PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043958

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043958

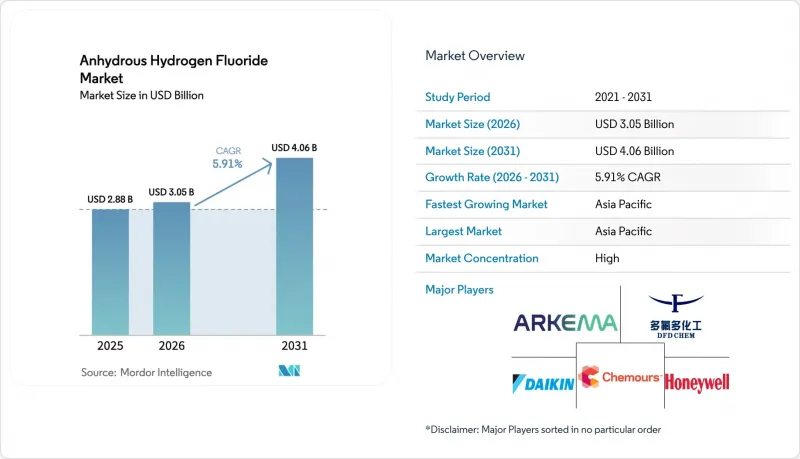

Anhydrous Hydrogen Fluoride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Anhydrous Hydrogen Fluoride Market size is expected to increase from USD 2.88 billion in 2025 to USD 3.05 billion in 2026 and reach USD 4.06 billion by 2031, growing at a CAGR of 5.91% over 2026-2031.

Sustained semiconductor reshoring in the United States, gigafactory build-outs across North America and Europe, and Asia-Pacific's integrated fluorspar-to-fluorochemical ecosystem are reinforcing steady demand even as refrigerant phase-downs reshape legacy consumption patterns. Over the next five years, the anhydrous hydrogen fluoride market will derive incremental volumes from ultra-high-purity grades required for sub-5 nm logic nodes, closed-loop HF recycling from phosphate fertilizer by-products, and specialty fluoropolymers used in electric-vehicle batteries and 5G infrastructure. Supply security is emerging as a decisive competitive factor because 63% of mined fluorspar and more than 70% of global HF capacity remain concentrated in China, amplifying the strategic appeal of backward-integrated operations in Mexico and India. At the same time, refiners upgrading gasoline sulfur specifications and petrochemical producers extending HF alkylation to mixed butylene, propylene feeds are sustaining technical-grade volumes, albeit under tighter safety and regulatory controls.

Global Anhydrous Hydrogen Fluoride Market Trends and Insights

Semiconductor Capacity Build-Out Amplifies Ultra-High-Purity Demand

Domestic-fabrication incentives under the CHIPS and Science Act have triggered more than USD 150 billion of announced wafer-fab spending across Arizona, Texas, and Ohio, yet none of the grants address the secure supply of 12N hydrofluoric acid, the only etchant that volatilizes silicon oxide without metallic residues. South Korea awarded Toyo Engineering Korea an EPC contract in 2025 for a 50,000 tonnes per year HF plant that will diversify sourcing away from Japanese vendors after the 2019 export-control dispute. Stella Chemifa, which already operates 105,000 tonnes of high-purity capacity across Japan and Singapore, is adding North-American production to co-locate near planned fabs, mirroring the broader move to shorten sensitive chemical supply lines. The Semiconductor Industry Association urged USTR in 2026 to harmonize purity standards globally so that contract pricing transparently reflects the cost of achieving sub-ppt impurity thresholds.

Fluoropolymer Expansion for EV Batteries and 5G Infrastructure

Polyvinylidene fluoride volumes are expected to rise, anchored in Li-ion battery binders and separators that consume HF-derived vinylidene fluoride monomer. Arkema allocated USD 20 million to lift PVDF output 15 % at Calvert City, Kentucky, by mid-2026, reinforcing US battery-grade resin self-reliance. Supply tightness is compounded because the Kigali Amendment is squeezing R142b feedstock availability even as the European Union and US regulators accelerate PFAS scrutiny, encouraging producers to shift toward waterborne PVDF dispersions that cut VOCs 90 % without sacrificing performance.

Fluorspar Supply-Chain Concentration and Price Volatility

Geopolitical friction in early 2026 curtailed Strait of Hormuz traffic by more than 90 %, pushing Brent to USD 88.87 per barrel and inflating Chinese HF spot offers by 12 % month-over-month; Zhejiang Juhua and Shandong Dongyue responded with 15-16 % PTFE price hikes in March 2026, the steepest surge since 2024. The episode underscores how single-channel dependence permits rapid pass-through of upstream cost spikes across the fluorine value chain.

Other drivers and restraints analyzed in the detailed report include:

- Alkylation Catalyst Demand Tied to Sulfur Specifications

- Strategic Stockpiling and Critical-Minerals Policies

- Pending PFAS Regulations Dampening Fluorochemical Expansion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technical Grade AHF, at more than or equal to 99.9 wt%, dominated 57.12% of 2025 demand across refrigerants, bulk fluoropolymers, and alkylation catalysts. Yet High-Purity Electronic Grade, specified at more than or equal to 99.999 wt%, is forecast to grow at 6.47% CAGR, propelled by the needs of 3 nm and 2 nm semiconductor nodes where single-digit-part-per-trillion metallic contamination can slash wafer yields. A bifurcated pricing structure lets electronic-grade producers command more than double the margin of commodity suppliers; however, Chinese leaders such as Zhejiang Juhua are commissioning deep-purification modules that could compress premium spreads after 2028.

The anhydrous hydrogen fluoride market benefits as fabs co-locate chemical supply to minimize transit risk; North American projects under evaluation could add 60,000 tons per year of electronic-grade HF by 2030. Even so, permitting complexity and local community scrutiny extends lead times, reinforcing the value of established suppliers with transferable quality-management systems.

The Anhydrous Hydrogen Fluoride Market Report is Segmented by Physical Form and Purity Grade (Technical Grade AHF, High-Purity/ Electronic Grade, and Blended On-Site Generation Solutions), End-User Industry (Fluorochemicals and Refrigerants, Semiconductors and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 60.45% of the Anhydrous Hydrogen Fluoride market size in 2025 and is projected to expand at a 6.22 % CAGR to 2031. China remains the backbone, blending 63% of global fluorspar output with end-to-end HF, LiPF6, and PVDF lines; Zhejiang Juhua's Yumen silicon-fluoride complex, slated for 2026 start-up, will add tens of billions of CNY annual revenue and deepen domestic self-sufficiency. South Korea's Ulsan build, Japan's focus on 12N purity, and India's expansion through Navin Fluorine and Gujarat Fluorochemicals reflect a regional pivot toward capacity resilience after the 2019 Japan-Korea export tensions.

North America's share is poised to rise as semiconductor fabs, battery plants, and PVDF expansions come on-stream. Orbia's Matamoros unit exports nearly all of its 171,000 tons per year output to the United States, leveraging captive ore from San Luis Potosi to shield North-American buyers from Asian shipping delays. Arkema's Kentucky PVDF uplift and Syensqo's Georgia plant underscore a strategic shift toward localizing fluorochemical intermediates that hinge on HF availability.

Europe faces the stiffest regulatory headwinds as PFAS proposals advance under REACH. Producers are therefore investing in waterborne dispersions and closed-loop HF recycling rather than green-field commodity HF lines. Meanwhile the Middle East and Africa, along with South America, remain small yet strategically important because refiners there favor HF alkylation for LPG-rich feed slates, sustaining baseline demand despite environmental opposition elsewhere.

- Arkema

- Buss ChemTech AG

- Daikin Industries, Ltd.

- Do-Fluoride New Materials Co., Ltd. (DFD)

- Fluorsid

- Gujarat Fluorochemicals Ltd. (GFL)

- Honeywell International Inc.

- Jiangsu Meilan Chemical Co., Ltd.

- Merck KGaA

- Morita Chemical Industries Co., Ltd.

- Navin Fluorine International Ltd.

- Orbia Fluor & Energy Materials

- Solvay S.A.

- Stella Chemifa Corporation

- Taiwan Speciality Chemicals Corp

- Tanfac Industries Ltd.

- The Chemours Company

- Zhejiang Juhua Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Semiconductor capacity build-out in Asia and United States

- 4.2.2 Expansion of specialty fluoropolymers in Electric Vehicle and 5G cables

- 4.2.3 Stricter gasoline sulfur specs boosting HF alkylation catalysts

- 4.2.4 Government strategic stockpiling and critical-minerals policies

- 4.2.5 Closed-loop HF recycling from FSA and on-site systems

- 4.3 Market Restraints

- 4.3.1 Fluorspar supply-chain concentration and price shocks

- 4.3.2 Pending PFAS regulations dampening fluorochemical expansion

- 4.3.3 High capex for electronic-grade purification units

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Physical Form and Purity Grade

- 5.1.1 Technical Grade AHF (>=99.9 wt %)

- 5.1.2 High-Purity / Electronic Grade (>=99.999 wt %)

- 5.1.3 Blended On-site Generation Solutions

- 5.2 By End-user Industry

- 5.2.1 Fluorochemicals and Refrigerants

- 5.2.2 Semiconductors and Electronics

- 5.2.3 Mineral Processing and Metal Treatment

- 5.2.4 Petroleum Alkylation Catalysts

- 5.2.5 Glass Cleaning and Etching

- 5.2.6 Other Industrial Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 South Korea

- 5.3.1.4 India

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Buss ChemTech AG

- 6.4.3 Daikin Industries, Ltd.

- 6.4.4 Do-Fluoride New Materials Co., Ltd. (DFD)

- 6.4.5 Fluorsid

- 6.4.6 Gujarat Fluorochemicals Ltd. (GFL)

- 6.4.7 Honeywell International Inc.

- 6.4.8 Jiangsu Meilan Chemical Co., Ltd.

- 6.4.9 Merck KGaA

- 6.4.10 Morita Chemical Industries Co., Ltd.

- 6.4.11 Navin Fluorine International Ltd.

- 6.4.12 Orbia Fluor & Energy Materials

- 6.4.13 Solvay S.A.

- 6.4.14 Stella Chemifa Corporation

- 6.4.15 Taiwan Speciality Chemicals Corp

- 6.4.16 Tanfac Industries Ltd.

- 6.4.17 The Chemours Company

- 6.4.18 Zhejiang Juhua Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs