PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043960

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043960

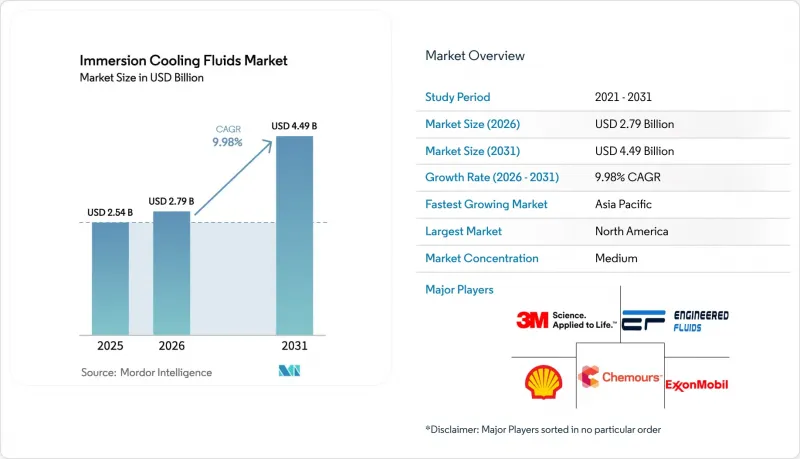

Immersion Cooling Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Immersion Cooling Fluids Market size is projected to expand from USD 2.54 billion in 2025 and USD 2.79 billion in 2026 to USD 4.49 billion by 2031, registering a CAGR of 9.98% between 2026 and 2031. Growing rack densities that exceed 30 kilowatts, hyperscale operators' shift toward AI clusters above 400 MW per campus, and district-heating programs that monetize waste heat are redefining data-center economics. Regulatory deadlines phasing out PFAS compounds in North America and Europe are steering buyers toward PFAS-free synthetics and esters, while Intel's 2025 certification of Shell and ExxonMobil fluids removed a key hurdle for hyperscale adoption. As a result, single-phase systems priced at USD 2-5 per liter for mineral oils dominate installed capacity, yet fluorinated alternatives, now PFAS-free, are the fastest-growing chemistry. Competitive intensity remains high because no vendor holds more than 12% share, but suppliers that combine refining scale with chip-maker endorsements are consolidating influence.

Global Immersion Cooling Fluids Market Trends and Insights

Rising Energy-Efficiency and PUE Optimization Pressures

Operators pushing PUE below 1.15 face steep air-cooling penalties once rack densities top 30 kW. Single-phase immersion reduces fan and chiller loads, delivering a PUE of 1.05-1.15, while two-phase achieves 1.02-1.08. Microsoft's fleetwide rollout of direct liquid cooling in July 2025 and Colovore's USD 925 million financing for 200 kW-per-rack capacity mark a shift from pilot to baseline engineering. Dell'Oro Group recorded 85% year-over-year liquid-cooling growth in 2025, although immersion still trails direct-to-chip retrofits. The European Data Centre Association measured only 5.6% immersion adoption in 2024, underscoring a five-to-ten-year conversion window. Intel-Shell tests confirmed up to 48% energy savings, 30% CO2 reduction, and 99% lower water use, aligning with corporate science-based targets.

Sustainability and Carbon-Neutral Targets Accelerate Adoption

District-heating programs price delivered heat at EUR 12-22 per MWh, undercutting gas boilers by roughly 50%. AWS Tallaght supplied 92% of Trinity College Dublin's heating and cut 704 tons of CO2 in 2024, proving revenue-positive heat export. Microsoft-Fortum's Finland scheme will reach 250,000 residents by 2026. Singapore's moratorium lift now mandates PUE less than 1.3 and renewable sourcing, stimulating liquid cooling at STT GDC. Meta's USD 65 billion AI build and Google's USD 40 billion Texas plan both specify liquid cooling, giving colocation operators pricing power premiums of 20-40% per kilowatt.

Material Compatibility and Safety Concerns Amid PFAS Regulation

Hydrocarbon coolants can attack certain elastomers, forcing component-by-component validation. Cargill FR3 is biodegradable but creates hotter spots, potentially shortening lifecycle in tight-margin designs. Two-phase tanks demand hermetic sealing; micro-leaks slash performance and raise fire risk when fluids are flammable. Absent long-term field data, Shell and ExxonMobil only cleared Intel tests in 2025; risk-averse BFSI users defer conversion. Divergent EU and U.S. rules oblige region-specific blends, inflating SKUs and cost.

Other drivers and restraints analyzed in the detailed report include:

- Stricter PFAS-Phase-Out Deadlines Reshape Fluid Chemistries

- Growing Edge-Micro-Data-Centers in Untapped Emerging Markets

- Limited Standards / Inter-Operability Across OEM Ecosystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic hydrocarbons captured 37.12% of the Immersion Cooling Fluids market share in 2025, buoyed by Intel's endorsement of Shell and ExxonMobil formulas. Fluorinated fluids, relaunched as PFAS-free hydrofluoroethers by Chemours, Solvay, and DOW, are forecast for a 10.22% CAGR during the forecast period (2026-2031). Mineral oils keep crypto miners loyal thanks to USD 2-5 per-liter pricing and 6-12 month paybacks, while natural-ester blends meet IEC 62770 yet run hotter, curbing HPC uptake. Engineered suppliers such as Dynalene and Engineered Fluids fill customization gaps at premium margins.

Single-phase accounted for 64.44% of the Immersion Cooling Fluids market size in 2025 and should grow at a 10.36% CAGR, reflecting their lower capital cost (no hermetic sealing required), simpler fluid management (no evaporation control), and compatibility with district-heating networks that accept 50-60°C inlet temperatures. Two-phase remains essential for racks above 100 kW, demonstrated by Accelsius pipelines and DarkNX's 300 MW Ontario campus hitting PUE 1.02-1.08. However, hermetic design complexity and refrigerant management keep the two-phase adoption niche today.

The Immersion Cooling Fluids Market Report is Segmented by Fluid Type (Synthetic Hydrocarbon Oils, and More), Cooling Type (Single-Phase Immersion Cooling and More), Application (Data Centers - Hyperscale, and More), End-User Industry (IT and Telecom, BFSI, and Mores), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 41.18% of 2025 revenue owing to Meta's USD 65 billion AI build and Google's USD 40 billion Texas project. Asia-Pacific shows a 10.45% forecast CAGR, catalyzed by Singapore's green-data-center rules, Japan's 9.6% market CAGR, and India's 200 kW-rack deployments. Europe monetizes waste heat, AWS Tallaght cut 704 tons of CO2 in 2024, and Microsoft-Fortum will heat 250,000 Finns by 2026, creating 15-25% better ROI for operators. Latin America and the Middle East record double-digit growth but struggle with hazmat regulations and skills shortages, slowing immersion ramp.

List of Companies Covered in this Report:

- 3M

- AGC Inc.

- Cargill

- Castrol Limited (BP)

- Chevron Oronite

- DOW

- Dynalene Inc.

- Engineered Fluids

- ExxonMobil Corporation

- FUCHS

- Lubrizol

- M&I Materials Ltd

- Shell plc

- Solvay

- The Chemours Company

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising energy-efficiency and PUE optimization pressures

- 4.2.2 Sustainability and carbon-neutral targets accelerate adoption

- 4.2.3 Stricter PFAS-phase-out deadlines reshape fluid chemistries

- 4.2.4 Growing edge-micro-data-centers in untapped emerging markets

- 4.2.5 Heat-to-heat-re-use initiatives driving district-heating integration

- 4.3 Market Restraints

- 4.3.1 Material compatibility and safety concerns amid PFAS regulation

- 4.3.2 Limited standards/inter-operability across OEM ecosystems

- 4.3.3 Volatility in synthetic base-oil supply chain post-3M exit

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fluid Type

- 5.1.1 Synthetic Hydrocarbon Oils

- 5.1.2 Mineral Oils

- 5.1.3 Fluorinated Fluids

- 5.1.4 Esters / Bio-based and Biodegradable Fluids

- 5.1.5 Other Fluid Types

- 5.2 By Cooling Type

- 5.2.1 Single-phase Immersion Cooling

- 5.2.2 Two-phase Immersion Cooling

- 5.3 By Application

- 5.3.1 Data Centers - Hyperscale

- 5.3.2 Data Centers - Colocation

- 5.3.3 Data Centers - Enterprise

- 5.3.4 Crypto-mining/Blockchain

- 5.3.5 HPC and AI Training Clusters

- 5.3.6 Power Electronics and Industrial Computing

- 5.3.7 EV Fast-charging and Battery Thermal Management

- 5.3.8 Other Applications

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Manufacturing and Industrial

- 5.4.4 Energy and Utilities

- 5.4.5 Automotive and Transportation

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 Singapore

- 5.5.1.5 South Korea

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Cargill

- 6.4.4 Castrol Limited (BP)

- 6.4.5 Chevron Oronite

- 6.4.6 DOW

- 6.4.7 Dynalene Inc.

- 6.4.8 Engineered Fluids

- 6.4.9 ExxonMobil Corporation

- 6.4.10 FUCHS

- 6.4.11 Lubrizol

- 6.4.12 M&I Materials Ltd

- 6.4.13 Shell plc

- 6.4.14 Solvay

- 6.4.15 The Chemours Company

- 6.4.16 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs