PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044097

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044097

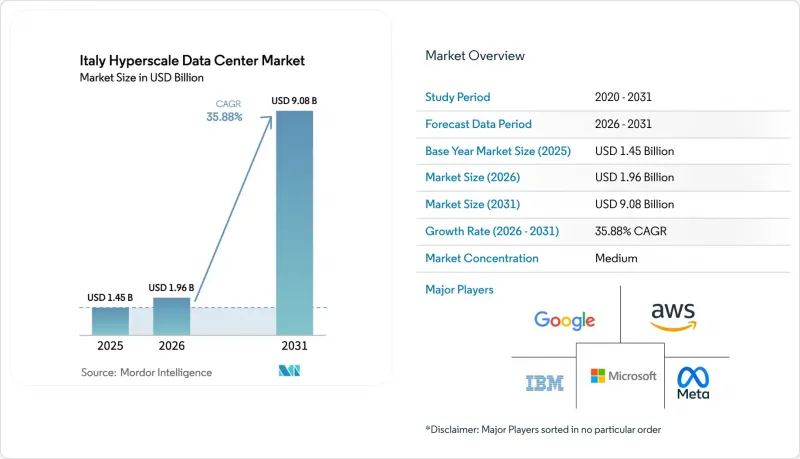

Italy Hyperscale Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Italy hyperscale data center market size is expected to increase from USD 1.45 billion in 2025 to USD 1.96 billion in 2026 and reach USD 9.08 billion by 2031, growing at a CAGR of 35.88% over 2026-2031.

Sovereign-cloud mandates under the EU Digital Decade program, sizable grants from Italy's National Recovery and Resilience Plan, and stepped-up cloud-region launches by U.S. hyperscalers are pulling new capacity toward Milan and Rome. Subsea cable landings in Sicily are repositioning southern Italy as a low-latency gateway to North Africa, while generative-AI clusters are pushing rack densities above 40 kW and accelerating the shift to direct-to-chip liquid cooling. Developers are reserving grid capacity two years ahead of construction to avoid Lombardy's head-room constraints, and many are pairing those allocations with long-term renewable power purchase agreements that cap electricity costs below EUR 50 per MWh. Competitive intensity is further magnified by the rush to pre-lease white space that meets Gaia-X and Tier IV requirements, giving turnkey colocation campuses a time-to-market edge over self-build projects.

Italy Hyperscale Data Center Market Trends and Insights

Rapid Cloud-Region Roll-Outs by AWS, Microsoft Azure and Google Cloud

Cloud majors are accelerating multi-availability-zone builds in Milan and Rome to satisfy GDPR location clauses and DORA resilience rules. AWS has earmarked EUR 1.2 billion for its Milan region through 2029, while Microsoft is injecting EUR 4.3 billion into Italy North, each project adding three or more zones interconnected by sub-10-millisecond fiber paths. Oracle's second cloud region in Turin, opened in late 2025, widened the competitive field and created an ecosystem effect in which colocation providers pre-lease shells next door to hyperscaler on-ramps. The clustering compresses procurement cycles for switchgear, generators and prefabricated liquid-cooling loops, pulling lead times below 40 weeks for some mechanical packages. Tenant urgency is further evident in DATA4's MIL02 campus where 60% of the first 15 MW phase was pre-committed before foundations were poured.

Deployment of New Subsea Cables Landing in Sicily

Sparkle's Unitirreno system went live in October 2025 with 24 fiber pairs, cutting round-trip latency between Milan and Tunis from 45 milliseconds to under 15 milliseconds and bringing Palermo within one hop of North African traffic flows. The cable coincides with Terna's 1,000 MW Tyrrhenian Link HVDC interconnector, giving Sicilian sites both bandwidth and clean-power head-room. Edge nodes near Catania are already processing maritime sensor feeds and drone video within strict 20-millisecond budgets, use cases that would be unviable over Milan-routed paths. Developers able to secure 20-30 MW at 150 kV substations near the Palermo landing station can under-cut Lombardy's land prices by half while using solar-backed PPAs to keep operating costs flat.

Grid-Capacity Head-Room Constraints in Lombardy and Lazio

Terna warns that substations around Milan and Rome could face a 150 MW shortfall by 2028 as cumulative data-center demand breaches 500 MW. Developers now secure allocations 18-24 months before breaking ground and, in some cases, pre-pay grid-access charges that raise land costs by 10-15%. Vantage Data Centers absorbed this premium at its MXP2 site, buying 96 MW capacity upfront to guarantee phased expansion. Operators that miss the queue must invest in on-site battery energy storage or accept curtailment penalties that erode service-level guarantees.

Other drivers and restraints analyzed in the detailed report include:

- EU Digital-Sovereignty and Gaia-X Compliance Boosting Local Builds

- Corporate PPAs Tapping Italy's Solar and Wind Surge

- AI-Grade GPU and Optics Preferentially Allocated to FLAP-D Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-build campuses held the majority Italy hyperscale data center market share at 61.73% in 2025, but the capital-light appeal of turnkey white space is steering hyperscalers toward third-party halls that achieve the same security envelope without tying up balance sheets. The Italy hyperscale data center market size for colocation halls is projected to expand at a 36.73% CAGR through 2031, a trajectory underpinned by MXP2's 32 MW first phase that attracted two cloud majors and one sovereign tenant before slab pour. Such early commitments shave a year off time-to-market compared with green-field self-builds, giving enterprises faster on-ramps for AI inference workloads.

Self-build remains entrenched in scenarios requiring bespoke hot-aisle geometry or proprietary optical fabrics, as seen in Oracle's Turin region that integrates directly with TIM's backbone for deterministic throughput. Even so, colocation operators are absorbing the steep entry cost of liquid cooling, letting tenants scale 60 kW racks without single-client outlay. That shift unlocks demand from fintechs and SaaS firms that would otherwise push training jobs to Frankfurt, enhancing geographic stickiness inside Italy hyperscale data center market clusters.

IT infrastructure accounted for 52.88% of the share in 2025 due to GPU-dense servers, while mechanical systems are projected to grow the fastest at a 36.84% CAGR as operators replace CRAC units with immersion tanks to maintain PUE below 1.15. Each GB200 NVL72 rack dissipates 132 kW, requiring facilities to implement 480 V backbones, 2N+1 UPS strings, and chilled-water loops rated for 45 °C inlet. These upgrades are expected to increase wallet share for switchgear and pumps.

Immersion cooling also allows higher supply-air temperatures in surrounding cold aisles, trimming fan energy and lifting overall facility efficiency. These gains explain why the Italy hyperscale data center market share for mechanical packages tied to liquid cooling is expected to eclipse legacy CRAC spend by 2028. Electrical infrastructure follows the same curve, as campuses add bus ducts and static transfer switches sized for 30 MW blocks to support staggered cloud availability zones.

The Italy Hyperscale Data Center Market Report is Segmented by Data Center Type (Hyperscale Self-Build, and Hyperscale Colocation), Component (IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction), Tier Standard (Tier III, and Tier IV), and Data Center Size (Large, Massive, and Mega). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services

- Microsoft Corporation

- Google LLC

- Meta Platforms Inc.

- Oracle Corporation

- IBM Corporation

- Equinix Inc.

- Digital Realty Trust Inc.

- STACK Infrastructure

- DATA4 Group

- Vantage Data Centers

- Compass Datacenters LLC

- Iron Mountain Inc. (Data Centers)

- Green DC Italy S.r.l.

- Aruba S.p.A.

- Rai Way S.p.A. (Data Centers)

- Irideos S.p.A. (Avalon)

- CyrusOne (KKR and GIP)

- Colt Data Centre Services

- Telecom Italia Sparkle S.p.A.

- Retelit S.p.A.

- Aligned Data Centers

- SuperNAP Italia S.r.l.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Cloud-Region Roll-Outs by AWS, Microsoft Azure and Google Cloud

- 4.2.2 Deployment of New Subsea Cables Landing in Sicily

- 4.2.3 EU Digital-Sovereignty and Gaia-X Compliance Boosting Local Builds

- 4.2.4 Corporate PPAs Tapping Italy's Solar and Wind Surge

- 4.2.5 GenAI Inference Clusters Requiring Liquid-Cooled Edge Zones

- 4.2.6 Tier IV Fintech And Instant-Payments Hubs in Milan-Turin Corridor

- 4.3 Market Restraints

- 4.3.1 Grid-Capacity Head-Room Constraints in Lombardy and Lazio

- 4.3.2 Scarcity of HV/MV Engineering Talent for 24x7 O & M

- 4.3.3 Water-Stress Curbs on Evaporative Cooling in Po Valley

- 4.3.4 AI-Grade GPU and Optics Preferentially Allocated to FLAP-D Hubs

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

5 ARTIFICIAL INTELLIGENCE (AI) INCLUSION IN HYPERSCALE DATA CENTER (Sub-Segments are Subject to Change Depending on Availability of Data)

- 5.1 AI Workload Impact: Rise of GPU-Packed Racks and High Thermal Load Management

- 5.2 Rapid Shift toward 400G and 800G Ethernet Local OEM Integration and Compatibility Demands

- 5.3 Innovations in Liquid Cooling: Immersion and Cold Plate Trends

- 5.4 AI-Based Data Center Management (DCIM) Adoption Role of Cloud Providers

6 REGULATORY AND COMPLIANCE FRAMEWORK

7 KEY DATA CENTER STATISTICS

- 7.1 Existing Hyperscale Data Center Facilities in Italy (in MW) (Hyperscale Self-Build VS Colocation)

- 7.2 List of Upcoming Hyperscale Data Center in Italy

- 7.3 List of Hyperscale Data Center Operators in Italy

- 7.4 Analysis on Data Center CAPEX in Italy

8 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 8.1 By Data Center Type

- 8.1.1 Hyperscale Self-Build

- 8.1.2 Hyperscale Colocation

- 8.2 By Component

- 8.2.1 IT Infrastructure

- 8.2.1.1 Server Infrastructure

- 8.2.1.2 Storage Infrastructure

- 8.2.1.3 Network Infrastructure

- 8.2.2 Electrical Infrastructure

- 8.2.2.1 Power Distribution Units

- 8.2.2.2 Transfer Switches and Switchgears

- 8.2.2.3 UPS Systems

- 8.2.2.4 Generators

- 8.2.2.5 Other Electrical Infrastructure

- 8.2.3 Mechanical Infrastructure

- 8.2.3.1 Cooling Systems

- 8.2.3.2 Racks

- 8.2.3.3 Other Mechanical Infrastructure

- 8.2.4 General Construction

- 8.2.4.1 Core and Shell Development

- 8.2.4.2 Installation and Commissioning Services

- 8.2.4.3 Design Engineering

- 8.2.4.4 Fire Detection, Suppression and Physical Security

- 8.2.4.5 DCIM/BMS Solutions

- 8.2.1 IT Infrastructure

- 8.3 By Tier Standard

- 8.3.1 Tier III

- 8.3.2 Tier IV

- 8.4 By Data Center Size

- 8.4.1 Large ( Less than or equal to 25 MW)

- 8.4.2 Massive (Greater than 25 MW and Less than equal to 60 MW)

- 8.4.3 Mega (Greater than 60 MW)

9 COMPETITIVE LANDSCAPE

- 9.1 Market Share Analysis

- 9.2 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 9.2.1 Amazon Web Services

- 9.2.2 Microsoft Corporation

- 9.2.3 Google LLC

- 9.2.4 Meta Platforms Inc.

- 9.2.5 Oracle Corporation

- 9.2.6 IBM Corporation

- 9.2.7 Equinix Inc.

- 9.2.8 Digital Realty Trust Inc.

- 9.2.9 STACK Infrastructure

- 9.2.10 DATA4 Group

- 9.2.11 Vantage Data Centers

- 9.2.12 Compass Datacenters LLC

- 9.2.13 Iron Mountain Inc. (Data Centers)

- 9.2.14 Green DC Italy S.r.l.

- 9.2.15 Aruba S.p.A.

- 9.2.16 Rai Way S.p.A. (Data Centers)

- 9.2.17 Irideos S.p.A. (Avalon)

- 9.2.18 CyrusOne (KKR and GIP)

- 9.2.19 Colt Data Centre Services

- 9.2.20 Telecom Italia Sparkle S.p.A.

- 9.2.21 Retelit S.p.A.

- 9.2.22 Aligned Data Centers

- 9.2.23 SuperNAP Italia S.r.l.

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-Space and Unmet-Need Assessment