PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043981

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043981

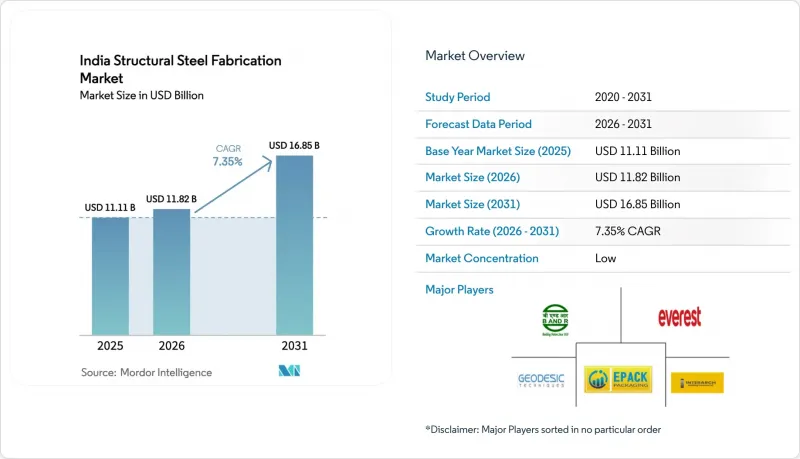

India Structural Steel Fabrication - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The India Structural Steel Fabrication Market size is expected to increase from USD 11.11 billion in 2025 to USD 11.82 billion in 2026 and reach USD 16.85 billion by 2031, growing at a CAGR of 7.35% over 2026-2031.

Sustained federal spending through the USD 1.4 trillion National Infrastructure Pipeline and the cross-sector PM Gati Shakti program has turned what were once episodic construction bursts into a predictable multiyear order book, ensuring steady tonnage off-take from fabricators. Demand is also widening beyond commodity beams; data center campuses, green hydrogen electrolyser plants, and offshore wind monopiles are driving a shift toward custom plate-worked assemblies that command price premiums but require greater engineering capability. At the same time, automation is moving from aspiration to necessity: CNC laser, plasma, and water-jet lines are replacing manual cutting to meet hyperscale developers' tolerance targets and shorten project cycles. These forces together underpin the 7.35% growth outlook for the India structural steel fabrication market.

India Structural Steel Fabrication Market Trends and Insights

Multiyear Rail, Road, Airport, Port Capex Under NIP/PM Gati Shakti

Budget 2025-26 earmarked USD 134 billion for infrastructure, locking in demand for bridges, viaducts, and terminal roofs through 2031. The Eastern and Western Dedicated Freight Corridors alone need more than 2 million tonnes of fabricated steel for bridges and gantries, with completion timelines stretching to 2028. Metro additions across seven metros add 400-500 route-km, each km requiring 1,200-1,500 tonnes of steel. Sagarmala's port upgrades and airport modernizations further widen the order funnel but impose liquidated-damages clauses that penalize schedule lapses, raising the premium on just-in-time delivery and automated inspection.

Warehousing and Industrial PEB Surge into Tier II/III Cities

The National Logistics Policy aims to cut logistics cost to below 10% of GDP by 2030, sparking a warehouse boom that absorbed 58 million ft2 of Grade A capacity during 2024, 42% of which rose in Tier II/III locations. Pre-engineered buildings (PEBs) dominate these projects because standardized portal frames allow a 100,000 ft2 hub to go live in 120 days versus 180-plus days for concrete. PM Gati Shakti's single digital window has trimmed statutory clearances by 10 months, compressing developers' working-capital cycles. For fabricators, a single multimodal park can lock in 8,000-12,000 tonnes across warehouses, truck terminals, and cold storage, but tight reverse-auction pricing keeps EBITDA margins in the mid-single digits. Transporting 12-meter members from coastal yards to inland sites adds 8-12% to delivered costs, nudging larger fabricators to open satellite welding yards near demand centers.

Imported Coking-Coal Dependence and Price Volatility Inflating Input Costs

In 2024-2025, spot prices for coking coal, which India imports 85% of, fluctuated between USD 350 and USD 425 per tonne, primarily due to logistical challenges at Queensland mines. A 10% rise in hot-rolled coil prices typically results in a 4-6% increase in related prices. However, public-sector and PEB contracts seldom permit mid-cycle price adjustments. While large yards mitigate risks through inventory management or swap contracts, over 60% of MSME shops faced negative cash flow in 2024, as steel prices surged beyond their bid buffers. Integrated producers, like Tata Steel's Australian JV, benefit from a 7-10% cost advantage due to their captive mine stakes, putting pressure on standalone fabricators to either forward-buy or face margin erosion.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center Campus Build-Out to 1.8 GW IT Capacity

- Renewable Tenders Expanding BOS Steel Needs

- Persistent Welder/Detailer Scarcity and Slow Upskilling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heavy sections such as W-beams and H-columns captured 40.68% of the India structural steel fabrication market share in 2025, mirroring their ubiquity in multi-story offices, industrial sheds, and metro viaducts. Commodity profiles enjoy mill-direct pricing and standardized design tables, enabling fast quoting and high throughput. Yet commodity tonnage offers thin margins, so top-tier fabricators funnel earnings into engineering software and submerged-arc welding lines to chase higher-value plate-worked girders and modular skids. The fastest-growing custom module segment is projected to expand at an 8.73% CAGR from 2026-2031, as data center, hydrogen, and offshore wind developers demand bespoke assemblies pre-integrated with electrical and mechanical systems.

The India structural steel fabrication market for custom plate-worked products is rising significantly, driven by these specialized needs. Plate girders for long-span bridges, for example, require UT-tested full-penetration welds and third-party inspection under AWS D1.5; only 20-25 Indian yards presently carry this accreditation. Fabricators that pair BIM-driven detailing with off-site modular assembly cut on-site labor by 40-50%, meet EPC schedules, and carve a defensible niche above commodity players.

The India Structural Steel Fabrication Market Report is Segmented by Product Type (Heavy Section, Light Sectional & Cold-Formed Members, and More), by End-User Industry (Construction, Power & Energy, and More), by Fabrication Process (Cutting, Bending, Welding, and More), and by Geography (North India, West India, South India, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Bridge & Roof Co. (India) Ltd.

- EPACK Prefab Technologies

- Everest Industries (Steel Buildings)

- Geodesic Techniques

- Interarch Building Solutions

- JSW Severfield Structures (JSSL)

- Kalpataru Projects International (Towers/Structures)

- KEC International (Towers/Structures)

- Kirby Building Systems & Structures India

- Larsen & Toubro Construction

- Maurer Sanfield India

- Onshore Construction Company

- Pennar Industries (PEB/Structures)

- Phenix Construction Technologies (M&B Engineering)

- Satec EnvirEngineering (India)

- Sharp Tanks & Structurals

- SKV Engineering India Pvt. Ltd.

- Spacechem Group (Spacechem Engineers)

- Tata BlueScope Building Solutions (BUTLER)

- Tata Projects

- TJSV Steel Fabrication & Galvanizing

- Zamil Steel Buildings India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Warehousing and industrial PEB surge into Tier II/III under National Logistics Policy and PM Gati Shakti

- 4.2.2 Data center campus build-out to 1.8 GW capacity by 2027 driving heavy steel shells and long-span floors

- 4.2.3 Renewable tenders (solar/wind/BESS) expanding BOS steel needs across mounting, yards, and substations

- 4.2.4 Multi-year rail/road/airport/port capex under NIP/PM Gati Shakti sustaining bridge, terminal, and metro steel

- 4.2.5 Green Hydrogen Mission (SIGHT, low-carbon steel pilots) catalyzing electrolyser and ammonia plant structures

- 4.2.6 Offshore wind and port modernization kick-offs requiring complex marine steel fabrication

- 4.3 Market Restraints

- 4.3.1 Imported coking coal dependence and price volatility inflating input costs and buffers

- 4.3.2 Persistent welder/detailer scarcity and slow upskilling at MSME clusters

- 4.3.3 Elongated receivables cycles and bid-driven margin pressure for MSME fabricators

- 4.3.4 Tender/PSA slippages and undersubscription in renewables delaying steel-intensive projects

- 4.4 Value-Chain / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter?s Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Values, In USD Billion)

- 5.1 By Product Type

- 5.1.1 Heavy Section(Beams & Columns)

- 5.1.2 Light Sectional & Cold-Formed Members

- 5.1.3 Tubular & Hollow Structural Sections (HSS)

- 5.1.4 Other Product Types(Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.)

- 5.2 By End-user Industry

- 5.2.1 Construction

- 5.2.1.1 Commercial

- 5.2.1.2 Residential

- 5.2.1.3 Industrial Buildings

- 5.2.1.4 Infrasructure(Transport)

- 5.2.2 Power & Energy (include utilities and renewable energy)

- 5.2.3 Manufacturing & Industrial Equipment

- 5.2.4 Oil and Gas

- 5.2.5 Automotive & Transportation (railways systems, metro components, etc.)

- 5.2.6 Other End User Industries(Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications)

- 5.2.1 Construction

- 5.3 By Fabrication Process

- 5.3.1 Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.)

- 5.3.2 Bending (Press brakes, roll bending, rotary bending)

- 5.3.3 Welding (TIG, MIG, arc welding, spot welding)

- 5.3.4 Machining (Milling, turning, drilling, grinding, CNC machining)

- 5.3.5 Forming (Stamping, forging, rolling, hydroforming)

- 5.3.6 Casting (Sand casting, die casting, investment casting)

- 5.3.7 Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.)

- 5.4 By Geography

- 5.4.1 North India

- 5.4.2 West India

- 5.4.3 South India

- 5.4.4 East & North-East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Bridge & Roof Co. (India) Ltd.

- 6.4.2 EPACK Prefab Technologies

- 6.4.3 Everest Industries (Steel Buildings)

- 6.4.4 Geodesic Techniques

- 6.4.5 Interarch Building Solutions

- 6.4.6 JSW Severfield Structures (JSSL)

- 6.4.7 Kalpataru Projects International (Towers/Structures)

- 6.4.8 KEC International (Towers/Structures)

- 6.4.9 Kirby Building Systems & Structures India

- 6.4.10 Larsen & Toubro Construction

- 6.4.11 Maurer Sanfield India

- 6.4.12 Onshore Construction Company

- 6.4.13 Pennar Industries (PEB/Structures)

- 6.4.14 Phenix Construction Technologies (M&B Engineering)

- 6.4.15 Satec EnvirEngineering (India)

- 6.4.16 Sharp Tanks & Structurals

- 6.4.17 SKV Engineering India Pvt. Ltd.

- 6.4.18 Spacechem Group (Spacechem Engineers)

- 6.4.19 Tata BlueScope Building Solutions (BUTLER)

- 6.4.20 Tata Projects

- 6.4.21 TJSV Steel Fabrication & Galvanizing

- 6.4.22 Zamil Steel Buildings India

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment