PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043973

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043973

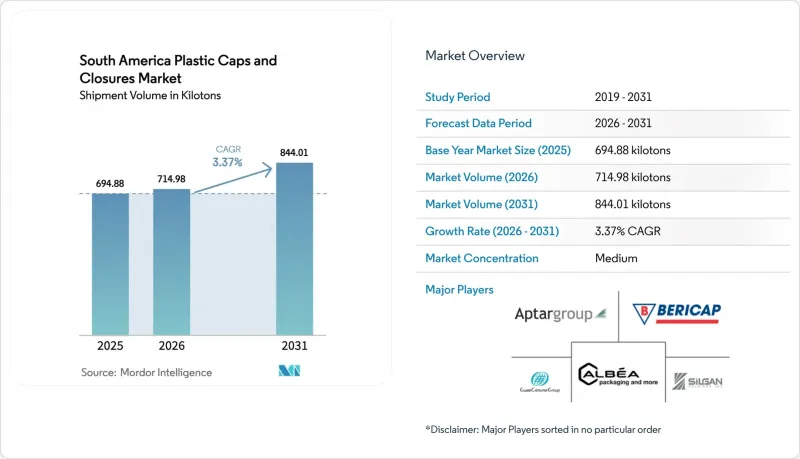

South America Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America plastic caps and closures market size was valued at 694.88 kilotons in 2025 and estimated to grow from 714.98 kilotons in 2026 to reach 844.01 kilotons by 2031, at a CAGR of 3.37% during the forecast period (2026-2031).

Favorable recycled-content mandates, the rapid uptick in e-commerce fulfillment, and exporter alignment with the European Union tethered-cap rule are redefining product specifications and sourcing strategies. Regional resin producer Braskem has accelerated the shift toward mechanically and chemically recycled grades, while premium personal-care and spirits brands are installing smart closures that validate authenticity at the point of consumption. Converters able to blend virgin and post-consumer resin, integrate tamper-evident functionality, and offer short print runs for promotional campaigns are winning new contracts. At the same time, closure lightweighting is becoming a cost-of-entry requirement as brand owners pursue carbon-reduction targets and seek relief from volatile polypropylene prices.

South America Plastic Caps And Closures Market Trends and Insights

Surging On-The-Go Beverage Consumption

Urban commuters are favoring single-serve PET bottles that can be consumed on the move, pushing brands to specify closures that maintain carbonation, resist leakage, and open smoothly. Retail data show soft-drink and energy-drink volumes rising in Brazil and Colombia, and sports-drink lines are adopting flip-top and push-pull designs that enable one-handed use. Converters are responding with tamper-evident bands, pressure-relief vents, and stronger hinge designs that add up to 8% to unit cost yet reduce shrinkage for retailers. Investment in high-cavity compression molds supports the volume surge, while lightweighting offsets part of the added feature cost. The net effect is a positive mix shift toward value-added closures that lift average selling prices.

Rising Penetration of PET Bottled Dairy Drinks

Dairy processors in Brazil and Argentina are switching from cartons to chilled PET bottles, driving demand for closures that protect flavor and signal premium positioning. Sugarcane-based tethered caps introduced by Tetra Pak demonstrate that bio-attributed materials can meet both sustainability targets and performance needs. Dual-seal designs combining foil liners with tamper rings are gaining traction, though their co-injection tooling requirements limit production to larger converters. Cold-chain expansion in Peru and Colombia will unlock additional volume once infrastructure matures, making PET dairy drinks a key long-term growth pocket. Closure makers able to co-mold dissimilar resins and manage small color runs hold a strategic edge.

Shift Toward Stand-Up Pouches In Household Cleaners

Flexible refill pouches now dominate detergent and fabric-softener aisles in Brazil and Chile, reducing demand for rigid-bottle closures. Unilever's South America revenue rose 6.0% in 2024, helped by pouch formats that weigh 70% less and sell at a lower cost-per-use. Closure suppliers are exploring spouted pouches with flip-tops, yet the subformat still accounts for less than 5% of flexible-pack volume. As concentrated pods gain traction, closures could lose further relevance unless converters pivot to dispensing heads for refill stations or design resealable spouts compatible with film laminates.

Other drivers and restraints analyzed in the detailed report include:

- Booming E-Commerce Demand For Tamper-Evident Packaging

- Private-Label Expansion Among Regional FMCG Players

- Growing Anti-Plastic Regulations In Pacific Alliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Other Materials, mainly recycled PET, bio-based polyethylene, and advanced bioplastics, are forecast to outpace the overall South America plastic caps and closures market at a 4.33% CAGR, benefiting from Brazil's 22% mandatory recycled content in PET packaging beginning in 2026. Polypropylene retained 44.20% volume share in 2025, but volatile offer prices at USD 840 per tonne have prompted converters to blend in 20-30% post-consumer resin, safeguarding margins while meeting client sustainability commitments.

Braskem's FDA-compliant PCR PP launched in June 2025 removed the last technical barrier to using recycled PP in food-contact closures. Meanwhile, bio-attributed sugarcane PE qualifies for Bonsucro certification and cuts life-cycle carbon emissions by 70%. Limited food-grade rPET capacity in Peru and Colombia, however, constrains PET closure growth. Across the region, converters now qualify four resin streams, virgin, mechanically recycled, chemically recycled, and bio-based, raising inventory costs yet providing supply resilience..

Beverage closures delivered 49.32% of volume in 2025 thanks to Ambev's breweries and Coca-Cola FEMSA's bottling footprint. Even so, cosmetics and toiletries closures will grow faster at 4.52% CAGR as premium skincare and hair-care lines adopt soft-squeeze and airless pumps that improve dosing precision. The South America plastic caps and closures market size for cosmetics commands higher average selling prices, offsetting lower tonnage.

Food closures advance in lockstep with rising per-capita income, while household-chemical closures suffer from refill pouches. Pharmaceutical and healthcare remain niche but highly profitable because of child-resistant and desiccant-integrated features demanded by ANVISA and ANMAT. Brand owners in Chile and Brazil, markets with stricter quality regulation, already pay 3-5 times the price of commodity screw caps for these advanced formats.

The South America Plastic Caps and Closures Market Report is Segmented by Material (PET, PP, LDPE, and More), End-User Industry (Beverage, Food, and More), Cap Type (Screw Closures, Tethered Caps, Child-Resistant Closures, and More), Manufacturing Technology (Injection Molding, Compression Molding, and More), and Geography (Brazil, Argentina, Colombia, and More). The Market Forecasts are Provided in Terms of Volume (Kilotons).

List of Companies Covered in this Report:

- Silgan Holdings Inc.

- Albea S.A.

- Guala Closures S.p.A.

- Bericap GmbH & Co. KG

- AptarGroup, Inc.

- Amcor plc

- Crown Holdings, Inc.

- Closure Systems International, Inc.

- Plastivaloire SE

- Tecnocap S.p.A.

- Pano Cap (Canada) Limited

- Mold-Tek Packaging Limited

- RPC M&H Plastics Ltd.

- Oben Holding Group S.A.C.

- Universal Closures Ltd.

- Paccor Packaging GmbH

- Weener Plastics Group BV

- Freudenberg Home and Cleaning Solutions GmbH

- Comar, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging On-The-Go Beverage Consumption

- 4.2.2 Rising Penetration Of Pet Bottled Dairy Drinks

- 4.2.3 Booming E-Commerce Demand For Tamper-Evident Packaging

- 4.2.4 Private-Label Expansion Among Regional Fmcg Players

- 4.2.5 Refill-And-Reuse Pilots By Large Beverage Brands

- 4.2.6 Adoption Of Tethered-Cap Eu Directive By Sa Exporters

- 4.3 Market Restraints

- 4.3.1 Shift Toward Stand-Up Pouches In Household Cleaners

- 4.3.2 Growing Anti-Plastic Regulations In Pacific Alliance

- 4.3.3 Price Volatility Of Virgin Polypropylene

- 4.3.4 Consumer Preference For Metal Crowns In Premium Beer

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 The Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Material

- 5.1.1 Polyethylene Terephthalate (PET)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Low Density Polyethylene (LDPE)

- 5.1.4 High-Density Polyethylene (HDPE)

- 5.1.5 Other Materials

- 5.2 By End-user Industry

- 5.2.1 Beverage

- 5.2.2 Food

- 5.2.3 Pharmaceutical and Healthcare

- 5.2.4 Cosmetics and Toiletries

- 5.2.5 Household Chemicals

- 5.2.6 Other End-user Industries

- 5.3 By Cap Type

- 5.3.1 Screw Closures

- 5.3.2 Tethered Caps

- 5.3.3 Flip-top and Snap-on Caps

- 5.3.4 Child-resistant Closures

- 5.3.5 Luxury/Premium Decorative Closures

- 5.3.6 Dispensing Caps

- 5.4 By Manufacturing Technology

- 5.4.1 Injection Molding

- 5.4.2 Compression Molding

- 5.4.3 3-Piece and In-line Assembly

- 5.4.4 Digitally Printed Smart Closures

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Silgan Holdings Inc.

- 6.4.2 Albea S.A.

- 6.4.3 Guala Closures S.p.A.

- 6.4.4 Bericap GmbH & Co. KG

- 6.4.5 AptarGroup, Inc.

- 6.4.6 Amcor plc

- 6.4.7 Crown Holdings, Inc.

- 6.4.8 Closure Systems International, Inc.

- 6.4.9 Plastivaloire SE

- 6.4.10 Tecnocap S.p.A.

- 6.4.11 Pano Cap (Canada) Limited

- 6.4.12 Mold-Tek Packaging Limited

- 6.4.13 RPC M&H Plastics Ltd.

- 6.4.14 Oben Holding Group S.A.C.

- 6.4.15 Universal Closures Ltd.

- 6.4.16 Paccor Packaging GmbH

- 6.4.17 Weener Plastics Group BV

- 6.4.18 Freudenberg Home and Cleaning Solutions GmbH

- 6.4.19 Comar, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment