PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043982

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043982

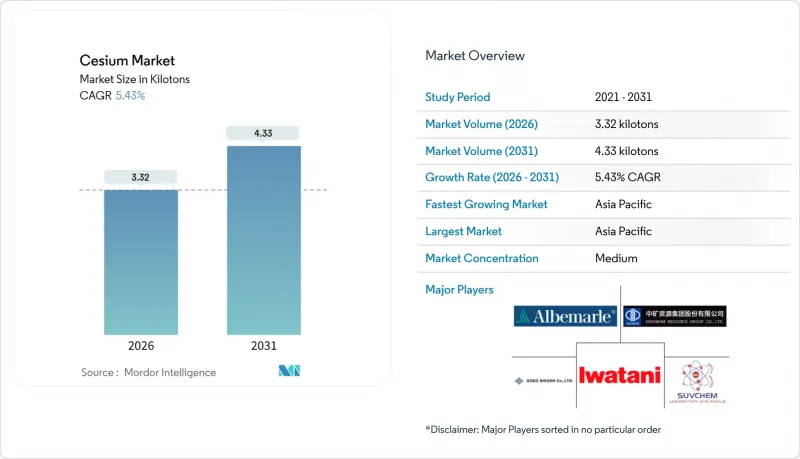

Cesium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Cesium Market size is estimated at 3.32 kilotons in 2026, and is expected to reach 4.33 kilotons by 2031, at a CAGR of 5.43% during the forecast period (2026-2031).

Rising high-pressure high-temperature (HPHT) drilling activity, fast-growing 5G and future 6G infrastructure, and new medical-imaging uses are expanding demand even as the pipeline of primary pollucite ore remains thin. Vertically integrated suppliers have reacted by raising prices in 2024 while locking in multiyear contracts with drilling-service companies to secure scarce feedstock. Asia-Pacific leads both consumption and processing because China refines the bulk of global cesium salts, and Japan dominates precision-electronics applications. In North America and Europe, offshore HPHT completions and defense programs sustain a stable demand base but expose buyers to a single-supplier risk centered on Sinomine and Albemarle.

Global Cesium Market Trends and Insights

Surging Use of Cesium-Formate Fluids in Ultra-Deep HPHT Wells

Cesium-formate brines, with high densities and minimal formation damage, have emerged as the go-to completion fluid for reservoirs exceeding 20,000 psi. Operators in the North Sea, Gulf of Mexico, and Brazil have demonstrated that they can recover the cost of these fluids within a year, thanks to preserved formation integrity and enhanced lifetime recovery. The global inventory of cesium-formate is limited, and the supply is tightening as the demand for deeper wells grows. In response, Sinomine has established dedicated recovery bases in Aberdeen and Bergen, and has tied long-term supply contracts to Brent oil futures. These strategic moves not only safeguard profit margins but also create barriers for new competitors in the HPHT service chain, solidifying Sinomine's dominance in the cesium market.

Proliferation of 5G/6G Networks Requiring Ultra-Stable Cesium Clocks

Telecom operators are increasingly replacing rubidium oscillators with cesium atomic clocks, which can maintain GPS-free accuracy for an extended period. This shift is largely driven by the need for sub-microsecond synchronization, a requirement for 5G coordinated multipoint transmission. Vodafone Turkey's 2024 deployment is just one example of a trend that's rapidly gaining momentum in China, South Korea, and the United States. While optical lattice clocks have achieved greater accuracy than cesium in laboratory settings, the regulatory metrology still recognizes the SI second based on the 9.19 GHz cesium-133 transition. As long as standards bodies uphold this definition, cesium's dominant position-and the market for cesium-remains firmly established.

Limited Number of Commercially Active Pollucite Mines

In 2024, the absence of a continuously operating primary pollucite mine compelled the demand for cesium salts-used outside of drilling fluids-to depend on existing inventories and sporadic outputs from Tanco. Despite Sinomine's leadership, Tanco has opted for batch processing over continuous operations, hinting at either subpar ore grades or challenging processing economics given the current price levels. With global reserves of cesium oxide (Cs2O) showing no significant discoveries since the early 2000s, aerospace and defense sectors have begun stockpiling high-purity cesium carbonate and metal. This move has not only heightened their working-capital demands but also dampened the demand's elasticity in the cesium market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Cs-Based Scintillators in Advanced Medical Imaging

- Rise of Mini-Cs Atomic Clocks for Autonomous and Defense UAV Fleets

- Tight Export Controls on Strategic Alkali Metals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cesium market size for compounds stood equals to 73.45% of total volume, and is forecast to grow at 6.02% through 2031. Formate brines lead this segment, while carbonate supports pharmaceutical catalysis and high-refractive-index glass. Iodide and bromide cater to scintillator and infrared-optics markets. The metal segment commands premium margins as purity levels increase. Although each CSAC unit requires only small amounts of metal, defense buyers are willing to pay significantly higher prices compared to commodity salts, insulating this sub-segment from broader market fluctuations.

As global infrastructure and healthcare spending rise, the demand for cesium compounds-driven by HPHT drilling, specialty glass, and medical imaging-is set to continue. While metal demand will see episodic growth aligned with defense procurement and telecom upgrades, it won't alter the overall tonnage balance. Other cesium derivatives like hydroxide, fluoride, and antimonide will remain niche players, catering to etching chemistry and photocathodes, collectively making up a minor portion of the market. Thus, vertical integration into both cesium compounds and metal emerges as the most reliable strategy against demand fluctuations in the industry.

The Cesium Market Report is Segmented by Product Type (Cesium Metal, Cesium Compounds, and Other Product Types), Application (Oil and Gas, Electronics, Medical and Healthcare, and Other Applications), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 43.86% of the cesium market share in 2025 and is anticipated to log the fastest 6.56% CAGR to 2031. China, boasting the world's largest refinery cluster, adeptly transforms pollucite sourced from Canada and Zimbabwe into carbonate, iodide, and ultra-dry formate. Meanwhile, Japan's specialized producers, spearheaded by GODO SHIGEN and Iwatani, not only cater to domestic electronics with atomic-clock-grade salts but also export their surplus to North America and Europe. South Korea's nationwide 5G Advanced upgrade amplifies the regional demand for cesium oscillators. Concurrently, Chinese offshore explorations in the South China Sea bolster the demand for formate. However, a looming concern is the pending export-license frameworks, which may redirect high-purity cesium to prioritize domestic aerospace and telecom needs.

North America and Europe, while mature, represent a market cluster of strategic significance. Western refining of cesium metal and its specialty compounds finds a cornerstone in Albemarle's Langelsheim plant in Germany. The Lower Tertiary HPHT wells in the Gulf of Mexico and the aging high-pressure reservoirs of the North Sea guarantee a steady offtake of formate. Yet, both regions find themselves heavily reliant on upstream ore supplied by Sinomine. In the U.S., defense sectors are stockpiling cesium metal for CSAC programs, even if it means accepting longer lead times and incurring higher purity-assurance costs. Across the Atlantic, European importers face challenges with the traceability mandates of the EU Critical Raw Materials Act. While these mandates extend procurement cycles, they might also set the stage for a revival of North American pollucite operations, especially if prices surpass a critical threshold.

While the Rest of the World currently plays a modest role, its potential is undeniably strategic. In Brazil's pre-salt fields, Petrobras and its partners are tapping into formate brines for depths surpassing 7,000 m, signaling a demand that could stretch through 2030. West Africa's deepwater activities, though swayed by oil-price fluctuations, hint at a promising long-term trajectory as infrastructure continues to develop. However, Africa's potential as a cesium supplier is closely tied to a rebound in lithium prices. Projects in lepidolite-rich regions of Namibia, Zimbabwe, and the DRC are banking on higher lithium values to make cesium co-processing viable. Without this price recovery, these nations remain on the periphery as prospective suppliers, leaving the global cesium market heavily concentrated in a select few producing locales.

- Albemarle Corporation

- GODO SHIGEN Co., Ltd.

- Iwatani Corporation

- Sinomine Resource Group Co., Ltd.

- Suvchem

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging use of cesium-formate fluids in ultra-deep HPHT wells

- 4.2.2 Proliferation of 5G/6G networks requiring ultra-stable cesium clocks

- 4.2.3 Growing demand for Cs-based scintillators in advanced medical imaging

- 4.2.4 Rise of mini-Cs atomic clocks for autonomous and defense UAV fleets

- 4.2.5 Pilot-scale extraction of cesium from lepidolite tailings in Africa

- 4.3 Market Restraints

- 4.3.1 Limited number of commercially active pollucite mines

- 4.3.2 Tight export controls on strategic alkali metals

- 4.3.3 Volatile pricing due to by-product dependence on Li supply

- 4.4 Value Chain Analysis

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Policy Analysis

- 4.6.1 Export Controls and Trade Restrictions

- 4.6.2 Environmental Regulations

- 4.7 Pricing Analysis

- 4.7.1 Historical Price Trend

- 4.7.2 Price Influencing Factors

- 4.8 Trade Analysis

- 4.9 Production Cost Analysis

- 4.10 Porter's Five Forces

- 4.10.1 Threat of New Entrants

- 4.10.2 Bargaining Power of Suppliers

- 4.10.3 Bargaining Power of Buyers

- 4.10.4 Threat of Substitutes

- 4.10.5 Competitive Rivalry

- 4.11 List of Cesium Mines, By Company

- 4.12 Supply Analysis

- 4.13 Regulatory Policy Analysis

- 4.14 Trade Analysis

- 4.15 Price Trend Analysis

- 4.16 Production Cost Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Cesium Metal

- 5.1.2 Cesium Compounds

- 5.1.3 Other Product Types

- 5.2 By Application

- 5.2.1 Oil and Gas

- 5.2.2 Electronics

- 5.2.3 Medical and Healthcare

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Rest of the World

6 Competitive Landscape

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Albemarle Corporation

- 6.4.2 GODO SHIGEN Co., Ltd.

- 6.4.3 Iwatani Corporation

- 6.4.4 Sinomine Resource Group Co., Ltd.

- 6.4.5 Suvchem

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment