PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044037

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044037

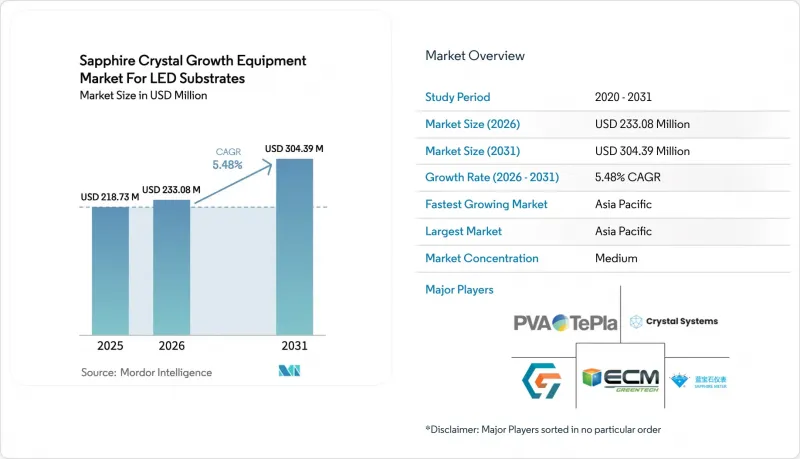

Sapphire Crystal Growth Equipment For LED Substrates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The sapphire crystal growth equipment market for LED substrates market size was valued at USD 218.73 million in 2025, USD 233.08 million in 2026, and reach USD 304.39 million by 2031, at a CAGR of 5.48% during the forecast period (2026-2031).

Moderating general-illumination demand in North America and Europe coincides with rising specification pressure from mini-LED backlighting, automotive head-up displays and augmented-reality devices. Chinese epitaxy foundries accounted for roughly 60% of global sapphire wafer capacity additions between 2024 and 2025, yet their recent equipment spend skews toward larger-diameter boules and advanced automation, compressing order cycles for legacy 4-inch lines. Western furnace vendors defend share in above-300 mm systems by leveraging patented thermal-field designs, while Chinese peers gain traction in the 150-300 mm segment through price leadership and localized service. The interplay between premium display uptake and continued LED retrofit mandates under the U.S. Department of Energy and European Union Ecodesign directive will determine whether the projected growth curve accelerates beyond today's mid-single-digit baseline.

Insights and Trends of Sapphire Crystal Growth Equipment Market For LED Substrates

Aggressive Capacity Expansion by Chinese Epitaxy Foundries

Chinese LED chipmakers commissioned more than 150 new MOCVD reactors during 2024-2025, spearheaded by San'an Optoelectronics and HC SemiTek, whose CNY 2.8 billion (USD 392 million) Yangzhou project targets mini-LED and micro-LED substrates. This uptick triggered a near-term spike in demand for 6-inch and 8-inch sapphire wafers, yet it also realigned procurement toward 150-300 mm and above-300 mm furnaces that optimize throughput per boule. State Council funding of CNY 50 billion (USD 7 billion) for compound-semiconductor infrastructure reinforces the build-out, although wafer ASPs slipped 12% year-on-year in Q1 2025, compelling buyers to prioritize automation that compresses cycle time. The net effect raises installed base turnover and lifts attach rates for AI-driven process-control packages, benefiting suppliers able to combine furnace hardware with predictive analytics.

Surging Mini-LED Backlighting Adoption in High-End TVs

Premium television manufacturers shipped roughly 8 million mini-LED sets in 2024, a 35% jump over 2023, with Samsung Electronics and LG Display expanding panel capacity at Paju and other hubs. Each mini-LED array relies on a higher-quality sapphire substrate to achieve bin-matching for thousands of emissive chips, tightening impurity tolerances to sub-1 ppm. Automotive head-up displays and emerging AR glasses evaluate similar architectures, further lifting demand for defect-free boules. Equipment OEMs now face customer specifications that older Kyropoulos lines can meet only via costly retrofits or complete replacement with Czochralski tools that deliver lower dislocation densities. These premium requirements raise per-furnace ASPs but also lock in higher lifecycle revenue from consumables and software upgrades.

High Capex Requirement Compared with SiC Furnace Lines

A turnkey 200 mm sapphire line costs USD 8-12 million, versus USD 5-7 million for an equivalently sized silicon-carbide sublimation setup, while SiC wafers sell at 30-40% higher prices. Government incentives, notably the U.S. CHIPS Act, disproportionately favor SiC and other wide-bandgap materials, further diverting investment. Payback for sapphire tools stretches to 4-5 years under current LED ASPs, a hurdle for venture-backed entrants seeking quicker returns. Vendors mitigate sticker shock through equipment-as-a-service offerings and outcome-based pricing, yet financing constraints still delay adoption among second-tier fabs.

Other drivers and restraints analyzed in the detailed report include:

- Transition Toward 300 mm Sapphire Boules to Reduce Wafer CMP Loss

- Energy Savings Mandates from U.S. DOE and EU Ecodesign

- Volatile Alumina Prices Tightening OEM Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystal growth furnaces anchored 69.87% of 2025 spending, underscoring their central role in the sapphire crystal growth equipment market for LED substrates industry market size. Foundries, however, now increasingly bundle furnaces with software-centric process control packages, lifting automation attach rates to 42% in 2024. The sapphire crystal growth equipment market for LED substrates industry market share for automation and process control systems is poised to expand fastest at 6.13% CAGR through 2031 as wage inflation and tighter display specifications converge. Western OEMs differentiate through AI-driven thermal-field optimization, while Chinese vendors compete on total-cost-of-ownership guarantees that resonate with high-throughput fabs.

Replacement cycles average 8-10 years, yet the pivot to 300 mm compresses depreciation schedules, forcing write-offs of serviceable 6-inch tools. Automation platforms enjoy shorter three-to-five-year refresh intervals, creating a recurring revenue stream that cushions suppliers from furnace order volatility. Consumables such as graphite crucibles and high-purity alumina further lock customers into OEM ecosystems, gradually shifting competitive leverage from hardware price to total solution performance.

The Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and More), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and More), Sapphire Diameter Capability (Up To 150 Mm, 150-300 Mm, and Above 300 Mm), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 72.68% of the sapphire crystal growth equipment market for LED substrates industry market size in 2025 and is tracking a 5.72% CAGR through 2031. China alone absorbed roughly 55% of global wafer output, fueled by municipal subsidies that offset furnace depreciation. Taiwan specializes in high-margin mini-LED substrates, while South Korea's Samsung Display and LG Display balloon mini-LED TV capacity, indirectly ratcheting up sapphire substrate pull. Japan's LED incumbents divert capex to SiC and GaN, yet demand from Nichia and Toyoda Gosei still sustains a niche domestic equipment market.

North America and Europe collectively represented about 18% of 2025 revenue, constrained by limited LED chip fab footprints and subsidy programs skewed toward power electronics. The U.S. CHIPS and Science Act directed only a fractional slice of funding toward sapphire, and Wolfspeed's strategic pivot to SiC eliminated a major historical buyer. Europe's Chips Act similarly orients toward advanced logic and SiC, leaving sapphire consumption to specialized vendors such as Monocrystal, whose EU shipments face sanctions-related friction. Regulations still spur LED adoption, but the resulting substrate orders largely accrue to Asian foundries.

The Rest of the World accounted for less than 10% of sales in 2025, yet infrastructure electrification in Saudi Arabia, the UAE and Brazil positions the region for incremental gains. India's USD 10 billion Semiconductor Mission could alter the map by 2028-2030, though no sapphire tool orders were booked as of March 2026. Equipment OEMs weigh joint-venture assembly models to satisfy potential domestic-content rules, especially as South Asian governments explore localization incentives.

- GT Advanced Technologies Inc.

- PVA TePla AG

- ECM Greentech S.A. (Cyberstar)

- Crystal Systems Inc.

- Zhejiang Jingjing Science and Technology Co., Ltd.

- Crystec Technology Trading GmbH

- Monocrystal LLC

- Ferrotec Holdings Corporation

- Castech Inc.

- Linton Crystal Technologies

- Hangzhou Shalom Electro-optics Technology Co., Ltd.

- Advanced Crystal Technology Inc.

- Naura Technology Group Co., Ltd.

- Toyo Tanso Co., Ltd.

- Changchun Up Optotech Co., Ltd.

- Silian Optoelectronics (Chongqing) Co., Ltd.

- Heraeus Noblelight Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Mini-LED Backlighting Adoption in High-End TVs

- 4.2.2 Aggressive Capacity Expansion by Chinese Epitaxy Foundries

- 4.2.3 Energy Savings Mandates From U.S. DOE and EU Ecodesign

- 4.2.4 Transition Toward 300 mm Sapphire Boules to Reduce Wafer CMP Loss

- 4.2.5 Integration of AI-Enabled Predictive Control in Growth Furnaces

- 4.2.6 Accelerated Capital Subsidies for Compound-Semiconductor Clusters in India

- 4.3 Market Restraints

- 4.3.1 Volatile Alumina Prices Tightening OEM Margins

- 4.3.2 High Cap-Ex Requirement Compared with SiC Furnace Lines

- 4.3.3 Yield Losses During Core-Drilling of Large-Diameter Boules

- 4.3.4 Sluggish LED Lighting Retrofit Demand in Europe Post-2024

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Ecosystem Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Crystal Growth Furnaces

- 5.1.2 Thermal Field and Crucible Systems

- 5.1.3 Growth Automation and Process Control Systems

- 5.2 By Growth Technology

- 5.2.1 Kyropoulos Method

- 5.2.2 Edge-Defined Film-Fed Growth (EFG)

- 5.2.3 Heat Exchanger Method

- 5.2.4 Czochralski Method

- 5.3 By Sapphire Diameter Capability

- 5.3.1 Upto 150 mm

- 5.3.2 150-300 mm

- 5.3.3 Above 300 mm

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GT Advanced Technologies Inc.

- 6.4.2 PVA TePla AG

- 6.4.3 ECM Greentech S.A. (Cyberstar)

- 6.4.4 Crystal Systems Inc.

- 6.4.5 Zhejiang Jingjing Science and Technology Co., Ltd.

- 6.4.6 Crystec Technology Trading GmbH

- 6.4.7 Monocrystal LLC

- 6.4.8 Ferrotec Holdings Corporation

- 6.4.9 Castech Inc.

- 6.4.10 Linton Crystal Technologies

- 6.4.11 Hangzhou Shalom Electro-optics Technology Co., Ltd.

- 6.4.12 Advanced Crystal Technology Inc.

- 6.4.13 Naura Technology Group Co., Ltd.

- 6.4.14 Toyo Tanso Co., Ltd.

- 6.4.15 Changchun Up Optotech Co., Ltd.

- 6.4.16 Silian Optoelectronics (Chongqing) Co., Ltd.

- 6.4.17 Heraeus Noblelight Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment