PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044095

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044095

France Hyperscale Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

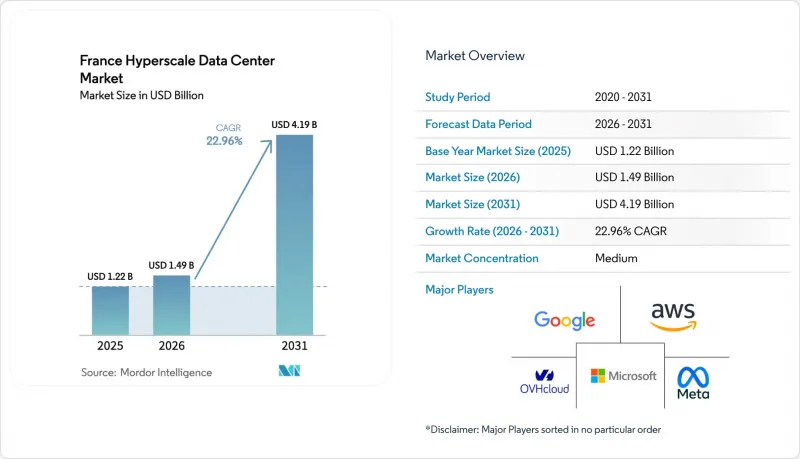

The France hyperscale data center market size is expected to increase from USD 1.22 billion in 2025 to USD 1.49 billion in 2026 and reach USD 4.19 billion by 2031, growing at a CAGR of 22.96% over 2026-2031. The France hyperscale data center market is being propelled by three structural pivots: the siting of NVIDIA's 1.4 GW Paris campus, the French government's program to add six EPR2 nuclear reactors, and the European Sovereign Cloud framework that funnels U.S. and Chinese cloud tenants toward in-country capacity. Operators are capitalizing on France's nuclear-based power mix to host GPU-dense clusters that satisfy low-carbon procurement rules while meeting data-residency mandates. Rapid uptake of liquid-cooling retrofits, the ability to secure long-duration nuclear or offshore-wind power-purchase agreements, and edge-to-core consolidation along the Paris-Marseille fiber corridor together shorten commissioning cycles and lower unit operating costs for the France hyperscale data center market. As hyperscalers replicate sovereign-cloud footprints across EU member states, they must now duplicate availability zones inside France, which inflates regional capex but lifts national installed capacity.

France Hyperscale Data Center Market Trends and Insights

Exploding GPU-Centric AI/ML Workloads from U.S. and China Cloud Tenants

French campuses are absorbing GPU-dense inference clusters that overseas hyperscalers cannot deploy domestically amid power-grid constraints. NVIDIA's 1.4 GW Paris site will house more than 100,000 Blackwell GPUs configured in liquid-cooled designs, making it the largest single-location AI deployment in Europe. A similar 1 GW campus being built in northern France targets Chinese AI labs that require EU data residency. As a result, average rack loads climbed from 8 kW in 2024 to 22 kW in 2025, and operators now specify 40-60 kW cabinets as standard. France's dense network of nuclear plants, permissive AI regulation, and proximity to multiple subsea cables collectively place the France hyperscale data center market at the center of Europe's GPU supply chain.

Sovereign-Cloud Roll-Outs by Hyperscalers in Europe

AWS launched a physically and logically isolated European Sovereign Cloud in January 2026 to ensure that customer data remain exclusively inside the EU and that only EU-resident staff have administrative access. Microsoft added three availability zones in Paris and Marseille in April 2025 to expand its sovereign footprint. Domestic challenger Scaleway obtained SecNumCloud certification in December 2025, allowing French government workloads to reside on its DGX Cloud Lepton platform. These parallel deployments force leading hyperscalers to duplicate infrastructure in multiple member states rather than consolidating in a single low-cost hub, thereby accelerating the France hyperscale data center market while lifting per-unit costs.

Water-Usage Restrictions on Evaporative Cooling

In 2025, prefectures in Ile-de-France capped evaporative-cooling consumption at 0.4 liters per kilowatt-hour, pushing new builds toward closed-loop or dry-cooler designs that cost 30-40% more upfront. OVHcloud demonstrated a water usage effectiveness of 0.3 liters per kilowatt-hour in 2024 by employing adiabatic towers fed by rainwater. While the benchmark proves compliance is possible, land-use and capex barriers lengthen project timelines and reduce near-term additions to the France hyperscale data center market.

Other drivers and restraints analyzed in the detailed report include:

- 5G Edge-Core Consolidation Along Paris-Marseille Fiber Corridors

- Renewable PPAs Tied to New EPR2 and Offshore-Wind Projects

- GPU and Optic Supply-Chain Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hyperscale self-build captured 64.06% of the France hyperscale data center market share in 2025, underscoring the weight that AWS, Microsoft, and Google place on architectural control. Yet colocation is forecast to expand at a 23.43% CAGR, outpacing the overall France hyperscale data center market by 47 basis points. Data4's EUR 5 billion Escaudain campus delivers turnkey shells that shrink commissioning cycles from 36 months to under 18. Vantage Data Centers and Altarea are investing EUR 400 million in a 400 MW Bordeaux campus tailored to sovereign-cloud tenants constrained by balance-sheet limits.

Self-build will remain the method of choice for workloads that demand deterministic performance across global availability zones. AWS's sovereign-cloud regions employ identical rack layouts from Paris to Milan, a standardization not guaranteed in multi-tenant shells. As a result, the France hyperscale data center market is bifurcating; U.S. hyperscalers extend self-builds for latency-critical zones, while mid-tier and sovereign providers gravitate to colocation that prioritizes speed-to-market over full asset control.

IT hardware accounted for 45.18% of the share in 2025. Mechanical systems are on track to post the fastest growth, with a 23.83% CAGR, as liquid cooling has become mandatory for racks exceeding 40 kW. France's DDADUE law obliges new builds above 500 kW to recover waste heat, driving demand for heat exchangers and district-heating tie-ins that add 15-20% to baseline construction cost.

Electrical gear such as UPS and switchgear scales with total megawatts but benefits from modularization, keeping its growth near the headline France hyperscale data center market rate. Network and storage equipment see slower growth as hyperscalers increase server densities and shift to NVMe flash. The result is that mechanical capex now represents the primary bottleneck, absorbing an estimated 30% of total additions to the French hyperscale data center market through 2027.

The France Hyperscale Data Center Market Report is Segmented by Data Center Type (Hyperscale Self-Build, and Hyperscale Colocation), Component (IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction), Tier Standard (Tier III, and Tier IV), and Data Center Size (Large, Massive, and Mega). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services

- Microsoft Corporation

- Google LLC (Alphabet Inc.)

- Meta Platforms Inc.

- Oracle Corporation

- IBM Corporation

- OVHcloud

- Interxion (Digital Realty)

- Equinix Inc.

- Data4 Group

- Thesee DataCenter

- Scaleway (Iliad DCs)

- CloudHQ

- CyrusOne Inc.

- Vantage Data Centers LLC

- STACK Infrastructure

- Iron Mountain Data Centers

- EdgeConneX

- Quality Technology Services (QTS)

- Brookfield Asset Management

- Sesterce

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding GPU-Centric AI/ML Workloads from US and China Cloud Tenants

- 4.2.2 Sovereign-Cloud Roll-Outs by Hyperscalers In Europe

- 4.2.3 Real-Time Payment Mandates Boosting Tier IV Builds in Paris

- 4.2.4 5G Edge-Core Consolidation Along Paris-Marseille Fiber Corridors

- 4.2.5 Genai Inference Build-Outs Demanding Liquid-Cooling Campuses

- 4.2.6 Renewable PPAs Tied to New EPR2 and Offshore-Wind Projects

- 4.3 Market Restraints

- 4.3.1 Water-Usage Restrictions on Evaporative Cooling

- 4.3.2 GPU And Optic Supply-Chain Bottlenecks

- 4.3.3 Rising Heat-Tax and Carbon Levies

- 4.3.4 Local-Grid Curtailment Rules Capping Draw More Than30 MW

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

5 ARTIFICIAL INTELLIGENCE (AI) INCLUSION IN HYPERSCALE DATA CENTER (Sub-Segments are Subject to Change Depending on Availability of Data)

- 5.1 AI Workload Impact: Rise of GPU-Packed Racks and High Thermal Load Management

- 5.2 Rapid Shift toward 400G and 800G Ethernet Local OEM Integration and Compatibility Demands

- 5.3 Innovations in Liquid Cooling: Immersion and Cold Plate Trends

- 5.4 AI-Based Data Center Management (DCIM) Adoption Role of Cloud Providers

6 REGULATORY AND COMPLIANCE FRAMEWORK

7 KEY DATA CENTER STATISTICS

- 7.1 Existing Hyperscale Data Center Facilities in France (in MW) (Hyperscale Self-Build VS Colocation)

- 7.2 List of Upcoming Hyperscale Data Center in France

- 7.3 List of Hyperscale Data Center Operators in France

- 7.4 Analysis on Data Center CAPEX in France

8 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 8.1 By Data Center Type

- 8.1.1 Hyperscale Self-Build

- 8.1.2 Hyperscale Colocation

- 8.2 By Component

- 8.2.1 IT Infrastructure

- 8.2.1.1 Server Infrastructure

- 8.2.1.2 Storage Infrastructure

- 8.2.1.3 Network Infrastructure

- 8.2.2 Electrical Infrastructure

- 8.2.2.1 Power Distribution Units

- 8.2.2.2 Transfer Switches and Switchgears

- 8.2.2.3 UPS Systems

- 8.2.2.4 Generators

- 8.2.2.5 Other Electrical Infrastructure

- 8.2.3 Mechanical Infrastructure

- 8.2.3.1 Cooling Systems

- 8.2.3.2 Racks

- 8.2.3.3 Other Mechanical Infrastructure

- 8.2.4 General Construction

- 8.2.4.1 Core and Shell Development

- 8.2.4.2 Installation and Commissioning Services

- 8.2.4.3 Design Engineering

- 8.2.4.4 Fire Detection, Suppression and Physical Security

- 8.2.4.5 DCIM/BMS Solutions

- 8.2.1 IT Infrastructure

- 8.3 By Tier Standard

- 8.3.1 Tier III

- 8.3.2 Tier IV

- 8.4 By Data Center Size

- 8.4.1 Large ( Less than or equal to 25 MW)

- 8.4.2 Massive (Greater than 25 MW and Less than equal to 60 MW)

- 8.4.3 Mega (Greater than 60 MW)

9 COMPETITIVE LANDSCAPE

- 9.1 Market Share Analysis

- 9.2 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 9.2.1 Amazon Web Services

- 9.2.2 Microsoft Corporation

- 9.2.3 Google LLC (Alphabet Inc.)

- 9.2.4 Meta Platforms Inc.

- 9.2.5 Oracle Corporation

- 9.2.6 IBM Corporation

- 9.2.7 OVHcloud

- 9.2.8 Interxion (Digital Realty)

- 9.2.9 Equinix Inc.

- 9.2.10 Data4 Group

- 9.2.11 Thesee DataCenter

- 9.2.12 Scaleway (Iliad DCs)

- 9.2.13 CloudHQ

- 9.2.14 CyrusOne Inc.

- 9.2.15 Vantage Data Centers LLC

- 9.2.16 STACK Infrastructure

- 9.2.17 Iron Mountain Data Centers

- 9.2.18 EdgeConneX

- 9.2.19 Quality Technology Services (QTS)

- 9.2.20 Brookfield Asset Management

- 9.2.21 Sesterce

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-Space and Unmet-Need Assessment