PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044118

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044118

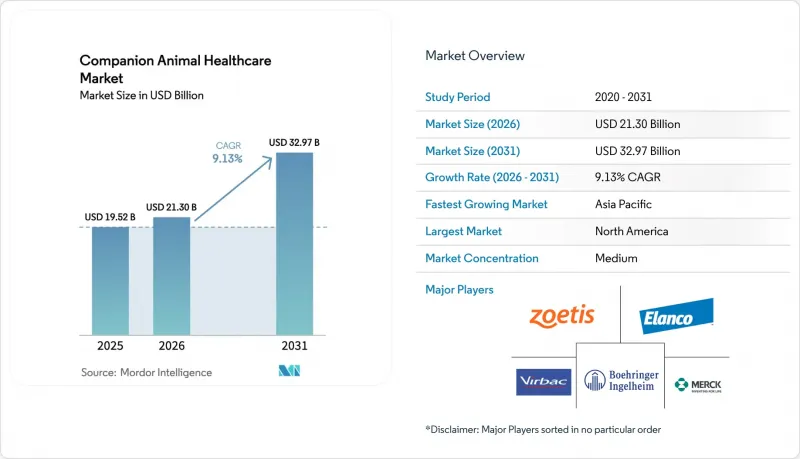

Companion Animal Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Companion Animal Healthcare Market size was valued at USD 19.52 billion in 2025 and is estimated to grow from USD 21.30 billion in 2026 to reach USD 32.97 billion by 2031, at a CAGR of 9.13% during the forecast period (2026-2031).

Expanding pet insurance coverage, rapid uptake of point-of-care (POC) diagnostics, and the growing acceptance of biologics are collectively reshaping revenue flows across the companion animal healthcare market. Higher disposable incomes among urban households, coupled with the humanization of pets, propel demand for sophisticated interventions ranging from oncology protocols to orthopedic surgeries. Diagnostics that deliver sub-10-minute turnaround times improve clinical decision-making and shorten the gap between symptom onset and therapy initiation, boosting downstream therapeutic sales. At the same time, e-commerce platforms disrupt legacy dispensing models by pairing telehealth consultations with auto-ship subscriptions, while practice-management software integrates diagnostics, billing, and inventory management in a single workflow. Competitive differentiation is shifting from blockbuster drugs toward data-driven services and cloud-connected devices that embed clinics more deeply in the daily routines of pet owners.

Global Companion Animal Healthcare Market Trends and Insights

Increase in Pet Adoption & Humanization of Animals

Pet ownership rose to 66% of U.S. households in 2024, with average annual outlays of USD 1,480 per pet, mirroring human wellness budgets. Owners now opt for procedures once limited to people-organ transplants, chemotherapy, and custom orthopedic implants-thereby elevating average revenue per patient. Millennials and Gen Z show the highest propensity to acquire pet insurance, positioning premium therapies for sustained uptake as these cohorts mature into higher income brackets. Wearable monitors that track heart rate, sleep, and activity create longitudinal datasets that surface conditions earlier, justifying frequent veterinary engagement. Device approvals must align with FDA Center for Veterinary Medicine safety guidelines, which prolong commercialization timelines but fortify consumer confidence. The combined effect is a virtuous cycle where data-driven insights validate higher standards of care and reinforce growth across the companion animal healthcare market.

Expanding Penetration of Pet Insurance

United States pet insurance premiums climbed from USD 3.9 billion in 2023 to USD 4.7 billion in 2024, covering 6.2 million animals and delivering 21.4% year-over-year growth. Insurance uptake enables costly monoclonal antibody injections for osteoarthritis or oncology regimens topping USD 15,000, because 70%-90% reimbursement rates lower owner out-of-pocket exposure. Surgical specialties benefit markedly; orthopedic procedures rose 18% between 2023 and 2024 in lockstep with insurance expansion. Carriers now add preventive diagnostics-annual blood panels and genetic screens-to their formularies, migrating revenue from reactive to proactive care models. The United Kingdom and Sweden already exceed 25% penetration, while Japan's 2024 tax incentive program is catalyzing regional growth. Increased coverage drives predictable demand, which stabilizes cash flows across the companion animal healthcare market.

Escalating Veterinary Service & Drug Costs

U.S. veterinary service prices rose 10.2% from 2023 to 2024, dwarfing 3.4% general inflation and lifting routine wellness exams from USD 52 to USD 58. Emergency visits in metro areas now exceed USD 1,500, discouraging timely care among budget-constrained owners. Drug prices mirror this trend: Simparica Trio wholesale cost climbed 8% in 2024 amid API constraints in India and China. Because 94% of U.S. pets remain uninsured, many owners defer elective procedures or pivot to lower-cost generics, tempering near-term growth across the companion animal healthcare market. Price-sensitive regions in Latin America and Southeast Asia feel the strain most acutely, as per-capita veterinary spending stays below USD 50 annually.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Advanced In-Clinic & POC Diagnostics

- Boom in Chronic-Care Monoclonal Antibodies

- Global Shortage of Skilled Veterinary Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostics represented the fastest-growing category, expanding at 12.25% CAGR through 2031, while therapeutics retained a 37.56% share of the companion animal healthcare market in 2025. Vaccines, parasiticides, and NSAIDs supply a stable base, but their incremental upside is modest as immunization rates plateau in developed economies. Multimodal parasiticides such as Simparica Trio captured owners' preference for single-dose convenience, yet competitive pressure from generics compresses margins. Monoclonal antibodies for chronic pain and emerging oncology indications are gaining traction, commanding premium pricing and anchoring revenue resilience inside the companion animal healthcare market.

The diagnostics surge is powered by POC devices, immunoassays, and molecular panels that compress turnaround times and facilitate same-visit care. Standard SDMA kidney screenings, once specialty procedures, are now routine during wellness exams. IDEXX alone processes over 200 million tests annually, reinforcing a razor-and-blade model that locks clinics into reagent subscriptions. Cloud integration funnels lab data into practice-management software, supporting AI alerts that flag anomalies in real time. Regulatory oversight by FDA's Center for Veterinary Medicine ensures >=95% accuracy, a bar that filters substandard entrants yet lengthens release cycles. Digital health services-telemedicine, wearable analytics, and practice-management platforms-remain smaller but accelerate as clinics seek operational efficiencies.

Infectious diseases dominated revenue with a 31.53% slice of the companion animal healthcare market size in 2025, fueled by mandated rabies vaccines and endemic parasite control. However, price competition and vaccination saturation restrain future expansion. Oncology, by contrast, is forecast to compound at 11.85% CAGR, riding breakthroughs such as Tanovea-CA1 and Stelfonta that improve survival without the adverse events associated with traditional chemotherapy.

Companion animals exhibit cancer rates comparable to humans, spurring investment in targeted biologics. Tanovea-CA1 achieved a 79% response rate in canine lymphoma, prompting earlier adoption by clinics equipped with in-house diagnostics. Stelfonta offers a non-surgical solution for mast cell tumors, reducing anesthesia risk and recovery time. Dermatology and allergy therapies like Apoquel and Cytopoint enjoy recurring demand, while endocrine disorders deliver predictable insulin and hormone-replacement sales. Together, these dynamics pivot revenue toward chronic disease management, layering predictable cash flows onto the companion animal healthcare market.

The Companion Animal Healthcare Market Report is Segmented by Product Type (Therapeutics [Vaccines, and More], Diagnostics [Immunodiagnostic Tests, and More], and Digital Health & Services), Therapeutic Area (Infectious Diseases, and More), Animal Type (Dogs, and More), Distribution Channel (Veterinary Hospitals & Clinics, and More), Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 36.53% share in 2025, benefiting from extensive specialty hospitals and mature insurance penetration. Corporate consolidators such as Mars Veterinary Health operate multi-state clinic networks and central labs that enable same-day diagnostics. Europe contributed roughly 28%, with synchronized EMA approvals expediting monoclonal antibody launches. The United Kingdom's insurance penetration above 25% sustains high-ticket therapies, whereas Eastern Europe lags on per-pet spending.

Asia-Pacific is poised for 10.21% CAGR, buoyed by rising pet ownership, insurance uptake, and government incentives. China's urban pet population topped 120 million in 2024, and policies rose 81% to 3.8 million in 2025, signaling willingness to fund preventive and chronic care. Japan's clinic count rose 8% between 2023 and 2025, underpinned by tax incentives for insurance. India remains nascent but exhibits 15% annual growth in pet adoption across major cities. The Middle East and Africa account for 5% of revenue, and South America represents 6%, with Brazil holding long-term promise despite macro volatility.

- bioMerieux

- Boehringer Ingelheim

- Ceva

- Covetrus

- Dechra Pharmaceuticals plc

- Elanco

- Heska

- Hipra

- IDEXX

- KRKA d.d.

- Mars Veterinary Health

- Merck

- Neogen Corp.

- Norbrook Laboratories

- PetIQ Inc.

- Phibro Animal Health

- Thermo Fisher Scientific

- Vetoquinol

- Virbac

- Zoetis

- Zomedica Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Pet Adoption & Humanization of Animals

- 4.2.2 Expanding Penetration of Pet Insurance

- 4.2.3 Rapid Uptake of Advanced In-Clinic & POC Diagnostics

- 4.2.4 Boom in Chronic-Care Monoclonal Antibodies

- 4.2.5 AI-Powered Predictive Analytics for Preventive Care

- 4.2.6 Subscription Models Monetising Wearable Biometrics

- 4.3 Market Restraints

- 4.3.1 Escalating Veterinary Service & Drug Costs

- 4.3.2 Global Shortage of Skilled Veterinary Talent

- 4.3.3 Regulatory Lag for Gene-Editing & Cell Therapies

- 4.3.4 Cyber-Security Risks to Connected Vet Devices

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Therapeutics

- 5.1.1.1 Vaccines

- 5.1.1.2 Parasiticides

- 5.1.1.3 Anti-Infectives

- 5.1.1.4 NSAIDs & Pain Management

- 5.1.1.5 Monoclonal Antibodies

- 5.1.1.6 Medical Feed Additives

- 5.1.1.7 Other Therapeutics

- 5.1.2 Diagnostics

- 5.1.2.1 Immunodiagnostic Tests

- 5.1.2.2 Molecular Diagnostics

- 5.1.2.3 Diagnostic Imaging

- 5.1.2.4 Point-of-Care Devices

- 5.1.2.5 Other Diagnostics

- 5.1.3 Digital Health & Services

- 5.1.3.1 Tele-medicine Platforms

- 5.1.3.2 Practice-Management Software

- 5.1.3.3 Wearable Monitoring Devices

- 5.1.1 Therapeutics

- 5.2 By Therapeutic Area

- 5.2.1 Infectious Diseases

- 5.2.2 Dermatology/Allergy

- 5.2.3 Pain & Inflammation

- 5.2.4 Endocrine & Metabolic Disorders

- 5.2.5 Oncology

- 5.2.6 Cardiology

- 5.3 By Animal Type

- 5.3.1 Dogs

- 5.3.2 Cats

- 5.3.3 Other Companion Animals

- 5.4 By Distribution Channel

- 5.4.1 Veterinary Hospitals & Clinics

- 5.4.2 Retail Pharmacies

- 5.4.3 Online /E-commerce Platforms

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 bioMerieux SA

- 6.3.2 Boehringer Ingelheim Animal Health

- 6.3.3 Ceva Sante Animale

- 6.3.4 Covetrus Inc.

- 6.3.5 Dechra Pharmaceuticals plc

- 6.3.6 Elanco Animal Health

- 6.3.7 Heska Corp.

- 6.3.8 HIPRA

- 6.3.9 IDEXX Laboratories Inc.

- 6.3.10 KRKA d.d.

- 6.3.11 Mars Veterinary Health

- 6.3.12 Merck Animal Health

- 6.3.13 Neogen Corp.

- 6.3.14 Norbrook Laboratories

- 6.3.15 PetIQ Inc.

- 6.3.16 Phibro Animal Health Corp.

- 6.3.17 Thermo Fisher Scientific

- 6.3.18 Vetoquinol SA

- 6.3.19 Virbac

- 6.3.20 Zoetis Inc.

- 6.3.21 Zomedica Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment