PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043988

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043988

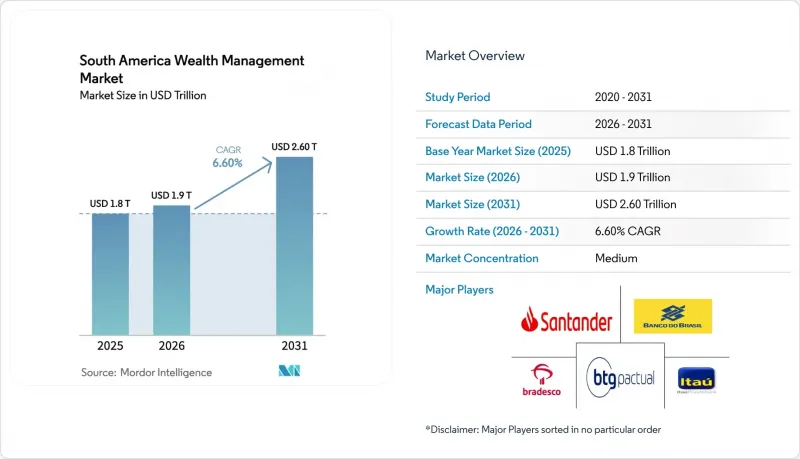

South America Wealth Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America Wealth Management Market size is expected to grow from USD 1.8 trillion in 2025 to USD 1.9 trillion in 2026 and is forecast to reach USD 2.60 trillion by 2031 at 6.60% CAGR over 2026-2031.

The South America wealth management market is anchored by regulatory modernization, digital distribution, and deepening advisory adoption across client tiers. Wealth platforms are aligning to Open Finance frameworks that enable data sharing and, when investment portability arrives at scale, lower switching frictions that favor advice-led relationships and broader product penetration. Portfolio construction is shifting as clients respond to high domestic rates in Brazil that pulled assets into fixed income while alternatives scale through private credit and infrastructure funds that deliver higher spreads at controlled default rates. Firms with credible cross-border capabilities are capturing fee-rich offshore mandates as tax reform and diversified booking centers make advisory on global allocations more complex and valuable. Consolidation among universal banks and specialist multifamily offices raises competitive benchmarks on scale, product breadth, and technology investment across the South America wealth management market.

South America Wealth Management Market Trends and Insights

Open Finance Enables Scalable Digital Wealth

Brazil's Open Finance now serves 52 million clients with 103 million active data-sharing authorizations across more than 700 institutions and processes 3.5 billion data requests weekly as of September 2025. Investment and salary portability are the next milestones, with the central bank coordinating with securities regulators to enable asset transfers without liquidation, a change expected to lower switching frictions while protecting client tax lots. Platforms that already embed pre-integration APIs and comprehensive planning tools are monetizing data aggregation. Outside Brazil, Chile's formal Open Finance rulemaking positions the country for a 2027-2029 go-live, creating an interoperable environment that can extend digital onboarding and portability benefits to South American investors. Adoption still faces a trust gap because fewer than half of eligible Brazilian accounts opted into sharing, even with Open Finance at scale, which currently advantages incumbents with brand equity and robust security practices. As portability matures, advisory-led models within the South America wealth management market should gain share due to seamless rebalancing and cross-institution product comparability.

Yield Rotation Anchors AuM Growth

Brazil's SELIC ended 2025 at 15%, which reinforced a migration into fixed income and supported USD 14.9 billion in net inflows to fixed-income funds during FY2025, within USD 1.9 trillion in total fund AuM that grew 15.2% year over year. Free duration and free credit categories together gained USD 26.2 billion in positive flows as wealth managers emphasized carry strategies and real yields above 5% after inflation. BTG Pactual closed 2025 with USD 219.1 billion in wealth assets and USD 38.0 billion in net new money, citing breadth in fixed-income solutions that layered duration and credit exposure to stabilize returns. The same dynamic raises reinvestment risk if rate easing resumes in 2026 or 2027, which would encourage rebalancing toward equities and alternatives unless portfolios are proactively positioned in blended strategies. XP Inc. reflected this shift as fixed income overtook equities in retail revenue, while the company grew loans to USD 11.9 billion and retirement assets to USD 14.4 billion to diversify income sources. Argentina presents a different pathway, where policy recalibration and a currency band of USD 0.7 to USD 1.0 per USD equivalent range guide a cautious rebuild of risk assets with a preference for dollar-linked structures.

Tax Reform Drives Portfolio Replatforming

Brazil enacted Law 15,270/2025 in December 2025, which raised monthly income-tax exemptions to USD 879 and annual exemptions up to USD 10,549 for lower-income filers, while introducing a 10% rate on foreign profits and dividends and a minimum-tax mechanism for high-income dividend recipients. The update interacts with Law 14,754/2023, which applies annual taxes up to 15% on income from offshore investments that are tied to Brazil, which is now pushing wealth managers to reconfigure vehicles toward tax-advantaged domestic options or treaty-aligned structures. Itau Private Bank is channeling sustainable-finance mandates as part of a plan to mobilize USD 175.8 billion by 2030 and has recommended 1% to 3% Bitcoin allocations for diversification since December 2025 within a controlled risk framework. The minimum-tax design raises planning complexity because advisors must model total taxable income before recommending dividend withdrawal strategies and entity choices. Argentina's IMF program sets fiscal targets that affect tax and capital-account policies, and with no harmonized dividend or wealth-tax guidance published in 2025, long-term after-tax projections remain challenging for repatriation scenarios. Chile's regulator is focused on Basel III Pillar 2 implementation, which may indirectly influence leverage-driven strategies that rely on bank intermediation for private-banking clients.

Other drivers and restraints analyzed in the detailed report include:

- Cross-Border Diversification Lifts Advisory Revenues

- Family-Office Professionalization Boosts UHNW Demand

- Private Credit Expands Advised Allocations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-net-worth individuals accounted for 56.4% of total assets in 2025, reinforcing that upper wealth tiers anchor fee pools in the South America wealth management market. The mass-affluent cohort is expanding fastest with a 9.6% CAGR to 2031 as digital onboarding and Open Finance aggregation cut acquisition costs and enable scaled financial planning. UHNW households, though fewer in number, drive high-touch mandates that include succession planning, philanthropy structuring, and co-investments that stretch beyond the capacity of standard relationship teams. Family-office adoption, at 38% of UHNW families in South America, continues to rise as governance needs grow and portfolios span multiple jurisdictions with varied tax and reporting regimes.

The South America wealth management market is also widening access to alternative investments once limited to UHNW clients, including private credit sleeves in the 5% to 20% range, depending on liquidity profiles. Regulatory support for data portability should further normalize advice-led distribution as clients move providers without forced liquidations once investment portability is launched. The South America wealth management market size for this segment is set to benefit from rules that raise disposable income and enhance digital trust, which can redirect savings into advisory channels. As Open Finance matures in Chile and consumer protections advance in Peru, spillover effects from Brazil's digital playbook are likely to expand the adviceable base.

The South America Wealth Management Industry is Segmented by Client Wealth Tier (UHNWI, HNWI, and Mass Affluent), Firm Type (Private Banks, Family Offices, and Others), Product Type (Fixed Income, Equities, Alternatives, and More), and Geography (Brazil, Chile, Peru, and More). The Report Offers Market Size and Forecasts for the South America Wealth Management Market in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- Itau Private Bank

- BTG Pactual Wealth Management

- Bradesco Private Bank

- Banco do Brasil Private

- Banco Safra Private Banking

- Santander Private Banking (LatAm)

- UBS Wealth Management Brazil

- XP Private

- Citi Private Bank (Brazil & LatAm)

- LarrainVial Wealth Management (Chile)

- Credicorp Capital Wealth Management (Peru/Chile/Colombia)

- Banco de Chile - Private Banking

- BBVA Peru - Global Wealth/Prime

- Itau Personal Bank (Chile)

- BTG Pactual Wealth (Chile/Peru/Colombia)

- Banco Galicia - Banca Privada (Argentina)

- Banco Macro - Selecta/Wealth

- UBS (post-CS) LatAm platform (Brazil focus)

- Julius Baer (Brazil/LatAm EAM links)

- Citi Private Bank - Rio/Sao Paulo desks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Yield rotation anchors AuM growth

- 4.2.2 Open Finance enables scalable digital wealth

- 4.2.3 Cross-border diversification lifts advisory revenues

- 4.2.4 Family-office professionalization boosts UHNW demand

- 4.2.5 Tax reform drives portfolio replatforming

- 4.2.6 Private credit expands advised allocations

- 4.3 Market Restraints

- 4.3.1 Volatility suppresses risk appetite and inflows

- 4.3.2 Fee compression pressures platform profitability

- 4.3.3 Open Finance trust gaps slow portability

- 4.3.4 Tax-regime fluidity raises compliance friction

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Additional South America-specific Landscape Items

5 Market Size & Growth Forecasts

- 5.1 By Client Wealth Tier

- 5.1.1 UHNWI

- 5.1.2 HNWI

- 5.1.3 Mass Affluent

- 5.2 By Firm Type

- 5.2.1 Private Banks

- 5.2.2 Family Offices

- 5.2.3 Others (Independent/External Asset Managers)

- 5.3 By Product Type

- 5.3.1 Fixed Income

- 5.3.2 Equities

- 5.3.3 Alternatives

- 5.3.4 Cash and Deposits

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Peru

- 5.4.3 Chile

- 5.4.4 Argentina

- 5.4.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Itau Private Bank

- 6.4.2 BTG Pactual Wealth Management

- 6.4.3 Bradesco Private Bank

- 6.4.4 Banco do Brasil Private

- 6.4.5 Banco Safra Private Banking

- 6.4.6 Santander Private Banking (LatAm)

- 6.4.7 UBS Wealth Management Brazil

- 6.4.8 XP Private

- 6.4.9 Citi Private Bank (Brazil & LatAm)

- 6.4.10 LarrainVial Wealth Management (Chile)

- 6.4.11 Credicorp Capital Wealth Management (Peru/Chile/Colombia)

- 6.4.12 Banco de Chile - Private Banking

- 6.4.13 BBVA Peru - Global Wealth/Prime

- 6.4.14 Itau Personal Bank (Chile)

- 6.4.15 BTG Pactual Wealth (Chile/Peru/Colombia)

- 6.4.16 Banco Galicia - Banca Privada (Argentina)

- 6.4.17 Banco Macro - Selecta/Wealth

- 6.4.18 UBS (post-CS) LatAm platform (Brazil focus)

- 6.4.19 Julius Baer (Brazil/LatAm EAM links)

- 6.4.20 Citi Private Bank - Rio/Sao Paulo desks

7 Market Opportunities & Future Outlook

- 7.1 Onshoring and tax-optimized discretionary mandates post-reform

- 7.2 Digital wealth orchestration via Open Finance and alternative distribution