PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044098

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044098

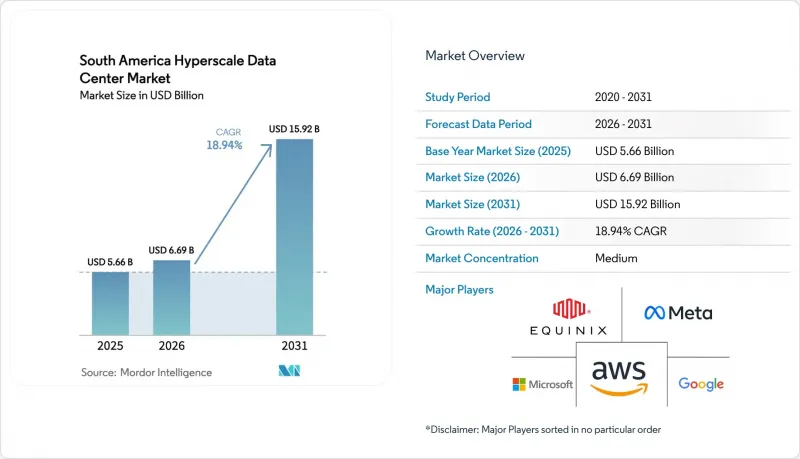

South America Hyperscale Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America hyperscale data center market size is expected to increase from USD 5.66 billion in 2025 to USD 6.69 billion in 2026 and reach USD 15.92 billion by 2031, growing at a CAGR of 18.94% over 2026-2031.

Rapid cloud-region roll-outs, new sub-sea cables, and abundant renewable-energy contracts combine to accelerate capital deployment across every major metro. Hyperscalers continue to build proprietary campuses, yet colocation providers are winning incremental megawatts by shortening time-to-production and diversifying grid exposure for clients that demand uninterrupted service. Data-sovereignty rules introduced in Brazil, Argentina, and Colombia require personal and public-sector data to remain on domestic soil, which effectively locks a rising share of workloads inside the South America hyperscale data center market. Simultaneously, GPU-rich artificial-intelligence clusters are lifting rack power densities beyond 30 kilowatts, forcing operators to invest aggressively in liquid-cooling and heat-exchanger retrofits that reshape mechanical-infrastructure budgets. Key drivers of revenue growth include hyperscaler self-build programs, cross-connect-centric business models inside carrier-neutral campuses, and renewable power purchase agreements that offer 12%-plus discounts relative to regulated tariffs. Challenges remain in the form of grid unreliability, a shortage of high-voltage technicians, and water-stress moratoria that restrict evaporative cooling in certain jurisdictions. Even so, mega campuses above 60 megawatts unlock operating leverage by centralizing substations, chilled-water plants, and fiber rings across a larger denominator of capacity. Competitive intensity sits at a moderate level because the top five providers account for about 62% of total installed megawatts, leaving meaningful headroom for regional specialists and edge-focused entrants to differentiate through local utility relationships, bilingual support teams, and next-generation liquid-cooling deployments.

South America Hyperscale Data Center Market Trends and Insights

Surge in Cloud-Region Launches by Hyperscalers

Aggressive cloud-region roll-outs anchor the strongest single catalyst for the South America hyperscale data center market. Amazon Web Services committed USD 4 billion to a Santiago cloud region that opens with 12 availability zones and an expandable 40-to-80-megawatt footprint, drawing software vendors that need single-digit-millisecond latency to operate payment engines and augmented-reality shopping carts. Microsoft mirrored the move with Azure zones in the same metro, while Google cut per-core pricing by 22% after enabling its M8g Arm-based instances in Sao Paulo. These flagship deployments trigger demand for adjacent colocation because independent software vendors must install application servers inside identical availability spheres to meet stringent service-level objectives. The loop closes when enterprises sign cross-connects to hyperscaler on-ramps, which in turn drives occupancy rates above 85% in Sao Paulo's Vila Olimpia cluster and Santiago's Quilicura corridor. Newly issued Brazilian regulations that classify sovereign workloads further lock in domestic hosting, ensuring the cloud-build momentum sustains through the medium term.

Sub-Sea Cable Landings Enhancing Latency and Redundancy

A second catalyst flows from trans-Pacific and north-south sub-sea fiber investments that drop latency and diversify fail-over paths. Google's 14,800-kilometer Humboldt cable will reduce Santiago-Sydney round-trip delay by 30 milliseconds when it lands in Valparaiso during late 2026, enabling Chilean mining firms to run predictive-maintenance models on Australian analytics platforms with no perceptible lag. Cirion Technologies activated the 72-terabit-per-second SAC-2 link between Brazil and the United States in early 2025, cutting transit charges for content-delivery networks by 18%. Meta's Project Waterworth diversified Brazilian routes in late 2024, reducing single-point-of-failure risk that previously plagued operators during anchor drag or seismic events. The new bandwidth lets cloud providers place larger cache nodes inside Sao Paulo and Santiago, serving consumers with sub-50-millisecond latency and stripping nearly 40% of peak-hour traffic from transcontinental trunks. Financial-services firms now gain dual-path network resilience that fulfils business-continuity mandates and nudges algorithmic-trading engines into regional halls.

Grid Unreliability and High Electricity Tariffs

Power instability and volatile tariffs remain the most acute short-term drag on the South America hyperscale data center market. Enel's November 2024 outage in Sao Paulo left 2.1 million customers without electricity for up to 72 hours, invoking force-majeure clauses that allowed tenants to suspend colocation payments. Industrial tariffs in Argentina jumped 38% during the same year after subsidy reductions, squeezing operating margins for facilities lacking hedged contracts. Chile's tariff regime is more stable, yet still commands a 9% premium over regional averages, prompting operators to negotiate interruptible-load deals that trade curtailment rights for 15% discounts. To maintain contractual uptime, a typical 20-megawatt hall in Sao Paulo now deploys 25 megawatts of on-site generation, which adds USD 3 million in up-front capex and USD 400,000 in recurring annual maintenance. The added expense deters latency-sensitive workloads such as real-time bidding engines, nudging those applications toward North American regions where five-nines uptime is standard.

Other drivers and restraints analyzed in the detailed report include:

- Renewable PPAs Leveraging Abundant Hydro-Solar-Wind

- Digital-Sovereignty Laws Mandating Local Hosting

- Skilled-Talent Shortage in HV Electrical and Mechanical O&M

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hyperscale colocation is forecast to expand at 19.54% during 2026-2031, surpassing the 18.94% pace set for self-build campuses, and this divergence underpins a structural shift inside the South America hyperscale data center market. Self-build designs captured 55.76% of 2025 spending because hyperscalers prefer vertical integration that lets them fine-tune cooling topologies for AI workloads. Even so, extended utility lead times and tariff shocks in Brazil and Argentina have persuaded cloud majors to hedge with leased hall blocks that can be activated within 90 days, sidestepping the 18-month greenfield timeline. Amazon Web Services exemplified this approach by reserving 5 megawatts within Equinix SP11 to backstop its Sao Paulo cloud region during maintenance windows, demonstrating that even capital-rich players value agility. Financial-services firms bolster colocation growth because Banco Central do Brasil's operational-resilience rules stipulate geographic separation between primary and disaster-recovery footprints, a requirement most economically met through multi-campus leasing rather than proprietary duplication.

Interconnection density amplifies colocation's edge by clustering tenant servers near multiple cloud on-ramps, internet exchanges, and carrier meet-me rooms. Scala Data Centers reported that 42% of 2025 revenue originated from cross-connects and peering services rather than pure rack rental, reflecting how network effects create sticky occupancy and premium yields. By contrast, self-build estates often select ex-urban land parcels where real-estate costs are 30% lower but fiber routes limited, which can constrain latency-sensitive AI inference pipelines that require multi-cloud federation. As workloads evolve toward federated learning models demanding simultaneous access to multiple public clouds, the interconnection premium inside carrier-neutral campuses will likely sustain colocation's above-market growth. Consequently, the South America hyperscale data center market appears to be tilting toward a hybrid procurement mix in which even hyperscalers blend owned and leased capacity to balance capex discipline with speed-to-capacity.

IT hardware retained the largest 42.18% share of 2025 expenditure, yet mechanical systems are positioned for the fastest 19.62% CAGR because power density continues its structural climb. GPU arrays such as NVIDIA H100 already drive cabinet loads beyond 30 kilowatts, and direct-to-chip cold plates or rear-door heat exchangers capable of 45 kilowatts per rack are now mandatory for retrofit projects. Electrical outlays rise at 18.7% because a 20-megawatt hall needs a 25-megawatt utility connection to guarantee N+1 redundancy, which requires substation upgrades that easily exceed USD 2 million. General construction lags at 18.3% because operators increasingly lease pre-built shells from industrial landlords, deploying modular white-space kits rather than breaking raw ground. Schneider Electric's latest predictive-analytics layer synchronizes chiller sequencing with AI workload surges, trimming energy waste by 12%, while Arista's 800-gigabit Ethernet spine-leaf fabrics handle east-west traffic bursts that accompany model training cycles.

Rising rack heights to 52U and even 60U further shift mechanical bills because taller frames require engineered bracing, expanded cable management, and heavier-duty airflow doors. Network upgrades form an allied theme as hyperscalers adopt 400-gigabit and 800-gigabit optics to link training nodes, which triples fiber count per rack and necessitates higher static-pressure cooling fans. Storage architecture transformation toward NVMe-over-Fabrics has centralized flash pools, reducing per-terabyte cost by 18%, yet the heavier east-west network load places added stress on cooling loops. Mechanical suppliers gain pricing power as lead times for heat-exchanger cores stretch to 16 weeks, particularly when global AI demand funnels limited copper and aluminum inventory into Tier-1 regions first. The overall result is a mechanical-spend growth curve that now exceeds server refresh trajectories, a reversal of historic patterns inside the South America hyperscale data center market.

The South America Hyperscale Data Center Market Report is Segmented by Data Center Type (Hyperscale Self-Build, and Hyperscale Colocation), Component (IT Infrastructure, Electrical Infrastructure, Mechanical Infrastructure, and General Construction), Tier Standard (Tier III, and Tier IV), Data Center Size (Large, Massive, and Mega), and Country(Brazil, Chile, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services

- Microsoft Corporation

- Google LLC

- Meta Platforms Inc.

- Digital Realty (Ascenty)

- Equinix Inc.

- Scala Data Centers

- ODATA

- EdgeConneX

- Cirion Technologies

- NTT Global Data Centers

- Vantage Data Centers LLC

- Kio Networks

- Lumen Technologies

- IBM (Kyndryl)

- Oracle Corporation

- Tencent Holdings Ltd.

- Alibaba Group Holding Ltd.

- TIVIT

- Sonda S.A.

- Ativy Data Centers

- InterNexa

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Cloud-Region Launches by Hyperscalers

- 4.2.2 Sub-Sea Cable Landings Enhancing Latency and Redundancy

- 4.2.3 Renewable PPAs Leveraging Abundant Hydro-Solar-Wind

- 4.2.4 Digital-Sovereignty Laws Mandating Local Hosting

- 4.2.5 5G Open-RAN Roll-Outs Spawning Micro-Hyperscale Edge

- 4.2.6 Lithium-Mining AI and HPC Workloads Needing Local Capacity

- 4.3 Market Restraints

- 4.3.1 Grid Unreliability and High Electricity Tariffs

- 4.3.2 Skilled-Talent Shortage in HV Electrical and Mechanical O&M

- 4.3.3 Water-Stress Moratoria on Evaporative Cooling

- 4.3.4 GPU or Optic Allocation Bias Toward Tier-1 Regions

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

5 ARTIFICIAL INTELLIGENCE (AI) INCLUSION IN HYPERSCALE DATA CENTER (Sub-Segments are Subject to Change Depending on Availability of Data)

- 5.1 AI Workload Impact: Rise of GPU-Packed Racks and High Thermal Load Management

- 5.2 Rapid Shift toward 400G and 800G Ethernet Local OEM Integration and Compatibility Demands

- 5.3 Innovations in Liquid Cooling: Immersion and Cold Plate Trends

- 5.4 AI-Based Data Center Management (DCIM) Adoption Role of Cloud Providers

6 REGULATORY AND COMPLIANCE FRAMEWORK

7 KEY DATA CENTER STATISTICS

- 7.1 Existing Hyperscale Data Center Facilities in South America (in MW) (Hyperscale Self-Build VS Colocation)

- 7.2 List of Upcoming Hyperscale Data Center in South America

- 7.3 List of Hyperscale Data Center Operators in South America

- 7.4 Analysis on Data Center CAPEX in South America

8 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 8.1 By Data Center Type

- 8.1.1 Hyperscale Self-Build

- 8.1.2 Hyperscale Colocation

- 8.2 By Component

- 8.2.1 IT Infrastructure

- 8.2.1.1 Server Infrastructure

- 8.2.1.2 Storage Infrastructure

- 8.2.1.3 Network Infrastructure

- 8.2.2 Electrical Infrastructure

- 8.2.2.1 Power Distribution Units

- 8.2.2.2 Transfer Switches and Switchgears

- 8.2.2.3 UPS Systems

- 8.2.2.4 Generators

- 8.2.2.5 Other Electrical Infrastructure

- 8.2.3 Mechanical Infrastructure

- 8.2.3.1 Cooling Systems

- 8.2.3.2 Racks

- 8.2.3.3 Other Mechanical Infrastructure

- 8.2.4 General Construction

- 8.2.4.1 Core and Shell Development

- 8.2.4.2 Installation and Commissioning Services

- 8.2.4.3 Design Engineering

- 8.2.4.4 Fire Detection, Suppression and Physical Security

- 8.2.4.5 DCIM/BMS Solutions

- 8.2.1 IT Infrastructure

- 8.3 By Tier Standard

- 8.3.1 Tier III

- 8.3.2 Tier IV

- 8.4 By Data Center Size

- 8.4.1 Large ( Less than or equal to 25 MW)

- 8.4.2 Massive (Greater than 25 MW and Less than equal to 60 MW)

- 8.4.3 Mega (Greater than 60 MW)

- 8.5 By Country

- 8.5.1 Brazil

- 8.5.2 Chile

- 8.5.3 Colombia

- 8.5.4 Argentina

- 8.5.5 Peru

- 8.5.6 Rest of South America

9 COMPETITIVE LANDSCAPE

- 9.1 Market Share Analysis

- 9.2 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 9.2.1 Amazon Web Services

- 9.2.2 Microsoft Corporation

- 9.2.3 Google LLC

- 9.2.4 Meta Platforms Inc.

- 9.2.5 Digital Realty (Ascenty)

- 9.2.6 Equinix Inc.

- 9.2.7 Scala Data Centers

- 9.2.8 ODATA

- 9.2.9 EdgeConneX

- 9.2.10 Cirion Technologies

- 9.2.11 NTT Global Data Centers

- 9.2.12 Vantage Data Centers LLC

- 9.2.13 Kio Networks

- 9.2.14 Lumen Technologies

- 9.2.15 IBM (Kyndryl)

- 9.2.16 Oracle Corporation

- 9.2.17 Tencent Holdings Ltd.

- 9.2.18 Alibaba Group Holding Ltd.

- 9.2.19 TIVIT

- 9.2.20 Sonda S.A.

- 9.2.21 Ativy Data Centers

- 9.2.22 InterNexa

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-Space and Unmet-Need Assessment