PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043950

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043950

Organic Edible Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

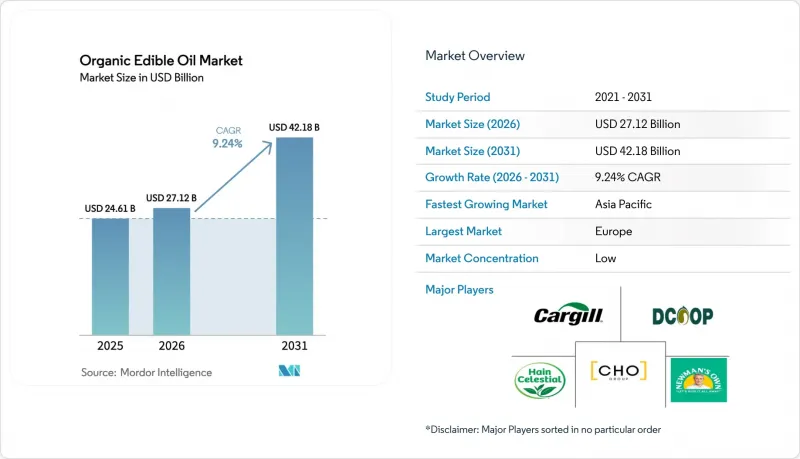

The organic edible oil market size is projected to expand from USD 24.61 billion in 2025 and USD 27.12 billion in 2026 to USD 42.18 billion by 2031, registering a CAGR of 6.73% between 2026 and 2031.

This surge in demand is driven by consumers moving away from chemical extractions, the adoption of cold-pressed technologies, and increased retail access to premium non-GMO products. While olive oil leads in value, processors are shifting focus to higher-margin oils like avocado, sesame, and specialty nut oils, prized for their resilience against oxidative breakdown during deep frying. Government incentives promoting organic acreage conversion, coupled with ESG-aligned investments in solvent-free extraction platforms, are alleviating historical supply constraints. Concurrently, online grocery platforms, notably quick-commerce apps in urban Asia, are simplifying purchases and bolstering repeat subscriptions for premium oils. The competitive landscape is moderately intense, with multinational giants vying for shelf space, while direct-to-consumer brands leverage single-origin narratives and blockchain traceability to build consumer trust.

Global Organic Edible Oil Market Trends and Insights

Rising health-conscious consumer base shifts to clean-label oils

Retailers and foodservice operators are reshaping their procurement strategies, increasingly favoring oils that are free from chemical solvents, trans fats, and genetically modified organisms. This shift, accelerated by post-pandemic wellness trends, sees consumers meticulously examining ingredient lists. Many are turning away from hexane-extracted oils, opting instead for expeller-pressed or cold-pressed variants that better preserve native antioxidants and essential fatty acids. Indian D2C brand Gramiyaa, for instance, saw its revenue jump from INR 10.9 crore (USD 1.3 million) in FY24 to INR 18.7 crore (USD 2.2 million) in FY25. This growth is attributed to their stringent quality control measures, which encompass batch-level testing and QR-coded traceability. The push for clean labels isn't confined to retail; foodservice operators are revamping their menus to spotlight organic oils. This is especially true for high-heat applications, where refined avocado oil, boasting a 500°F smoke point, outshines traditional canola or soybean oils. In Japan, while cooking oil consumption has dipped due to price inflation, premium olive and sesame oils have held their ground. Middle- and high-income households continue to favor these oils, valuing the perceived health benefits, as highlighted by Agriculture Canada.

Government incentives expanding certified organic acreage

Federal and regional programs are easing the financial burden of transitioning to organic farming, a process that usually mandates three years of chemical-free cultivation prior to certification. In 2024 and 2025, the USDA's Environmental Quality Incentives Program, Organic Transition Initiative, and Organic Certification Cost Share Program allocated funds to assist farmers in shifting conventional oilseed acreage to organic production. This move aims to alleviate the supply bottleneck that has hindered market growth. Meanwhile, EU member states have integrated organic farming objectives into their Common Agricultural Policy payments. This strategy encourages rapeseed, sunflower, and olive producers to seek EU Organic certification. In India, the Paramparagat Krishi Vikas Yojana provides financial support for developing organic clusters. However, oilseed farmers' adoption of this initiative lags behind their counterparts in cereals and pulses. While these programs aim to offset the opportunity cost of reduced yields during the transition, the three-year gap between program enrollment and achieving a certified harvest suggests that any relief in supply will only be realized in the medium to long term.

High production costs and premium pricing

Middle- and low-income markets find organic oils less affordable due to production costs being 40% to 60% higher than conventional oils. This price hike is attributed to factors like organic certification, lower crop yields, manual harvesting, and chemical-free extraction. Farms certified for organic oilseeds avoid synthetic fertilizers and pesticides, leading to a 20% to 30% drop in per-hectare yields compared to their conventional counterparts. Additionally, organic certification fees, annual inspections, and the need for segregated storage infrastructure introduce fixed costs that challenge small-scale farmers. Cold-press extraction, while favored for its purity, yields 10% to 15% less oil per kilogram of seed than methods like high-temperature screw pressing or hexane extraction, pushing up production costs per liter. These production inefficiencies are mirrored in retail prices. In the Asia-Pacific region, where disposable income growth lags behind food inflation, price sensitivity is pronounced. For instance, Japan's cooking oil market saw double-digit price surges, leading consumers to opt for cheaper blended oils and curtail their overall consumption. In response, processors are trialing "half-use" formulations, blending organic oils with conventional ones to achieve competitive pricing while still promoting clean-label claims. However, this strategy could potentially alienate purist consumers.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization of culinary oils in mature food markets

- Rapid growth of e-commerce and D2C grocery fulfilment

- Limited certified organic oilseed supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, olive oil held a 33.59% share of the organic edible oil market, reflecting its strong appeal in Mediterranean cuisines and established supply chains in Spain, Italy, and Greece. Avocado oil, the fastest-growing oil type, is projected to expand at a 7.48% CAGR from 2026 to 2031, driven by its heat stability for frying, neutral flavor appealing to non-Mediterranean consumers, and monounsaturated fat profile aligning with ketogenic and paleo diets. Coconut oil remains popular in South and Southeast Asia for traditional cooking and in North America for baking and personal care, though concerns over its saturated fat content limit growth in health-conscious segments. Sunflower, sesame, and almond oils cater to niche culinary and cosmetic markets, with sesame oil particularly strong in Japanese and Korean cuisines. Canola oil, despite its omega-3 benefits, faces challenges from anti-GMO sentiment, as most conventional canola is genetically modified. Organic non-GMO canola oil commands a premium but holds a small market share.

Founded in 2025 in Seville, Spain, the Avocado Oil Manufacturers Association aims to set global quality and sustainability standards for avocado oil and provide access to advanced extraction technologies. This highlights the industry's recognition of avocado oil's potential to rival olive oil in premium markets. In August 2024, Chosen Foods launched a 27-ounce squeeze bottle of 100% pure avocado oil, priced between USD 15.99 and USD 19.99, targeting consumers seeking gluten-free, glyphosate-residue-free, Non-GMO Project certified oils with a 500°F smoke point for high-heat cooking. Olive oil producers are emphasizing polyphenol content, single-estate origins, and early-harvest flavors to differentiate extra virgin olive oil from commodity avocado oil. However, avocado oil's versatility, especially for deep frying, gives it a structural advantage over olive oil.

The Organic Edible Oil Market Report is Segmented by Oil Type (Olive Oil, Coconut Oil, Avocado Oil, Sunflower Oil, Sesame Oil, Almond Oil, Canola Oil, Others), Packaging Type (Bottles, Jars, Cans, Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail Stores, and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Geography Analysis

In 2025, Europe commanded a 37.40% share of the organic edible oil market, bolstered by stringent EU organic labeling, the allure of Mediterranean olive groves, and retailers' preference for premium single-estate SKUs. German and French consumers are pivoting from seed-oil blends to cold-pressed rapeseed variants, further energizing the region's organic edible oil market. While CAP subsidies for organic conversion mitigate farmer risks, water scarcity in Spain and Italy poses challenges to future volume growth. Meanwhile, Eastern Europe's lower land costs are drawing private-equity investments into sunflower and flaxseed conversions, with an eye on meeting Northern Europe's demand peaks by 2029.

Asia-Pacific is set to lead with the highest regional CAGR of 7.58% through 2031, fueled by rising middle-class incomes, urbanization, and heightened food-safety concerns in China, India, and Japan. China's fragmented certification landscape muddies consumer trust, paving the way for blockchain-verified imports from Australia and Canada. Urban millennials in India are increasingly opting for cold-pressed groundnut and sesame oils over refined palmolein, though price disparities hinder rural adoption. Japan's cooking-oil market, on track to hit USD 1.92 billion by 2029 with a 5.2% CAGR, showcases a shift towards premiumization, as shoppers prioritize quality over price, drawn by functional claims, polyphenol content, and smoke-point labeling.

North America stands tall as a consumption titan, with the U.S. leading in organic avocado and olive oil absorption. Canada emerges as a key organic canola supplier to Asia, leveraging CPTPP tariff preferences, though its acreage expansion grapples with climatic uncertainties and certification delays. In South America, Brazil and Argentina are channeling investments into expeller-pressed sunflower and soybean conversions, yet face hurdles in export reliability due to logistics and certification issues. The Middle East witnesses a burgeoning demand in the gourmet retail segments of the UAE and Saudi Arabia; however, wider regional acceptance is stymied by price sensitivities and a nascent cold-chain infrastructure.

- Cargill Incorporated

- CHO GROUP

- Dcoop

- Newman's Own, Inc.

- The Hain Celestial Group, Inc.

- Borges International Group

- Deoleo S.A.

- Nutiva LLC

- La Tourangelle, Inc.

- Chosen Foods LLC

- Grupo DAABON

- California Olive Ranch, Inc.

- Carrington Farms

- Columbus Vegetable Oils

- Kleeschulte GmbH & Co. KG

- Centra Foods

- Clearspring Shop Limited

- Kevala International LLC

- Oil King Foods

- Bernhard Schell GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising health-conscious consumer base shifts to clean-label oils

- 4.2.2 Government incentives expanding certified organic acreage

- 4.2.3 Premiumization of culinary oils in mature food markets

- 4.2.4 Rapid growth of e-commerce and D2C grocery fulfilment

- 4.2.5 Blockchain-enabled traceability boosting consumer trust

- 4.2.6 ESG-driven investment in cold-press and super-critical extraction

- 4.3 Market Restraints

- 4.3.1 High production costs and a premium price

- 4.3.2 Limited certified-organic oilseed supply

- 4.3.3 Competition from conventional oils

- 4.3.4 Fraud/adulteration risk and testing gaps

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Oil Type

- 5.1.1 Olive Oil

- 5.1.2 Coconut Oil

- 5.1.3 Avocado Oil

- 5.1.4 Sunflower Oil

- 5.1.5 Sesame Oil

- 5.1.6 Almond Oil

- 5.1.7 Canola (Rapeseed) Oil

- 5.1.8 Others

- 5.2 Packaging Type

- 5.2.1 Bottles

- 5.2.2 Jars

- 5.2.3 Cans

- 5.2.4 Others

- 5.3 Distribution Channel

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Convenience Stores

- 5.3.3 Specialty Stores

- 5.3.4 Online Retail Stores

- 5.3.5 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Sweden

- 5.4.2.7 Belgium

- 5.4.2.8 Poland

- 5.4.2.9 Netherlands

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Thailand

- 5.4.3.5 Singapore

- 5.4.3.6 Indonesia

- 5.4.3.7 South Korea

- 5.4.3.8 Australia

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Peru

- 5.4.4.5 Chile

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Saudi Arabia

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Cargill Incorporated

- 6.4.2 CHO GROUP

- 6.4.3 Dcoop

- 6.4.4 Newman's Own, Inc.

- 6.4.5 The Hain Celestial Group, Inc.

- 6.4.6 Borges International Group

- 6.4.7 Deoleo S.A.

- 6.4.8 Nutiva LLC

- 6.4.9 La Tourangelle, Inc.

- 6.4.10 Chosen Foods LLC

- 6.4.11 Grupo DAABON

- 6.4.12 California Olive Ranch, Inc.

- 6.4.13 Carrington Farms

- 6.4.14 Columbus Vegetable Oils

- 6.4.15 Kleeschulte GmbH & Co. KG

- 6.4.16 Centra Foods

- 6.4.17 Clearspring Shop Limited

- 6.4.18 Kevala International LLC

- 6.4.19 Oil King Foods

- 6.4.20 Bernhard Schell GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK