PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044110

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044110

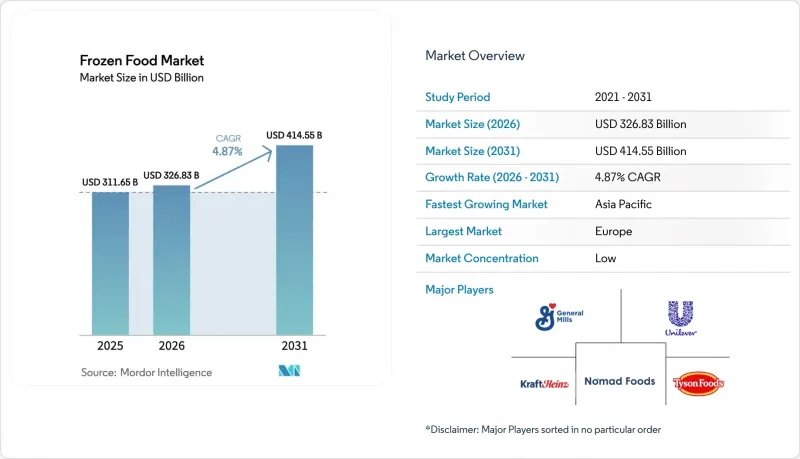

Frozen Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

By 2031, the global frozen food market, valued at USD 326.83 billion in 2026, is projected to grow to USD 414.55 billion, marking a CAGR of 4.87%.

Market growth is driven by rising consumer demand for convenient, long-shelf-life food products that reduce preparation time while maintaining quality and nutrition. Technological advancements such as Individual Quick Freezing (IQF) are improving product texture, flavor, and nutrient retention, strengthening consumer acceptance of frozen foods. Additionally, the expansion of modern retail and e-commerce platforms, along with temperature-controlled logistics, is improving product accessibility. In addition, rising investments in cold chain infrastructure across emerging economies are enhancing refrigerated storage, transportation, and distribution networks, enabling the efficient supply of frozen foods and supporting the market's steady global growth .

Global Frozen Food Market Trends and Insights

Surge in Frozen Snacking for Home-Based Socialising

As home entertainment trends continue to shape consumer habits, the demand for frozen snacks experiences significant growth during small gatherings and social events, thereby strengthening the frozen food market. Millennials and Generation Z consumers are increasingly drawn to bite-sized frozen appetizers compared to older generations. The market offers a wide range of frozen food options, including pizzas, sliders, and various snack foods, all designed to provide both convenience and variety. These products are easy to prepare and cater to diverse taste preferences, making them particularly suitable for social occasions. The frozen snack market is expanding as consumers increasingly seek solutions that combine efficiency with flavorful options for entertaining. This growth is primarily driven by Millennials and Generation Z, who prefer snacking options that are both convenient and varied. The growing adoption of air fryers in households further accelerates this market expansion, as frozen food manufacturers focus on developing products specifically tailored for air fryer preparation. In a strategic move, in April 2025, McCain Foods India collaborated with Philips to introduce a range of frozen snacks optimized for air fryers, including crispy fries that replicate the taste and texture of restaurant-quality offerings, providing consumers with quick and convenient dining solutions at home.

Rapid Uptake of IQF Technology Enabling Texture-Safe Vegetables

Individual Quick Freezing (IQF) technology has revolutionized the frozen vegetable market, ensuring that the structural integrity and nutritional value of produce are preserved. This advancement allows for the freezing of a wide array of vegetables, including those previously deemed challenging, such as avocados and leafy greens. As a result of this enhanced preservation quality, there has been a significant increase in frozen vegetable consumption, especially among health-conscious consumers. Furthermore, IQF technology plays a pivotal role in reducing food waste. By extending the seasonal availability of produce and minimizing spoilage throughout the supply chain, it addresses a critical concern in the industry. For example, the FLoFREEZE Individual Quick-Freezing freezer from JBT Frigoscandia employs advanced individual freezing technology, catering to vegetables, fruits, fish, and other premium IQF products. With its true fluidization capabilities, the system ensures both versatility and high-quality results. Additionally, JBT's Sequential Defrost technology offers substantial processing capacity in the Frigoscandia FLoFREEZE series-M range. Its adjustable airflow settings further enhance its utility, allowing it to accommodate products of diverse sizes and types.

Supply Gaps in Sustainable Seafood for Frozen SKUs

Frozen seafood manufacturers are facing significant supply chain challenges as consumer demand for sustainably sourced seafood continues to rise. The current market demand exceeds the availability of seafood certified by the Marine Stewardship Council (MSC) and responsibly harvested species. This imbalance is particularly evident in popular seafood varieties such as salmon, shrimp, and cod. Supplies of these wild-caught species are under increasing pressure due to overfishing and the adverse effects of climate change. The frozen food industry is experiencing notable shortages of seafood products that meet established sustainability standards. For example, the North Sea saithe fishery is expected to lose its certification from the Marine Stewardship Council by the end of June 2025. This suspension, announced by the Marine Stewardship Council earlier in the same month, follows a period of reduced stock productivity. A recent assessment conducted by the International Council for the Exploration of the Seas confirmed that the stock levels have fallen below sustainable thresholds. The North Sea saithe fisheries, which are a key source of cold-water species in the region, are the latest to face this certification setback.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Direct-to-Consumer Frozen Meal Kits

- Rising Demand for Clean-Label Frozen Entrees

- Consumer Perception of "Freshness Gap" vs. Chilled Meals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, ready-to-cook products commanded a dominant 63.32% of the market share, appealing to consumers who value control over seasoning and cooking methods, yet wish to save time on tasks like chopping vegetables or marinating proteins. Meanwhile, ready-to-eat formats are witnessing a robust annual growth of 5.27%, a trend projected to continue through 2031. This surge is largely fueled by single-person households and busy professionals who prioritize speed over customization. Such a divergence indicates a bifurcation in the category: ready-to-cook caters to families planning dinners together, while ready-to-eat focuses on quick lunches and last-minute meals.

In response, manufacturers are increasingly blurring category lines. They're rolling out hybrid products, such as pre-seasoned raw proteins that cook in just 8 minutes and fully cooked bowls that merely need a quick sear for texture enhancement. This wave of innovation is most pronounced in the Asia-Pacific region. Here, convenience-store chains, exemplified by 7-Eleven Japan, are offering frozen rice bowls and noodle kits, allowing customers to microwave them in-store, effectively transforming retail spaces into quasi-foodservice venues. Regulatory considerations also play a pivotal role. For instance, the European Union's Nutri-Score system, which penalizes high sodium content on front-of-pack labels, is nudging ready-to-eat manufacturers towards reformulation. This is crucial to avoid lower scores that could alienate health-conscious consumers. On the other hand, ready-to-cook items navigate these regulatory waters more smoothly, as the addition of salt during cooking grants brands greater formulation flexibility.

The Frozen Food Market Report Segments the Industry Into Product Category (Ready-To-Eat, Ready-To-Cook), Product Type (Frozen Fruits and Vegetables, Frozen Meat and Fish, Frozen Ready Meals, Frozen Desserts, and More), Distribution Channel (On Trade and Off Trade), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe holds a 31.32% market share in 2025, supported by established frozen food consumption patterns and developed cold-chain infrastructure. The market encompasses major economies, including Germany, the United Kingdom, France, Spain, Italy, and Russia, each contributing significantly to the regional market dynamics. The European market focuses on product innovation, sustainable packaging solutions, and premium frozen food products.

Asia-Pacific demonstrates the fastest growth with a CAGR of 6.80% during 2026-2031. The frozen food industry shows significant growth potential, driven by rapid urbanization, changing consumer lifestyles, and increasing disposable incomes. The region encompasses major markets including China, Japan, India, and Australia, each showing distinct market characteristics and growth patterns. The region is experiencing substantial developments in cold chain infrastructure and retail network expansion, supporting growth in the frozen food market. Consumers in the Asia-Pacific show increasing acceptance of frozen food products, particularly in tier-1 and tier-2 cities.

The North American frozen food market demonstrates robust growth driven by changing consumer lifestyles and increasing demand for convenient food options. The United States leads the regional market, followed by Canada and Mexico, with each country showing distinct consumption patterns and market dynamics. The frozen food industry in the United States has expanded its premium offerings, with manufacturers introducing new product variants to meet consumer preferences. For instance, in February 2024, Conagra announced the expansion of its Bertolli brand in the frozen food segment with the launch of Bertolli oven meals and appetizers. The oven meals include three varieties: chicken alfredo, chicken parmigiana and penne, and meatball rigatoni. The appetizers feature three cheese toasted ravioli and arancini Parmesan, which are compatible with air fryers.

- Nestle S.A.

- Conagra Brands Inc.

- General Mills Inc.

- Nomad Foods Ltd.

- Tyson Foods Inc.

- McCain Foods Ltd.

- The Kraft Heinz Company

- Ajinomoto Co. Inc.

- Unilever PLC

- Hormel Foods Corp.

- Bellisio Foods Inc.

- Iceland Foods Ltd.

- Grupo Bimbo SAB de CV

- Charoen Pokphand Foods

- BRF S.A.

- Oetker Group

- Frosta AG

- NH Foods Ltd.

- Maple Leaf Foods Inc.

- CJ CheilJedang Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Frozen Snacking for Home-Based Socialising

- 4.2.2 Rapid Uptake of IQF Technology Enabling Texture-Safe Vegetables

- 4.2.3 Growth of Direct-to-Consumer (D2C) Frozen Meal Kits

- 4.2.4 Rising Demand for Clean-Label Frozen Entrees

- 4.2.5 Increasing Frozen aisles in Retail Channels

- 4.2.6 Increasing Demand for Plant-Based Frozen Foods

- 4.3 Market Restraints

- 4.3.1 Supply Gaps in Sustainable Seafood for Frozen SKUs

- 4.3.2 Consumer Perception of "Freshness Gap" vs. Chilled Meals

- 4.3.3 Rising Raw Material Cost

- 4.3.4 High tariffs on imported frozen goods

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Product Category

- 5.1.1 Ready-to-Eat

- 5.1.2 Ready-to-Cook

- 5.2 By Product Type

- 5.2.1 Frozen Fruits and Vegetables

- 5.2.2 Frozen Meat and Seafood

- 5.2.3 Frozen Ready Meals

- 5.2.4 Frozen Snacks and Bakery

- 5.2.5 Frozen Desserts

- 5.2.6 Other Product Types

- 5.3 By Distribution Channel

- 5.3.1 On-Trade

- 5.3.2 Off-Trade

- 5.3.2.1 Supermarkets and Hypermarkets

- 5.3.2.2 Convenience Stores

- 5.3.2.3 Online Stores

- 5.3.2.4 Other Retail Formats

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nestle S.A.

- 6.4.2 Conagra Brands Inc.

- 6.4.3 General Mills Inc.

- 6.4.4 Nomad Foods Ltd.

- 6.4.5 Tyson Foods Inc.

- 6.4.6 McCain Foods Ltd.

- 6.4.7 The Kraft Heinz Company

- 6.4.8 Ajinomoto Co. Inc.

- 6.4.9 Unilever PLC

- 6.4.10 Hormel Foods Corp.

- 6.4.11 Bellisio Foods Inc.

- 6.4.12 Iceland Foods Ltd.

- 6.4.13 Grupo Bimbo SAB de CV

- 6.4.14 Charoen Pokphand Foods

- 6.4.15 BRF S.A.

- 6.4.16 Oetker Group

- 6.4.17 Frosta AG

- 6.4.18 NH Foods Ltd.

- 6.4.19 Maple Leaf Foods Inc.

- 6.4.20 CJ CheilJedang Corp.

7 Market Opportunities and Future Outlook