PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062280

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062280

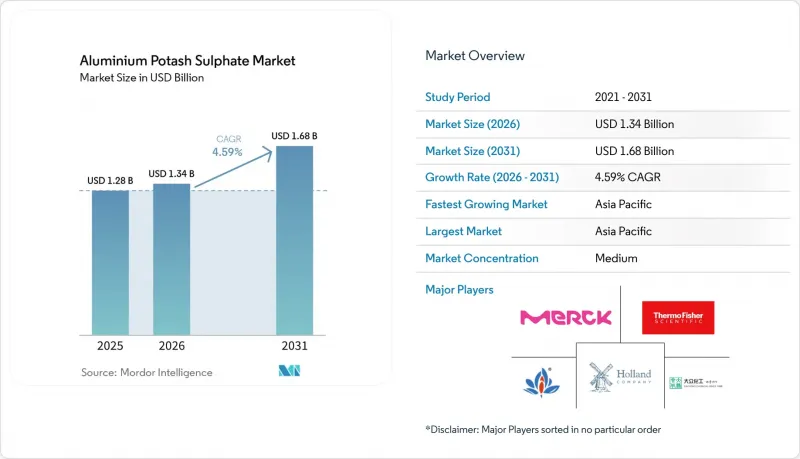

Aluminium Potash Sulphate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aluminium potash sulphate market size is projected to be USD 1.28 billion in 2025, USD 1.34 billion in 2026, and reach USD 1.68 billion by 2031, growing at a CAGR of 4.59% from 2026 to 2031.

This report is Segmented by Form (Solid, Liquid Solutions), Grade (Industrial Grade, Food Grade, and More), Application (Water and Wastewater Treatment, Textile and Leather Processing, and More), End-User (Municipal, Industrial, Commercial, Household), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Aluminium Potash Sulphate Market Trends and Insights

Increased Use in Natural Deodorants and Personal-Care Astringents

In April 2024, regulators endorsed potassium alum's safety at specific concentrations. This approval led to an increase in natural deodorant launches across both mass and premium markets. Clinical studies indicate that 2-5% formulations reduce underarm odor in less than two weeks with minimal irritation. This enables brands to promote a plant-based narrative without blocking sweat ducts. Formats such as roll-ons and gels, particularly those using hydrogel carriers, are attracting consumers. Additionally, transparent ingredient labels are aligning with the preferences of clean-beauty consumers. Private-label retailers in the United States and Germany are now placing alum crystals alongside synthetic antiperspirants, reflecting broader market acceptance. Suppliers certifying particle sizes under 10 micrometers (µm) for sprays are experiencing increased sales volumes.

Expansion of Textile and Leather Processing in Asia-Pacific

As apparel and footwear production shifts from China to India, Vietnam, and Bangladesh, regional processors are increasing their mordanting and tanning capacities. China's export duties of up to 30% on aluminum products are tightening global alum feedstocks, prompting downstream buyers to secure multi-year supply contracts. European Union (EU) regulations limiting chromium effluent are accelerating the transition to aluminum-based tanning agents, which are less toxic. Furthermore, India's Production Linked Incentive scheme for textiles is driving alum consumption. Multinational leather brands are implementing purchasing scorecards that prioritize suppliers using lower-carbon alum, encouraging mills to adopt waste-aluminum valorization methods.

Stricter Limits on Aluminium in Foods and Cosmetics

Formulators are required to either reduce aluminum levels or invest in analytical verifications due to maximum aluminum thresholds set by the European Scientific Committee on Consumer Safety (SCCS) opinion and increasing consumer scrutiny. Germany's regulations prohibit uncoated aluminum from coming into contact with acidic foods, necessitating retrofits for coatings and reducing the demand for bulk aluminum. Additionally, testing for nanoform exclusions introduces additional laboratory costs. These regulations enhance consumer safety but also impact growth, particularly in sectors like spray deodorants and acidic pickling.

Other drivers and restraints analyzed in the detailed report include:

- Up-Cycling of Aluminium Waste into High-Purity Potassium Alum

- Adoption in Plant-Based Meat Processing as Clean-Label Firming Agent

- Geopolitical Potash-Supply Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, solid powder and crystal formats held a 63.24% share of the aluminium potash sulphate market, supported by advantages such as dense storage, established dosing equipment, and cost-efficiency. Liquid solutions are projected to grow at a 5.51% compound annual growth rate (CAGR) through 2031. This growth is driven by digital channels enabling small and medium enterprises (SMEs) to avoid on-site dissolution tanks, reducing capital expenditures. Field trials in France demonstrated that electro-Fenton sludge can replace 50% of purchased liquid alum without affecting coagulation efficiency. Municipal utilities continue to prefer dry forms for their bulk storage stability, while craft cosmetic producers opt for pre-dissolved grades to minimize dust exposure. Additionally, hybrid concentrate pouches designed for automated dispensers are merging traditional formats, allowing suppliers to market both.

North America is experiencing significant growth in liquid solutions due to the Occupational Safety and Health Administration (OSHA) dust-exposure limits encouraging liquid dosing. Conversely, textile mills in the Asia-Pacific region maintain powder-feed systems due to lower labor costs and established supply chains. As containerized shipping becomes more efficient, the economics of liquid freight improve, addressing previous challenges associated with water weight. The competitive landscape will depend on suppliers' ability to ensure shelf-life stability and prevent microbial growth in aqueous solutions.

In 2025, industrial grades accounted for 60.56% of the aluminium potash sulphate market, driven by applications in water treatment and textile mordanting. Pharmaceutical and cosmetic grades are forecast to grow at a 5.83% CAGR through 2031, supported by European Union (EU) regulations on particle sizes for aerosols, which effectively require near-United States Pharmacopeia (USP) purity. Price premiums of 30-50% are encouraging producers to invest in recrystallization and inductively coupled plasma mass spectrometry (ICP-MS) analytics. Food-grade alum occupies a middle ground, catering to baking and the growing plant-protein market, which demands Generally Recognized as Safe (GRAS) compliance but not full pharmacopeial standards.

Producers implementing closed-loop rinsing and high-efficiency particulate air (HEPA) filtration are achieving heavy-metal baselines below 10 parts per million (ppm), meeting Nordic eco-label standards. While industrial buyers in Asia-Pacific remain cost-focused, cosmetics exporters in South Korea are increasingly requiring European Pharmacopeia (EP)/USP certification to meet EU import standards. This segmentation divides the aluminium potash sulphate market into volume-driven industrial channels and value-driven specialty segments, encouraging dual-line manufacturing strategies.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.88% of the aluminium potash sulphate market share and is projected to achieve a 5.81% compound annual growth rate (CAGR) through 2031. China's 711 million-ton bauxite reserves, along with its export-duty regime, are tightening the supply of alum feedstock. This has led processors in India and Vietnam to explore alternative supply chains and invest in scrap-based alum production. Japan and South Korea are utilizing high-purity alum in semiconductor-grade water systems, while ASEAN nations are expanding their textile and leather industries under favorable trade agreements. Regional growth is supported by urbanization, stricter wastewater standards, and policies promoting a circular economy.

North America demonstrates stable municipal demand, with notable growth in household and cosmetics applications. The United States Environmental Protection Agency's (EPA) nutrient criteria continue to drive alum dosing for phosphorus removal, maintaining baseline consumption. Proximity to Saskatchewan potash ensures a reliable feedstock supply, while Mexico's maquiladora industries are increasingly adopting high-purity water treatment solutions.

Europe, operating under stringent Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) and Scientific Committee on Consumer Safety (SCCS) regulations, is experiencing increased demand for pharmaceutical-grade alum with precise particle-size control. Geopolitical disruptions in potash supply have raised costs, but circular economy incentives are encouraging aluminum-scrap utilization. Germany and France are key markets for cosmetics applications, while Nordic utilities are implementing renewable-powered crystallisation to meet low-carbon procurement requirements.

South America and the Middle East & Africa are emerging markets in this sector. Brazil's sanitation programs and Saudi Arabia's desalination pre-treatment initiatives are driving baseline growth. However, logistical challenges and limited analytical capacity are constraining short-term expansion. Multilateral infrastructure funding is expected to enhance market penetration over the next decade.

- Alpha Chemika

- Amar Narain Industries

- American Elements

- Arch Industries

- Avantor, Inc.

- GEO Specialty Chemicals

- GFS Chemicals, Inc.

- Hengyang Jianheng Industry Development Co., Ltd.

- HOLLAND COMPANY

- K+S Aktiengesellschaft

- Merck KGaA

- NATIONAL CHEMICAL INDUSTRIES

- Otto Chemie Pvt. Ltd.

- Thermo Fisher Scientific Inc.

- Zibo Dazhong Edible Chemical Co., LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased use in natural deodorants and personal-care astringents

- 4.2.2 Expansion of textile and leather processing in Asia-Pacific

- 4.2.3 Up-cycling of aluminium waste into high-purity potassium alum

- 4.2.4 Adoption in plant-based meat processing as clean-label firming agent

- 4.2.5 Digital-direct B2B distribution unlocking SME demand

- 4.3 Market Restraints

- 4.3.1 Stricter limits on aluminium in foods and cosmetics

- 4.3.2 Geopolitical potash-supply volatility (sanctions, export bans)

- 4.3.3 High energy intensity of alum crystallisation limiting green credentials

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Form

- 5.1.1 Solid (Powder, Crystals)

- 5.1.2 Liquid Solutions

- 5.2 By Grade

- 5.2.1 Industrial Grade

- 5.2.2 Food Grade

- 5.2.3 Pharmaceutical/Cosmetic Grade

- 5.3 By Application

- 5.3.1 Water and Wastewater Treatment

- 5.3.2 Textile and Leather Processing

- 5.3.3 Cosmetics and Personal Care

- 5.3.4 Food and Beverage Additives

- 5.3.5 Pharmaceuticals and Medical

- 5.3.6 Paper and Pulp Industry

- 5.3.7 Other (Photography, Fireproofing, Agriculture)

- 5.4 By End-User Industry

- 5.4.1 Municipal

- 5.4.2 Industrial

- 5.4.3 Commercial

- 5.4.4 Household

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Alpha Chemika

- 6.4.2 Amar Narain Industries

- 6.4.3 American Elements

- 6.4.4 Arch Industries

- 6.4.5 Avantor, Inc.

- 6.4.6 GEO Specialty Chemicals

- 6.4.7 GFS Chemicals, Inc.

- 6.4.8 Hengyang Jianheng Industry Development Co., Ltd.

- 6.4.9 HOLLAND COMPANY

- 6.4.10 K+S Aktiengesellschaft

- 6.4.11 Merck KGaA

- 6.4.12 NATIONAL CHEMICAL INDUSTRIES

- 6.4.13 Otto Chemie Pvt. Ltd.

- 6.4.14 Thermo Fisher Scientific Inc.

- 6.4.15 Zibo Dazhong Edible Chemical Co., LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment