rising middle-class incomes are driving demand for packaged and frozen tortillas. However, the region's cultural preference for fresh, locally produced foods limits the appeal of shelf-stable imports. This dynamic underscores the need for localized strategies to address consumer preferences while leveraging urban growth trends. The Middle East and Africa remain emerging markets for tortillas. Distribution is primarily through hypermarkets in Gulf Cooperation Council countries such as the United Arab Emirates and Saudi Arabia, as well as urban areas in South Africa. However, limited cold-chain infrastructure and low consumer awareness constrain near-term growth. These regions represent long-term opportunities, contingent on investments in infrastructure and efforts to educate consumers about the category.

- GRUMA S.A.B. de C.V.

- Grupo Bimbo S.A.B. de C.V.

- PepsiCo Inc.

- Ole Mexican Foods Inc.

- Tyson Foods Inc.

- La Tortilla Factory

- Azteca Foods Inc.

- Liven SA

- Siete Family Foods

- Tia Lupita Foods

- Azteca Milling

- General Mills Inc.

- Mission Foods Australia PTY

- Guerrero Tortillas

- Intersnack Group GmbH & Co. KG

- Flowers Foods Inc.

- Fireworks Foods

- Toufayan Bakeries

- Julio's Seasoning & Corn Chips, Inc.

- The Simply Good Foods Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for convenient, portable meal options like wraps and burritos

- 4.2.2 Growing popularity of ethnic cuisines, especially Tex-Mex and Mexican fusion globally

- 4.2.3 Expansion of quick-service restaurants (QSR) and fast-casual chains using tortillas

- 4.2.4 Increasing adoption of gluten-free corn-based tortillas for dietary needs

- 4.2.5 Urbanization leading to time-pressed lifestyles favoring ready-to-eat formats

- 4.2.6 Versatility in applications, from tacos to snacks and meal kits

- 4.3 Market Restraints

- 4.3.1 Stringent food safety and labeling regulations varying by region

- 4.3.2 Short shelf life of fresh tortillas leading to spoilage risks

- 4.3.3 Limited cold chain infrastructure in emerging regions

- 4.3.4 Packaging waste concerns amid sustainability scrutiny

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Tostadas

- 5.1.2 Corn Tortillas

- 5.1.3 Flour Tortillas

- 5.1.4 Tortilla Chips

- 5.1.5 Taco Shells

- 5.2 By Form

- 5.2.1 Fresh/Shelf Stable

- 5.2.2 Frozen

- 5.3 By Category

- 5.3.1 Regular

- 5.3.2 Gluten-Free

- 5.4 By Distribution Channel

- 5.4.1 Foodservice and Institutions (B2B)

- 5.4.2 Retail (B2C)

- 5.4.2.1 Supermarkets and Hypermarkets

- 5.4.2.2 Convenience Stores

- 5.4.2.3 Online Retail Stores

- 5.4.2.4 Other Distribution Channel

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GRUMA S.A.B. de C.V.

- 6.4.2 Grupo Bimbo S.A.B. de C.V.

- 6.4.3 PepsiCo Inc.

- 6.4.4 Ole Mexican Foods Inc.

- 6.4.5 Tyson Foods Inc.

- 6.4.6 La Tortilla Factory

- 6.4.7 Azteca Foods Inc.

- 6.4.8 Liven SA

- 6.4.9 Siete Family Foods

- 6.4.10 Tia Lupita Foods

- 6.4.11 Azteca Milling

- 6.4.12 General Mills Inc.

- 6.4.13 Mission Foods Australia PTY

- 6.4.14 Guerrero Tortillas

- 6.4.15 Intersnack Group GmbH & Co. KG

- 6.4.16 Flowers Foods Inc.

- 6.4.17 Fireworks Foods

- 6.4.18 Toufayan Bakeries

- 6.4.19 Julio's Seasoning & Corn Chips, Inc.

- 6.4.20 The Simply Good Foods Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK