PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044102

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044102

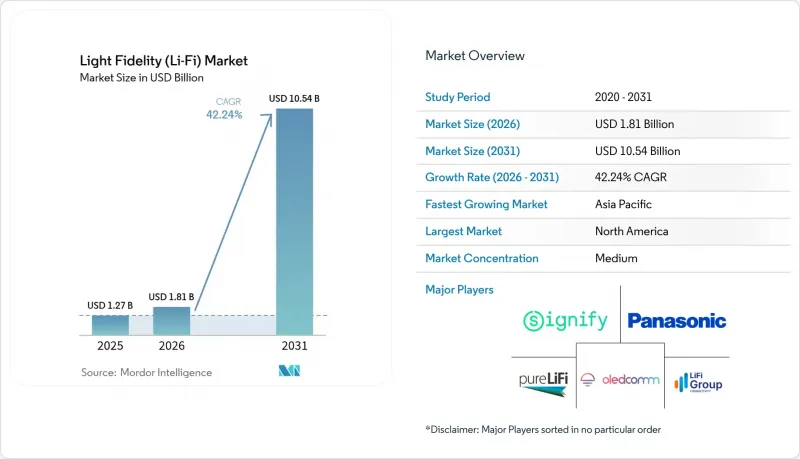

Light Fidelity (Li-Fi) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Light Fidelity (Li-Fi) market size is expected to increase from USD 1.27 billion in 2025 to USD 1.81 billion in 2026 and reach USD 10.54 billion by 2031, growing at a CAGR of 42.24% over 2026-2031.

Commercial momentum accelerated after the IEEE 802.11bb interoperability standard removed vendor-lock risk, while large-scale U.S. Army deployments validated field resilience. Enterprises now view optical wireless as a secure overlay that complements Wi-Fi, especially in environments where spectrum congestion, electromagnetic interference, or espionage threats undermine radio solutions. Early adopters in healthcare, aviation, and industrial automation report fewer network outages, lower latency, and greater confidence in data security, creating peer-driven demand that extends beyond traditional lighting refurbishment cycles. The resulting uptick in pilot activity supports a robust pipeline of retrofit and green-field projects scheduled to start during 2026-2028.

Global Light Fidelity (Li-Fi) Market Trends and Insights

LED-Lighting Retrofit Wave

Organizations that replaced fluorescent fixtures with LEDs during 2020-2025 now view Li-Fi as an incremental upgrade rather than a green-field build. Wieland Electric demonstrated the model in 2025 by embedding optical modulators into existing luminaires, avoiding new cable pulls and bringing 250 Mbps links online in days. Facility managers merge lighting and networking budgets, so the combined energy savings and connectivity gains shorten payback periods compared with separate wireless rollouts. As more lighting vendors ship "Li-Fi-ready" fixtures, procurement teams specify the capability up front, locking in future demand. The retrofit dynamic, therefore, converts a routine maintenance cycle into a large, addressable funnel for optical wireless.

IEEE 802.11bb Interoperability Standard

Formal ratification of IEEE 802.11bb in 2023, followed by government procurement notices that require compliant hardware, removed the multi-vendor risk that once stalled pilots. Enterprises now integrate Li-Fi access points into existing IP security and quality-of-service frameworks, eliminating the need for parallel IT stacks. Chipset makers have clear design rules that support volume production and narrow the cost gap with Wi-Fi. Standards alignment also eases global certification, enabling manufacturers to ship a single product family worldwide. The resulting confidence compresses sales cycles and lifts near-term shipment forecasts.

High Device Cost Versus Wi-Fi

Li-Fi access points and USB receivers still cost three to five times as much as comparable Wi-Fi gear, a premium that deters schools, start-ups, and homeowners. Oledcomm's LiFiMAX Compact kit reduces installation friction but remains priced for security-sensitive sites rather than mass adoption. The dual-hardware requirement transceivers in both lamps and client devices double the bill of materials. Until integrated chipsets appear in mainstream laptops and tablets, per-user dongle costs will keep total ownership high. Vendors are experimenting with leasing and subscription models, yet near-term uptake still hinges on applications where security or interference avoidance justifies the added spend.

Other drivers and restraints analyzed in the detailed report include:

- Secure RF-Free Links for Defense and Healthcare

- In-Flight Cabin Connectivity Adoption

- Line-of-Sight Blockage and Short Range

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Indoor networking and enterprise deployments accounted for 39.21% of the Light Fidelity (Li-Fi) market share in 2025, confirming that secure conference rooms, executive suites, and trading floors form the largest current revenue pool. Hospitals, factories, and airports added steady pilot volume, boosting confidence that Li-Fi performs reliably outside laboratories. The underwater and maritime niche, although small today, is projected to expand at a 43.66% CAGR through 2031 as navies and offshore operators replace attenuated radio links with blue-green laser systems. Healthcare installations continue to gain favor because optical signals do not interfere with life-support equipment, enabling patient-care areas to become reliable, high-bandwidth zones. Overall, strong early performance in mission-critical settings validates Li-Fi for broader enterprise rollouts.

Defense endorsements create a ripple effect that speeds procurement in civilian industries. Military field tests demonstrated that optical links remain jam-resistant and free of detectable emissions, a finding that resonates with financial services and critical infrastructure operators who fear espionage. Aviation trials show passengers can receive gigabit content without adding RF noise to avionics, further widening the technology's appeal. Smart home interest remains niche, yet gamers and home-office users already pay premiums for low-latency optical links, hinting at a gradual trickle-down to consumers. Taken together, diverse adoption paths diversify risk and underpin a strong outlook for the Light Fidelity (Li-Fi) market size tied to application breadth.

LEDs accounted for 47.38% of 2025 component revenue, as most organizations retrofit existing fixtures rather than invest in stand-alone emitters. Their dominance reflects the practical reality that ceiling lights already blanket offices and factories, so adding data modulation demands minimal extra hardware. Photodetectors, however, are on track to deliver the fastest growth, with a 43.26% CAGR from 2026 to 2031, as avalanche photodiodes and silicon photomultipliers extend range and unlock multi-gigabit throughput. Optical filters and precision lenses complement the new receivers by sharpening beam focus and blocking ambient light, essential for sunlit atria and glass-walled factories. Software and services revenue rises in tandem as enterprises need dashboards that orchestrate roaming between Li-Fi and Wi-Fi.

A transition toward laser-based vertical-cavity surface-emitting transmitters is underway, particularly in manufacturing environments that demand deterministic latency. While lasers still account for only a small share of the Light Fidelity (Li-Fi) market, their ability to reach 10 Gbps supports real-time machine vision and robotics, creating new demand for advanced detectors. Micro-controllers and modulators become more complex because adaptive coding keeps links stable during lighting variations, thereby increasing semiconductor content per fixture. As vendors chase eye-safety limits rather than raw brightness, receiver sensitivity improvements become the primary lever for coverage gains. This shift redirects value from commodity LEDs toward higher-margin photonics and signal-processing components.

The Light Fidelity Market Report is Segmented by Application (Underwater and Maritime, Aerospace and Defense, and More), Component (LEDs, Photodetectors, and More), Form Factor (Li-Fi Lamps/Luminaires, Li-Fi Dongles and Access Keys, Li-Fi Modules/Chipsets, Integrated Li-Fi Fixtures), End-User (Enterprises, Residential, Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38.42% of 2025 revenue, placing the region at the top of the light fidelity market share leaderboard. Federal cybersecurity mandates and sustained defense funding continue to anchor demand in government and financial services. Vendors also benefit from wide LED penetration, which speeds Li-Fi retrofits across corporate campuses. Local manufacturing investments shorten supply chains and satisfy domestic-content rules, further reinforcing buyer confidence. The region's growth outlook remains solid even though its forecast expansion trails that of the Asia-Pacific.

Asia-Pacific is projected to grow at a 43.29% CAGR through 2031, the highest regional growth rate recorded for the light fidelity market. Government-backed pilots in China, India, Japan, and South Korea channel grants into smart factories and smart city corridors, creating early anchor orders for domestic suppliers. Defense ministries fund secure fleet communications that avoid congested radio bands, and educational institutions install Li-Fi in research labs to protect intellectual property. Component ecosystems emerging around VCSEL arrays and photodetectors are expected to bring down costs and enable large-scale commercial launches. As standards alignment improves, cross-border deployments will allow Asian vendors to export turnkey solutions.

Europe follows closely behind, driven by stringent electromagnetic-compatibility codes and privacy regulations that favor optical confinement. Airlines retrofit cabins with Li-Fi lighting harnesses, while office landlords install secure meeting rooms to attract blue-chip tenants. Middle East and African governments pilot the technology at critical infrastructure sites, and Latin American logistics operators test it in high-bay warehouses where radio reflections degrade Wi-Fi reliability. Although these regions currently hold modest shares, successful trials could unlock pent-up demand, adding incremental volume to the global light fidelity market size during the forecast window.

- Signify N.V.

- pureLiFi Ltd

- Oledcomm SAS

- LiFi Group

- Panasonic Holdings Corp

- Lucibel SA

- Zero1 Pte Ltd

- LumEfficient LLC

- KYOCERA SLD Laser Inc

- Acuity Brands Lighting Inc

- Qualcomm Technologies Inc

- Broadcom Inc

- Lite-On Technology Corp

- Renesas Electronics Corp

- Velmenni OU

- Getac Technology Corp

- Honeywell International Inc

- PureLifi France SAS

- Firefly LiFi Ltd

- Fraunhofer HHI

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED-Lighting Retrofit Wave

- 4.2.2 Secure RF-Free Links for Defense and Healthcare

- 4.2.3 IEEE 802.11bb Interoperability Standard

- 4.2.4 In-Flight Cabin Connectivity Adoption

- 4.2.5 VCSEL-Based Above 10 Gbps Industrial Links

- 4.2.6 RF-Restricted Clean-Room Mandates

- 4.3 Market Restraints

- 4.3.1 High Device Cost versus Wi-Fi

- 4.3.2 Line-of-Sight Blockage and Short Range

- 4.3.3 Fragmented Optical-Spectrum Rules

- 4.3.4 Hybrid Li-Fi/Wi-Fi Security Gaps

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Indoor Networking and Enterprise

- 5.1.2 Healthcare and Medical Devices

- 5.1.3 Vehicle and Transportation

- 5.1.4 Underwater and Maritime

- 5.1.5 Aerospace and Defense

- 5.1.6 Smart Home and Consumer Electronics

- 5.1.7 Industrial Automation and Warehouse

- 5.2 By Component

- 5.2.1 LEDs

- 5.2.2 Photodetectors

- 5.2.3 Micro-Controllers and Modulators

- 5.2.4 Optical Filters and Lenses

- 5.2.5 Software and Services

- 5.3 By Form Factor

- 5.3.1 Li-Fi Lamps/Luminaires

- 5.3.2 Li-Fi Dongles and Access Keys

- 5.3.3 Li-Fi Modules/Chipsets

- 5.3.4 Integrated Li-Fi Fixtures

- 5.4 By End-User

- 5.4.1 Enterprises

- 5.4.2 Government and Defense

- 5.4.3 Residential

- 5.4.4 Transportation and Logistics

- 5.4.5 Industrial Manufacturing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 pureLiFi Ltd

- 6.4.3 Oledcomm SAS

- 6.4.4 LiFi Group

- 6.4.5 Panasonic Holdings Corp

- 6.4.6 Lucibel SA

- 6.4.7 Zero1 Pte Ltd

- 6.4.8 LumEfficient LLC

- 6.4.9 KYOCERA SLD Laser Inc

- 6.4.10 Acuity Brands Lighting Inc

- 6.4.11 Qualcomm Technologies Inc

- 6.4.12 Broadcom Inc

- 6.4.13 Lite-On Technology Corp

- 6.4.14 Renesas Electronics Corp

- 6.4.15 Velmenni OU

- 6.4.16 Getac Technology Corp

- 6.4.17 Honeywell International Inc

- 6.4.18 PureLifi France SAS

- 6.4.19 Firefly LiFi Ltd

- 6.4.20 Fraunhofer HHI

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment