PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044041

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044041

Japan Sapphire Crystal Growth Equipment For LED Substrates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

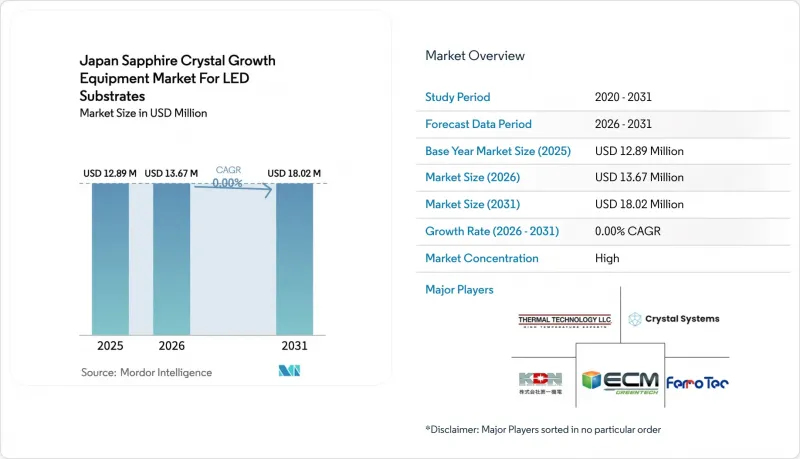

The Japan sapphire crystal growth equipment market for LED substrates industry size is expected to increase from USD 12.89 million in 2025 to USD 13.67 million in 2026 and reach USD 18.02 million by 2031, growing at a CAGR of 5.68% over 2026-2031.

Strong display-panel demand for mini-LED and micro-LED back-lighting is widening the domestic order book for large-diameter, low-defect sapphire furnaces, even as general-lighting demand plateaus. Equipment spending is heavily skewed toward Kyropoulos and Czochralski furnaces that can yield 6-inch and 8-inch boules with stable thermal gradients, while integrated metrology and AI-driven control modules push yields higher and labor dependency lower. Energy-cost volatility and tight iridium and molybdenum supply chains still weigh on smaller epitaxial houses, but government subsidies and vertical-integration moves by local component makers are trimming effective payback horizons for new tool installs.

Insights and Trends of Japan Sapphire Crystal Growth Equipment Market For LED Substrates

Rising Demand for Mini- and Micro-LED Back-lighting in High-Resolution Displays

Premium television, notebook, and automotive OEMs moved from edge-lit to mini-LED architectures during 2025, multiplying the number of die-level emitters per panel and pushing sapphire-wafer pullers to run longer campaigns. Commercial micro-LED pilots now target sub-100 µm die sizes grown on 6-inch c-plane sapphire, eliminating color filters and thick encapsulants for thinner displays with higher contrast. Osaka University demonstrated europium-doped GaN red LEDs on sapphire that approach 10% external quantum efficiency, allowing monolithic full-color stacks without die-transfer steps. Orbray responded with high-flatness 6-inch substrates that show total-thickness variation below 10 µm, accelerating adoption at Tokushima and Yamaguchi fabs. Electric-vehicle cockpits, which house multiple high-resolution displays, add an auto-grade reliability requirement that further anchors domestic sapphire demand.

Government Incentives for Domestic LED Supply-Chain Localization

Tokyo earmarked roughly USD 870 million in 2024 for compound-semiconductor R&D hubs, with dedicated lines for wide-band-gap devices grown on sapphire. Subsidies lower crystal-growth furnace payback from seven to about four years for small epitaxial houses, while workforce programs rebuild a talent pool hollowed out during the 2010s offshoring wave. Security concerns heightened urgency when China briefly restricted gallium and germanium exports in 2023; policymakers now target 30% local sapphire-wafer self-sufficiency by 2030, implying annual furnace installations 15-20% above historical norms.

Capital-Intensive Furnace Procurement Cycle for SME Epi-Houses

Premium Kyropoulos and Czochralski tools carry list prices ranging from USD 300,000 to USD 1.5 million, and custom large-boule systems exceed USD 2 million, placing them out of reach for many domestic specialty producers. Each furnace needs 10-20 days per pull, capping annual output near 18 runs and stretching payback horizons beyond five years unless utilization stays above 85%. Japan lacks a mature leasing market for sapphire equipment, so smaller firms must either self-fund or rely on high-interest project loans, both of which constrain working capital. Some plants respond by outsourcing wafers to low-cost Chinese suppliers, sacrificing lead-time control and custom orientation options. This restraint directly slows the refresh cycle for modern, automation-ready furnaces that could lift yields and cut power use.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Adoption of 6-Inch Wafer Lines by Japanese LED IDMs

- Volatility in LED End-Market Demand Post-2025 Lighting Retrofit Peak

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystal growth furnaces commanded 67.91% of the Japan sapphire crystal growth equipment market for LED substrates industry market share in 2025, underscoring their position as the largest single capital item. Thermal-field and crucible kits form the next cost block, with molybdenum replacements priced near USD 500 per piece and iridium containers fetching premium quotes on 99.99% purity needs. Growth-automation and process-control systems, while starting from a smaller base, are projected at a 6.17% CAGR because AI vision and in-chamber metrology cut scrap and operator minutes. Large integrated device manufacturers buy turnkey furnace-plus-automation bundles to raise throughput per clean-room square meter, whereas small specialty houses often continue with manual pullers to contain cash burn.

Competitive dynamics vary by buyer profile. Western vendors dominate high-end projects that demand tight diameter tolerances, while cost-focused Chinese suppliers court peripheral prefectures with 30-40% lower ticket prices. As labor shortages deepen, automation spending should capture an incrementally larger slice of the Japan sapphire crystal growth equipment market for LED substrates industry market size, even if the absolute number of new furnaces rises only modestly. Over the forecast horizon, software and sensor upgrades are expected to deliver more incremental value than hardware wattage alone, reshaping vendor qualification criteria.

The Japan Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and More), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and More), and Sapphire Diameter Capability (Up To 150 Mm, 150-300 Mm, and Above 300 Mm). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ferrotec Holdings Corporation

- Dai-ichi Kiden Co., Ltd.

- Crystal Systems Corporation

- ECM Greentech S.A.

- Thermal Technology LLC

- GT Advanced Technologies Inc.

- PVA TePla AG

- Luoyang Kunsheng Instrument Equipment Co., Ltd.

- Shanghai Xinkehui New Material Co., Ltd.

- ATTL Advanced Materials Co., Ltd.

- TechSapphire LLC

- EZAN-ERIE Ltd.

- Rostoks-N Ltd.

- APEKS Co., Ltd.

- Apollo Crystal LLC

- Ferrotec Material Technologies Corporation

- FAMETEC GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Mini- and Micro-LED Backlighting in High-Resolution Displays

- 4.2.2 Government Incentives for Domestic LED Supply-Chain Localization

- 4.2.3 Mainstream Adoption of 6-inch Wafer Lines by Japanese LED IDMs

- 4.2.4 Efficiency Gains from Furnace Automation and AI-Based Process Control

- 4.2.5 Shift Toward 8-inch Sapphire Wafers in Consumer Electronics Flash LEDs

- 4.2.6 Emergence of GaN-on-Sapphire Power Devices in EV Chargers

- 4.3 Market Restraints

- 4.3.1 Capital-Intensive Furnace Procurement Cycle for SME Epi-Houses

- 4.3.2 Volatility in LED End-Market Demand Post 2025 Lighting Retrofit Peak

- 4.3.3 High Energy Costs for Above 2000 °C Thermal Fields in Japan

- 4.3.4 Supply Risk of Molybdenum and Iridium Crucible Materials

- 4.4 Industry Ecosystem Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Crystal Growth Furnaces

- 5.1.2 Thermal Field and Crucible Systems

- 5.1.3 Growth Automation and Process Control Systems

- 5.2 By Growth Technology

- 5.2.1 Kyropoulos Method

- 5.2.2 Edge-Defined Film-Fed Growth (EFG)

- 5.2.3 Heat Exchanger Method

- 5.2.4 Czochralski Method

- 5.3 By Sapphire Diameter Capability

- 5.3.1 Up to 150 mm

- 5.3.2 150-300 mm

- 5.3.3 Above 300 mm

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ferrotec Holdings Corporation

- 6.4.2 Dai-ichi Kiden Co., Ltd.

- 6.4.3 Crystal Systems Corporation

- 6.4.4 ECM Greentech S.A.

- 6.4.5 Thermal Technology LLC

- 6.4.6 GT Advanced Technologies Inc.

- 6.4.7 PVA TePla AG

- 6.4.8 Luoyang Kunsheng Instrument Equipment Co., Ltd.

- 6.4.9 Shanghai Xinkehui New Material Co., Ltd.

- 6.4.10 ATTL Advanced Materials Co., Ltd.

- 6.4.11 TechSapphire LLC

- 6.4.12 EZAN-ERIE Ltd.

- 6.4.13 Rostoks-N Ltd.

- 6.4.14 APEKS Co., Ltd.

- 6.4.15 Apollo Crystal LLC

- 6.4.16 Ferrotec Material Technologies Corporation

- 6.4.17 FAMETEC GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment