PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043969

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043969

Rolling Stock Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

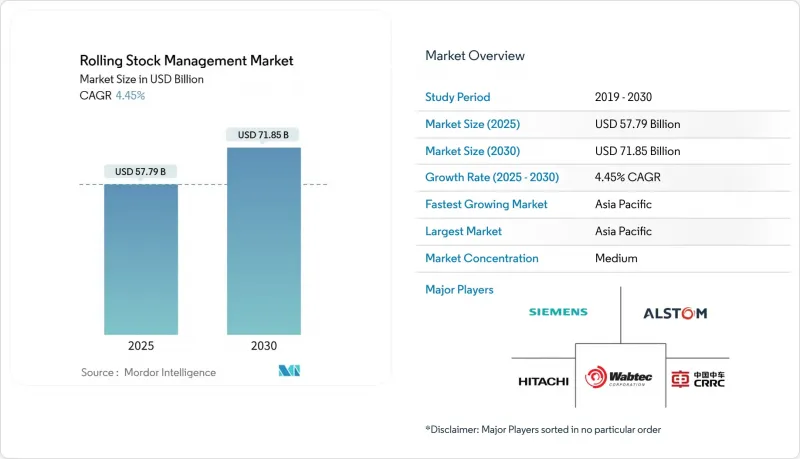

The rolling stock management market size stands at USD 57.79 billion in 2025 and is projected to reach USD 71.85 billion by 2030, reflecting a 4.45% CAGR over the forecast period.

The growth trajectory signals a methodical but irreversible shift toward digital rail operations, underpinned by rising investments in sensor networks, fleet-wide analytics, and software-defined maintenance platforms. Government modernization programs, adoption of predictive maintenance, and the expansion of high-density freight and passenger corridors continue to widen the addressable base for integrated lifecycle solutions. Vendors capable of delivering scalable, safety-certified platforms that tie rolling stock, infrastructure, and crew operations into one data fabric are positioned to capture long-term contracts as operators align technology choices with regulatory mandates. Cyber-secure, standards-compliant architectures, edge analytics, and digital-twin workflows emerge as core differentiators, while multi-vendor procurement remains the dominant strategy to avoid supply-chain lock-in.

Global Rolling Stock Management Market Trends and Insights

Predictive Maintenance and IoT Adoption

Operators are replacing calendar-based inspections with condition-based programs that leverage sensor arrays and onboard edge computing to detect anomalies in real time. Network Rail reported a gain of 100 additional high-speed train operating days annually after deploying wheelset monitoring, directly linking analytics to revenue. Component-level sensors now track more than 200 parameters per locomotive, producing terabytes of data each month. Lower sensor costs and increased on-train processing power remove economic barriers to fleet-wide instrumentation. Prognostic algorithms forecast failures weeks in advance, cutting emergency repairs and boosting punctuality. Vendors that embed AI models inside train-borne gateways minimize latency and support the 99.9% uptime demanded by safety regulators.

Heavy Government Investment in Rail Modernization

Public spending accelerates digitization. The U.S. Department of Transportation obligated USD 2.4 billion for rail upgrades in 2024 . The Korean National Railway established a digital rail IT center to unify data flows across urban and intercity lines. China's Belt and Road Initiative has earmarked over USD 60 billion for trans-Asian railways, each requiring interoperable management systems. In Europe, mandatory ETCS Level 2 rollouts by 2030 push operators to retrofit locomotives at EUR 2-4 million each. Authorities increasingly tie funding to integrated digital solutions that prove life-cycle value over isolated hardware buys.

High Upfront CAPEX for Digital Systems

Network Rail's eight-year on-track machine package underscores the capital intensity. Smaller lines with under 50 vehicles struggle to finance enterprise-grade platforms that show 7-10 year payback periods. Integration with legacy ERP, signaling, and reporting tools typically doubles software license costs, creating budgeting uncertainty. Financial institutions remain cautious, citing thin residual value data for digital assets.

Other drivers and restraints analyzed in the detailed report include:

- Rising Freight and Passenger-km Demand

- Safety-Driven Regulatory Mandates

- Cyber-security and Data-privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rail management held 62.15% of the rolling stock management market share in 2024, indicating operator emphasis on locomotive and coach performance optimization. Infrastructure management, although smaller, is moving ahead at a 4.88% CAGR as track, signaling, and power conditions prove inseparable from fleet health. Integrated dashboards now synthesize propulsion data, brake wear, and ride quality to advise consist formation and routing. The widening adoption of cloud-connected devices inside depots supports near-real-time decision-making, shrinking mean-time-to-repair across entire fleets.

Operators that initially digitized high-value assets are increasingly extending capabilities to wayside systems. Railigent X merges onboard diagnostics with track geometry analytics, giving planners one screen to align maintenance windows, resource allocation, and service timetables. The convergence unlocks incremental uptime improvements that compound into material revenue gains over multiyear horizons.

Preventive programs retained a 48.36% share of the rolling stock management market size in 2024 because regulatory calendars still prescribe minimum inspection cycles. Predictive maintenance registers the fastest 7.05% CAGR, as condition-based strategies consistently cut unscheduled downtime by up to 40%. Union Pacific's models reschedule component change-outs exactly before failure, trimming inventory and labor cost while preserving safety. Operators increasingly earn regulatory waivers to extend service intervals when backed by certified sensors and data science workflows, reinforcing the shift.

Digital twins amplify the value proposition by allowing simulation of maintenance policies across a virtual fleet. Cost-of-delay metrics and component stress curves guide budget allocation, turning maintenance from a fixed overhead into a variable cost aligned with demand patterns. Corrective maintenance, therefore, shrinks as a fraction of total spending, though it remains essential for rare catastrophic failures.

The Rolling Stock Management Market Report is Segmented by Management Type (Rail Management and Infrastructure Management), Maintenance Service (Corrective Maintenance, Preventive Maintenance, and More), Application (Passenger Transport and Freight Transport), Rolling Stock Type (Locomotives and More), End User (Railway Operators and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific claimed 55.33% of the rolling stock management market in 2024 and is on track for a 6.15% CAGR to 2030. China's USD 60 billion Belt and Road rail investments embed interoperable management standards across trans-Asian networks. India's fleet digitization agenda prioritizes predictive maintenance to cut unit operating cost on one of the world's busiest networks. Southeast Asian high-speed corridors bring greenfield deployments that skip legacy steps and adopt cloud-native platforms from day one.

North America represents a mature but opportunity-rich landscape. The commitment by the U.S. Department of Transportation funds freight reliability and passenger punctuality programs that hinge on advanced fleet analytics. Class I freight railroads allocate capital toward edge-compute gateways, integrating Positive Train Control data into broader asset-health ecosystems. Canadian carriers follow suit, investing in winter-resilient sensor suites.

Europe concentrates on ETCS Level 2 conformity and cross-border harmonization. Network Rail's EUR 1.1 billion (~USD 1.3 billion) machinery package exemplifies large-scale fleet digitization in a traditionally infrastructure-centric environment. Funding instruments such as the EU Connecting Europe Facility steer grants toward interoperability demonstrators and cybersecurity-enhanced platforms. The Middle East and Africa, along with South America, contribute smaller shares yet outpace global averages in growth as mining, port, and urban mobility projects introduce modern fleets that mandate digital oversight. Development banks tie financing to adoption of certified management systems, accelerating technology diffusion into nascent rail markets.

- Siemens Mobility

- Alstom S.A.

- Hitachi Rail

- Wabtec Corporation

- CRRC Corporation Limited

- CAF Group

- Stadler Rail AG

- Progress Rail (EMD)

- ABB Rail Solutions

- Mitsubishi Heavy Industries

- Talgo S.A.

- Trinity Rail Maintenance Services

- The Greenbrier Companies

- Trimble Inc.

- Cisco Systems

- Huawei Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Predictive Maintenance and IoT Adoption

- 4.2.2 Heavy Government Investment in Rail Modernization

- 4.2.3 Rising Freight and Passenger-km Demand

- 4.2.4 Safety-Driven Regulatory Mandates

- 4.2.5 Rail-as-a-Service Subscription Models

- 4.2.6 Digital-Twin Lifecycle Optimization

- 4.3 Market Restraints

- 4.3.1 High Upfront CAPEX for Digital Systems

- 4.3.2 Cyber-security and Data-privacy Concerns

- 4.3.3 Skilled Analytics-Talent Shortage

- 4.3.4 Legacy Interoperability in Multi-operator Corridors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Management Type

- 5.1.1 Rail Management

- 5.1.2 Infrastructure Management

- 5.2 By Maintenance Service

- 5.2.1 Corrective Maintenance

- 5.2.2 Preventive Maintenance

- 5.2.3 Predictive Maintenance

- 5.3 By Application

- 5.3.1 Passenger Transport

- 5.3.2 Freight Transport

- 5.4 By Rolling Stock Type

- 5.4.1 Locomotives

- 5.4.2 Passenger Coaches

- 5.4.3 Freight Cars

- 5.4.4 Specialized Vehicles

- 5.5 By End User

- 5.5.1 Railway Operators

- 5.5.2 Logistics Companies

- 5.5.3 Public Transportation Authorities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 Spain

- 5.6.3.4 Italy

- 5.6.3.5 France

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Siemens Mobility

- 6.4.2 Alstom S.A.

- 6.4.3 Hitachi Rail

- 6.4.4 Wabtec Corporation

- 6.4.5 CRRC Corporation Limited

- 6.4.6 CAF Group

- 6.4.7 Stadler Rail AG

- 6.4.8 Progress Rail (EMD)

- 6.4.9 ABB Rail Solutions

- 6.4.10 Mitsubishi Heavy Industries

- 6.4.11 Talgo S.A.

- 6.4.12 Trinity Rail Maintenance Services

- 6.4.13 The Greenbrier Companies

- 6.4.14 Trimble Inc.

- 6.4.15 Cisco Systems

- 6.4.16 Huawei Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment