PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044058

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044058

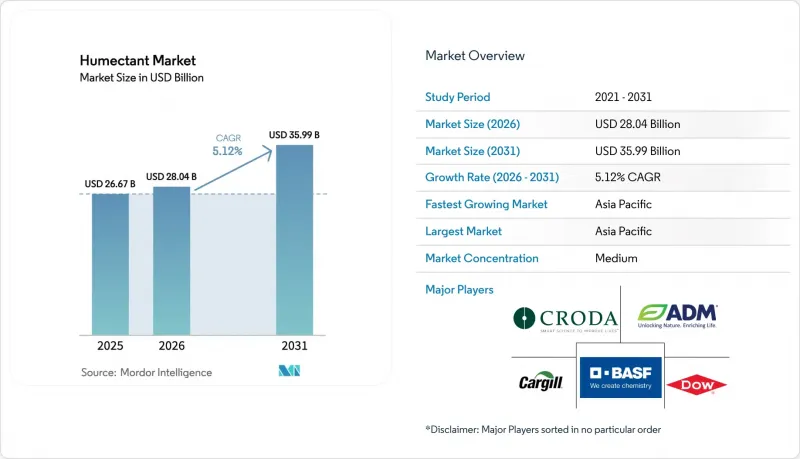

Humectant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Humectant Market size is expected to increase from USD 26.67 billion in 2025 to USD 28.04 billion in 2026 and reach USD 35.99 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

Clean-label mandates in cosmetics, functional-food texture engineering, and structural glycerol oversupply from biodiesel refining are the three forces that keep the humectant market expanding despite propylene-glycol cost swings. Sorbitol's wider usage approvals, together with pharmaceutical-grade humectant demand from the fast-rising nicotine-pouch segment, continue to lift volumes in North America and Scandinavia. Asia-Pacific retains pricing power by integrating excess glycerol from Indonesian and Malaysian biodiesel output into high-value hyaluronic-acid exports. Meanwhile, suppliers hedge feedstock risk by certifying bio-circular propylene glycol and locking in long-term crude-glycerol offtake contracts.

Global Humectant Market Trends and Insights

Rising Demand for Clean-Label Moisturizers in Cosmetics

To meet the transparency demands of millennials and Gen Z, brands are shifting from synthetic emollients to more recognizable humectants like glycerol, sodium PCA, and hyaluronic-acid salts. In response to this trend, ADM completed a USD 26 million upgrade in Erlanger, Kentucky, in January 2026, adding pharmaceutical-grade glycerol and sodium PCA to its offerings. Stricter safety dossier requirements from the U.S. Modernization of Cosmetics Regulation Act of 2022 (MoCRA) and the European Union (EU) Cosmetics Regulation increase compliance costs for lesser-known synthetics. This shift benefits well-characterized humectants, which already possess International Nomenclature of Cosmetic Ingredients (INCI) clearance. While premium brands are willing to shoulder a 10-15% increase in ingredient costs, mass-market players are reformulating their products to maintain their presence on retailer shelves, especially those enforcing clean-label standards. Suppliers are capitalizing on their pricing power, especially for fermentation-derived variants that boast International Sustainability and Carbon Certification (ISCC) PLUS bio-based certification, further distancing themselves from petro-derived alternatives.

Growth of Functional Food and Beverage Formulations for Texture/Shelf-Life

Food formulators are using sorbitol and glycerol to keep sugar-reduced bakery items soft and to mimic the mouthfeel of full-sugar in plant-based protein bars. Beverage brands are increasingly relying on propylene glycol as a solvent and antimicrobial co-factor in natural flavor systems, moving away from sorbates and benzoates without compromising shelf life. Hyaluronic-acid hydrogels are now encapsulating probiotics and flavor oils for a timed release in functional shots, backed by peer-reviewed studies confirming their oral compatibility. Despite a 20-30% price discount compared to cosmetic grades, volume expansion is making it worthwhile. Ingredion is investing in this trend with a dedicated spray-drying line for powdered humectants at its USD 100 million plant in Indianapolis, set to open in H2 2026. This trend is first gaining traction in North America and Europe, but is set to accelerate in the Asia-Pacific, driven by the demand for water-activity control in plant-based meat analogues.

Volatile Propylene-Glycol Feedstock Prices

Propylene glycol's (PG) reliance on propylene oxide makes it vulnerable to fluctuations in refinery utilization and natural gas costs, squeezing margins for independent humectant formulators. In Q4 2025, European spot PG prices surged 22% due to widening naphtha crack spreads, while North America experienced similar price swings linked to outages along the Gulf Coast. Dow and Evonik's HYPROSYN pilot, operational since November 2023 in Hanau, Germany, sidesteps the need for propylene oxide, achieving a 30-40% reduction in capital costs and ensuring more consistent output. Dow's bio-circular propylene glycol, certified by ISCC PLUS and introduced in March 2024 in Freeport, Texas, further distances PG pricing from traditional fossil-propylene sources. However, when formulation parity is reached, cost-sensitive food brands are pivoting to glycerol and sorbitol, resulting in a 0.8 percentage point reduction in the near-term forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Glycerol Output from Biodiesel Refining

- Moisture-Managed Nicotine-Pouch Boom

- Stringent EU REACH Limits on Petro-Humectants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, liquid humectants dominated the market, accounting for 62.84% of total revenue. Their direct metering into beverage syrups and cosmetic emulsions highlights their convenience. The liquid format of humectants, buoyed by Dow's March 2024 launch of bio-circular propylene glycol, which aligns with personal-care sustainability, remains the primary revenue driver. In high-throughput pharmaceutical and cosmetic plants, the batch-to-batch reproducibility of liquids is crucial, especially when closed-loop pumping minimizes contamination risks. Meanwhile, powder variants, expanding at a 5.21% CAGR, cater to distributors in emerging markets. These distributors, lacking refrigerated storage, find powders more cost-effective. Ingredion's new spray-drying line in Indianapolis is set to supply Asia-Pacific contract packers, who will transform these powders into ready-to-drink vegan shakes, underscoring the logistical profitability of powders.

Functional-food brand owners are increasingly turning to powders, as they seek shelf-stable sachets for e-commerce without the need for a cold chain. While solid formats like crystalline sorbitol and mannitol pellets remain niche, they command premium prices in biologics blister packs and moisture-sensitive drug capsules. Regulatory bodies show a preference for solids in modified-release oral forms, but these still lag behind liquids and powders in volume. Looking ahead, while the humectant market is set to maintain its liquid lead, both powder and solid formats present nimble players with opportunities for double-digit margins, especially in Southeastern Asia and the Middle East, where shipping at room temperature is essential.

The Humectant Market Report is Segmented by Form (Liquid, Powder, and Solid), Product Type (Glycerol, Propylene Glycol, Sodium PCA, and Sorbitol), Application (Cosmetic and Personal Care, Food and Beverage, Pharmaceutical, and Tobacco), and Geography (North America, South America, Europe, Asia-Pacific, Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, Asia-Pacific accounted for 39.42% of total revenue and is projected to lead with a 5.96% CAGR from 2026 to 2031. Key drivers include surging hyaluronic-acid registrations in China, scale-oriented generic-drug excipient plants in India, and a biodiesel-linked glycerol glut in Indonesia. In a strategic move, BASF expanded its operations in Bangpakong, Thailand, in November 2025, boosting the output of alkyl-polyglucoside and humectant-compatible surfactants. This ensures a steady local supply for Association of Southeast Asian Nations (ASEAN) manufacturers. The sheer volume of the Asia-Pacific market acts as a buffer, shielding suppliers from margin declines seen in more mature markets.

The United States stands as the dominant force in the nicotine pouch market, accounting for over 90% of Philip Morris International's (PMI) volume. This dominance is also driving a notable surge in the demand for pharmaceutical-grade glycerol. Meanwhile, in Europe, amendments to the REACH regulations are steering formulators towards bio-circular glycerol and sodium PCA. Responding to this trend, Dow has introduced ISCC PLUS-certified propylene glycol from its Stade, Germany, facility, commanding a premium price. This pricing strategy helps narrow the CAGR gap with Asia. Both North America and Europe benefit from strict sustainability standards, allowing them to pass on costs and enhance margins.

While South America, the Middle East, and Africa represent smaller markets, they exhibit significant growth potential. In South America, Brazil takes the lead as BASF channels Macauba-kernel inputs into its local personal-care plants, simultaneously establishing an export route to Europe. The Middle East witnessed a doubling of pouch volumes in 2025, signaling a growing demand for humectants in tobacco harm reduction. In Africa, the pharmaceutical expansions in Nigeria and Kenya are spurring a localized demand for USP-grade glycerol, although logistical challenges hinder wider adoption. Looking ahead, Asia-Pacific is set to achieve the largest absolute revenue gains, North America and Europe will bolster profitability, and emerging regions will offer strategic opportunities for nimble entrants.

- ADM

- Ashland

- BASF

- Cargill, Incorporated.

- CLARIANT

- Croda International Plc

- Dow

- Dupont

- Evonik

- Ingredion

- Lonza

- Lubrizol

- Nouryon

- Roquette Freres.

- Solvay

- Symrise

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for clean-label moisturisers in cosmetics

- 4.2.2 Growth of functional Food and Beverage formulations for texture/shelf-life

- 4.2.3 Expansion of glycerol output from biodiesel refining

- 4.2.4 Regulatory expansion of sugar-alcohol (sorbitol) usage

- 4.2.5 Moisture-managed nicotine-pouch boom

- 4.3 Market Restraints

- 4.3.1 Volatile propylene-glycol feedstock prices

- 4.3.2 Stringent EU REACH limits on petro-humectants

- 4.3.3 Allergen scrutiny of corn-based derivatives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Form

- 5.1.1 Liquid

- 5.1.2 Powder

- 5.1.3 Solid

- 5.2 By Product Type

- 5.2.1 Glycerol

- 5.2.2 Propylene Glycol

- 5.2.3 Sodium PCA

- 5.2.4 Sorbitol

- 5.3 By Application

- 5.3.1 Cosmetic and Personal Care

- 5.3.2 Food and Beverage

- 5.3.3 Pharmaceutical

- 5.3.4 Tobacco

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Info, Products & Services, Recent Developments)

- 6.4.1 ADM

- 6.4.2 Ashland

- 6.4.3 BASF

- 6.4.4 Cargill, Incorporated.

- 6.4.5 CLARIANT

- 6.4.6 Croda International Plc

- 6.4.7 Dow

- 6.4.8 Dupont

- 6.4.9 Evonik

- 6.4.10 Ingredion

- 6.4.11 Lonza

- 6.4.12 Lubrizol

- 6.4.13 Nouryon

- 6.4.14 Roquette Freres.

- 6.4.15 Solvay

- 6.4.16 Symrise

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment